Content

Report

What do young Chinese think about social credit? It's complicated

Main findings and conclusions

- China’s emerging social credit system should be understood not as a single unified system but as a package or policy framework combining many different policies.

- Results of our student survey at three Chinese universities between December 2018 and April 2019 suggest that no easy conclusions about broad-based approval of such policies can be drawn. We also surveyed Taiwanese and German students for comparison.

- Our survey sought their responses to four policies associated with the social credit system mega-project. Students from China rated the measures more positively, with approval rates between 41 and 57 percent, than their German counterparts, who gave a maximum of 19 percent approval. However, approval rates from students in China were lower than the 80 percent approval rates found in a previous study by researchers at Freie Universität Berlin.

- Our results also show a complex picture of how Chinese respondents think about social credit and the associated risks: e.g. government surveillance was rated as a higher risk in China than abuse of data by private companies, although media discussions related to "privacy protection" in China’s official media has focused predominantly on the latter.

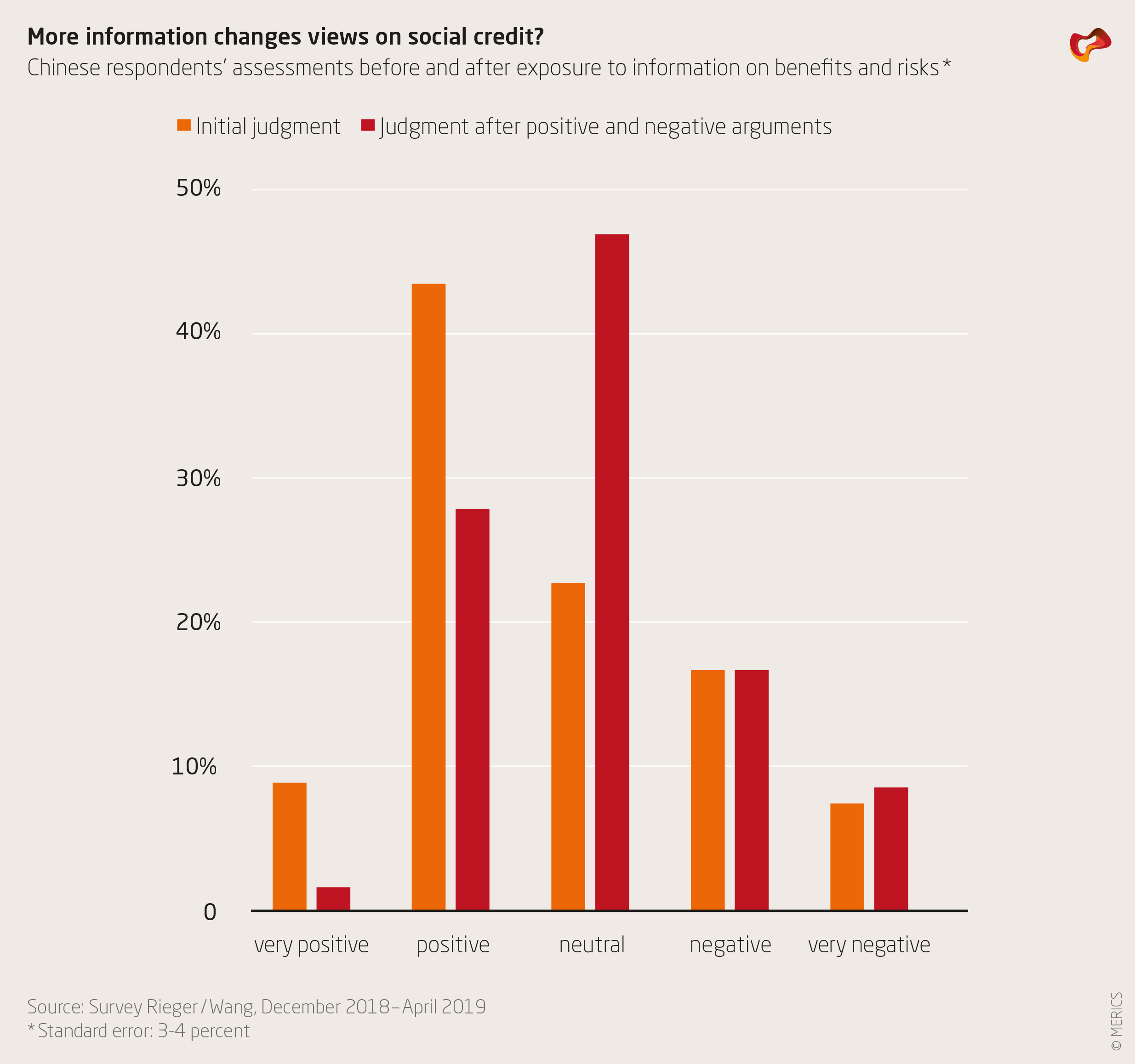

- After being informed about potential positive and negative effects, respondents were asked to rate one of the policies again; the proposal for an aggregated social credit score based on a range of behaviors. Germans rated it slightly more positively than before, whereas Chinese respondents adjusted their approval substantially downwards, from 53 percent in favor to just 29 percent.

- A mixture of cultural factors, concerns about safety and trust as well as censorship account for higher approval rates of policies associated with “building social credit” in China.

1. Revisiting public opinion on the social credit system

One of China’s most controversial recent government projects is the “social credit system” (社会信用体系, shehui xinyong tixi). It originated from the shortcomings of the consumer credit system and retail banking within the People’s Republic of China (PRC). Initially, it was conceived of as a way to compensate for the lack of financial credit scores and similar data on individuals to evaluate trustworthiness and creditworthiness. Lack of trust is a burden for China’s economy as it makes lending difficult and facilitates fraud. However, the idea quickly expanded to include many aspects of anti-social behavior as defined by the government.

Although the phrase “social credit system” has become familiar, and widely reported on in Western media, there is as yet no single, centrally coordinated system. Rather, there are a large number of different measures and pilot projects.

Government bodies implement the core of the system. However, many non-mandatory spin-offs have emerged. Several hundred policy documents have been produced by central, provincial and local government institutions. The rollout remains in the experimental phase and is taking place around China an uneven way.

There are three different target groups for measures rolled out under the social credit framework:

- public institutions

- individuals

- companies or other legal entities like NGOs

Projects that target individuals have varied goals and differ in the amount of data collected and the consequences of a certain score. Some deal solely with financial transactions and resemble the credit rating agencies common in other countries, such as FICO in the United States or Germany’s Schufa (General Credit Protection Agency). However, the most ambitious and potentially controversial pilot projects aim to steer people’s daily lives using automatized observation and a sophisticated system of sanctions to enforce the desired behavior.

Western observers have been puzzled at why, given the radical scope of these proposals, there has not been more resistance in China. In discussions of the social credit system, it is often assumed or implied that Chinese people simply care less about surveillance or their privacy than Westerners. While it is true that many ideas associated with the social credit system are indeed seen very critically by many Westerners, it is much more difficult to obtain an objective view of how people in China think about such issues. Genia Kostka of the Freie Universität Berlin published the first survey on the topic in 2019, titled “China’s social credit systems and public opinion: Explaining high levels of approval.” She found generally high approval rates for the social credit system as a whole,1 with the highest approval rates among wealthier, older and better-educated city dwellers.

Given that the construction of social credit is a package consisting of a range of different policies and, as implementation advances, more and more Chinese are confronted with these measures in their daily lives, it is important to revisit the issue by looking at more concrete examples.

We therefore conducted an anonymous internet survey from December 2018 to April 2019 among university students from three Chinese universities located in different parts of the PRC. We then compared the results with identical surveys carried out in Germany and Taiwan at the same time. In total, 553 students took part: 215 from mainland China, 227 from Germany and 61 from Taiwan. In addition, we collected data from 142 subjects from various other countries (outside China, Taiwan and Germany). Although the respondents are not representative of the general population, they constitute an important sub-group in Chinese society, namely urban, educated young people, that the PRC party-state particularly cares about.

2. Survey: Questions designed to stimulate reflection

We took examples of real pilot projects in China and briefly introduced the different policy proposals to the participants. As we were most interested in how people think about social credit systems ranking individuals, we chose measures that apply ratings or sanctions to individuals, rather than to enterprises or institutions:

- People who have not complied with court orders to repay some money are punished in the following way: if someone calls them, the caller first hears a message that the person he/she is trying to reach has been blacklisted. The message then asks the caller to persuade them to comply with the court order. Only afterwards are they connected to the person they wanted to talk to.

- Cameras and artificial intelligence (AI) are used to detect any traffic violations. Facial recognition software identifies the culprit and fines them automatically and immediately.

- This idea is extended beyond traffic violations to all kinds of behavior, from making prompt payments to depositing garbage correctly; the system calculates an individual’s aggregated score which determines their privileges and restrictions, such as whether somebody is allowed to book high-speed trains.

- A credit score based on behaviors is used to decide eligibility for loans. We then asked participants how they saw each of these policy proposals. Generally, their responses were in line with Kostka’s previous finding of higher approval rates within China than in, say, Germany. However, our findings challenge the idea that PRC citizens are overwhelmingly supportive of the system and do not care about keeping information private from the government. The survey generated several findings that complicate the current understanding of how China’s citizens view the social credit system.

3. Initial findings: Chinese respondents are concerned about risks of government surveillance

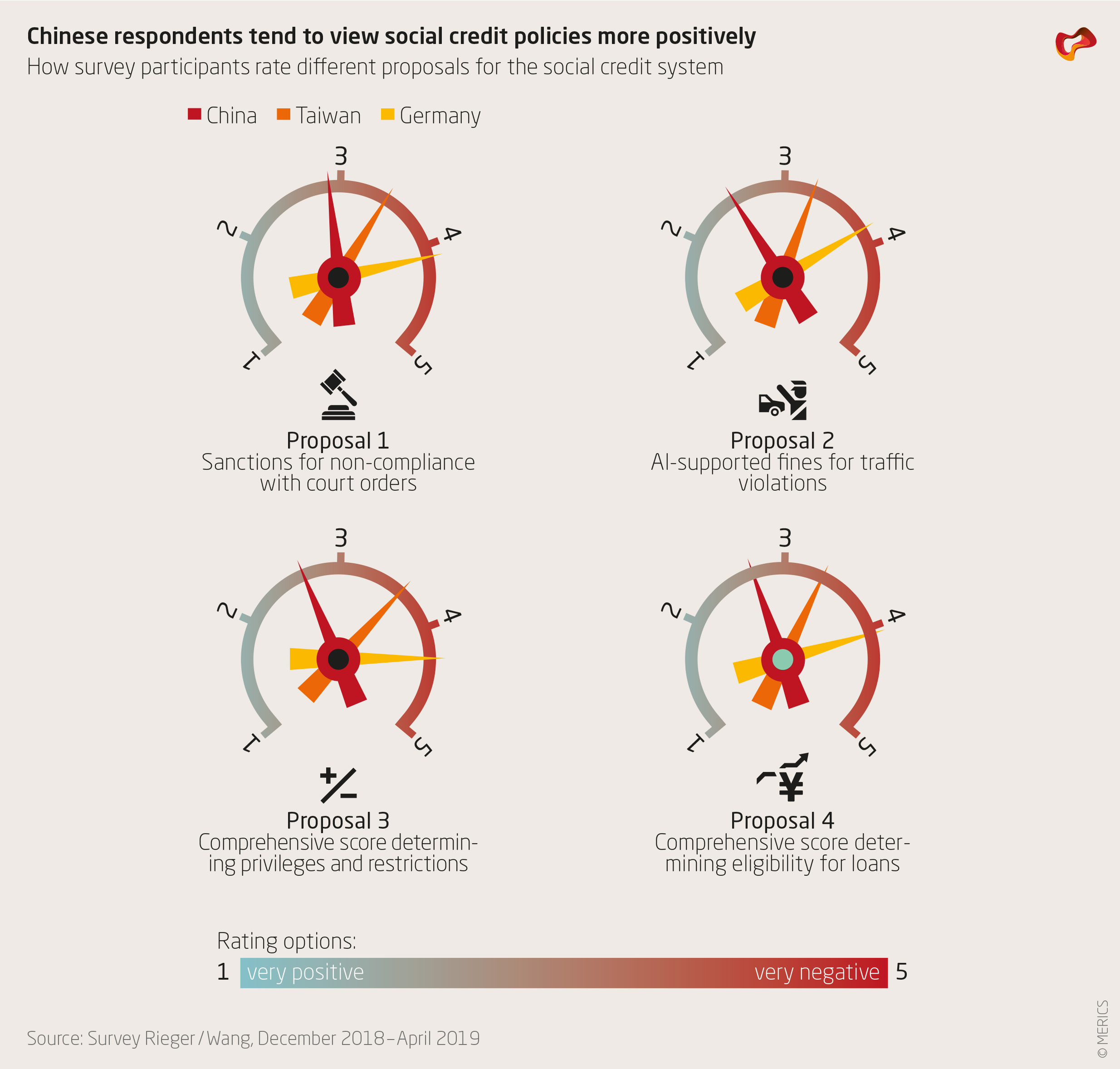

Approval ratings in China were somewhat smaller than in Kostka’s survey. Overall, between 41 and 57 percent of the participants had a “positive” or “very positive” opinion about the projects. There were also slight differences between the proposals: The most-liked one was proposal 2, involving immediate fines for traffic violations, and the least popular was proposal 1 where individuals are asked to reprimand fellow-citizens over non-payments. There was also significant opposition, particularly to proposal 1, which 31 percent rated negatively or very negatively, and to proposal 3 suggesting aggregate individual scores and personalized sanctions for a range of behaviors – it got a 23 percent “negative” or “very negative” response.

The results show the absence of either uniform approval or disapproval towards social credit systems among PRC university students: opinions are mixed. If we were to translate the opinions into school grades (very positive=A, very negative=F), the proposals would only get a C+ (“satisfactory”). Nevertheless, average agreement with such measures was much higher than among respondents in Germany, where none of the projects got more than 19 percent approval.

There are several possible explanations for why China’s citizens like or dislike these proposals. The survey findings mirrored some frequently stated arguments for and against building social credit profiles. On the positive side, there was the potential for increased trust among strangers; reduced crime and greater economic benefits. Cons included threats posed by hackers, privacy concerns, negative consequences of mistakes, rules in favor of institutions but not the people, government surveillance, and sharing data with private companies. Agreements to the positive effects were very similar across survey respondents of different national origins, with reduced crime seen as the biggest advantage.

However, the perceived risks reveal remarkable differences: in China, respondents reported the highest concerns over the risk of government surveillance and government institutions putting their own interests first. Interestingly, sharing huge amounts of data with private companies was seen as much less of a problem. This seems counterintuitive since in recent years, China’s official media has

frequently discussed data privacy with a focus on the protection of individuals from overreach by private companies.2 Overreach on the part of the government is rarely if ever addressed in China’s official media coverage. Therefore, one might assume that PRC students would also be primarily concerned about surveillance and abuse of data by private entities rather than government surveillance, but this is not the case.

4. Possible explanations: Cultural background, social conditions and censorship shape opinions

We would argue that there are several possible reasons why Chinese respondents generally evaluated social credit systems less negatively than interviewees in Germany:

- Chinese culture traditionally puts more emphasis on society than on the individual.3 Thus, measures that limit individual freedoms, but contribute to overall social well-being, are seen more positively than in Western countries. The difference may be increased by political and ideological education in the PRC which puts much greater emphasis on collective identities and interests.

- Worries about anti-social behavior and criminality are higher in China, while trust in strangers is lower.4 Much of the social credit system is geared towards addressing widely perceived problems such as fraud and cheating in China. This makes a policy framework to mitigate these problems more appealing.

- Censorship in China prevents people from seeing potential pitfalls to government projects. Moreover, the PRC government has been heavily promoting positive stories about the social credit system and the problems it is meant to solve.5

To test whether culture can explain the gap, a look at China’s neighbor, Taiwan, canhelp. While culturally definitely much closer to China than to Germany, Taiwan is a vigorous democracy with a free press. How do Taiwanese view the social credit systems? Exhibit 1 shows the average view of the four proposals for respondents in Taiwan, Germany and China. We see that respondents from Taiwan fell in between respondents from Germany and China. Translated into grades from A to F, Germans would award the proposals a D, Taiwanese would give a C–, and Chinese a C+. Cultural differences would therefore seem to play a role,6 but they cannot fully explain why PRC citizens not more negative about social credit systems.

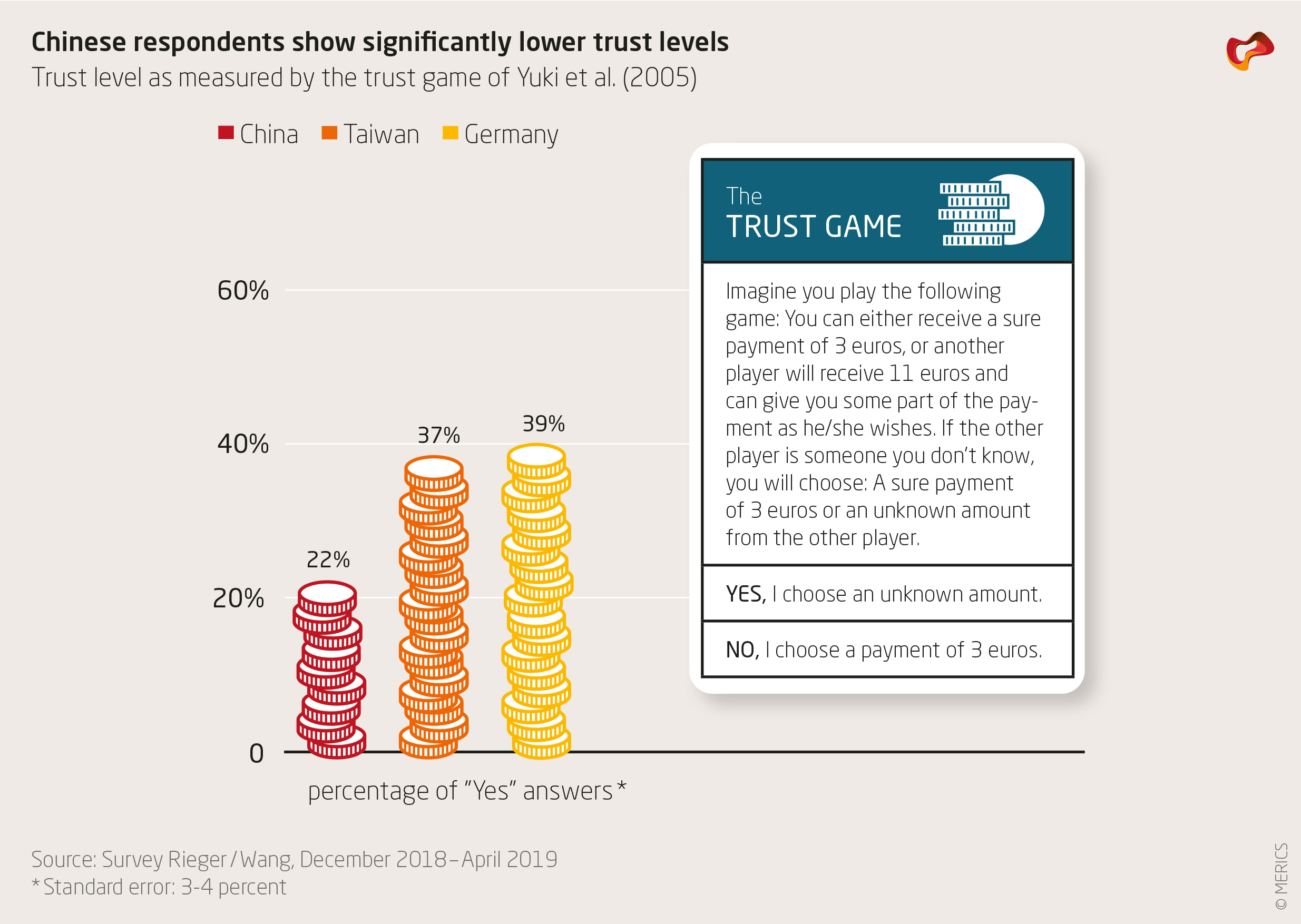

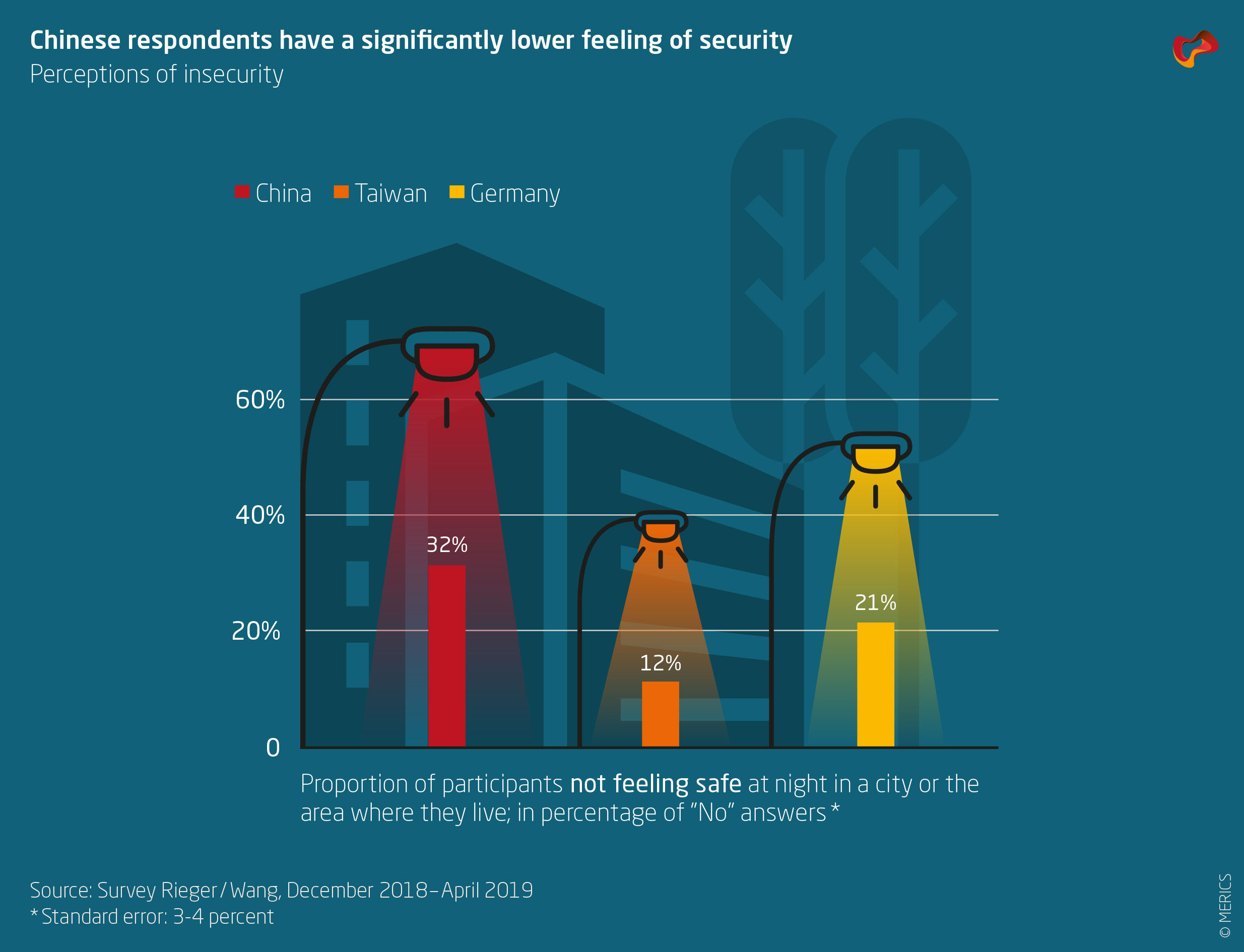

One possible explanation is that Chinese are more concerned about lack of trust and public safety. In our survey, we also elicited trust in strangers (using a trust game)7 and asked questions about perception of personal safety (“Do you feel safe alone at night in a city or the area where you live?”).

China-based respondents showed significantly lower trust levels compared to German or Taiwanese respondents. They also significantly felt less safe. It is conceivable that higher concerns in China (whether or not they are based on actual dangers) lead people to rank the benefits of social credit systems more highly and judge them more positively.

Censorship in the PRC provides another possible explanation for the higher approval ratings. We tested this possible explanation in two ways: first, we elicited what participants thought was the overall opinion of media on social credit systems. The most striking observation was that the percentage of participants who had “never seen or read anything about this [i.e. the various measures within the social credit framework] in the media” was highest in China: 30 percent. One would expect this percentage to be the lowest in the country where these proposals are actually being implemented. In Taiwan, 29 percent had never heard about it, but in Germany, only 15 percent stated they had never seen the social credit system mentioned in media.

Initially, we might have ascribed this to the German media’s emphasis on data protection topics. However, among the 142 respondents from countries outside China, Taiwan and Germany, only 16 percent had never heard of China’s social credit system – a similar proportion as among Germans.

The surprising lack of information among students in the PRC could be explainable by factors other than censorship, e.g. Chinese university students focusing more intently on their studies and have less time to follow the news. Similar academic pressures could explain why Taiwanese students did not see much of the topic in the media. However, where Chinese respondents had read media reports on the social credit system, those reports were on average considered to be more positive than news reports seen that Taiwanese or Germans had seen.

A second test revealed the impact of censorship (or more general a media bias) more directly: After being exposed to information on the potential benefits and dangers of social credit systems, we asked the subjects once more to judge proposal 3, i.e. an aggregated individual score based on a range of behaviors. In Taiwan, the judgment did not change and in Germany it was slightly more positive.8 Chinese respondents adjusted their opinion substantially downwards: instead of 53 percent, now only 29 percent thought about the project as “positive” or “very positive” (Exhibit 4), in other words, very little information, presented in an intentionally neutral way, can change opinions tremendously. This suggests that the information level before was low. The most likely cause of this is censorship and selective coverage: As previous studies have shown, Chinese media focuses predominantly on the positive aspects of the social credit system and its problem-solving potential.9 In addition, discussion of the topic has been censored on Chinese discussion platforms.

5. Conclusion: Awareness leads to less acceptance of social credit

To sum up, the social credit framework is not uncontroversial in China, though respondents there showed a higher acceptance of it than in Germany. The difference can be explained by a mixture of cultural differences; widespread worries in the PRC about safety and trust; and censorship, which has prevented PRC citizens from reading about the potential dangers of the new social credit framework. However, once they become aware of associated risks, they showed substantially less acceptance.

More research on the public perception of social credit in China is needed, especially as new measures are continuously rolled out and the framework touches more and more people’s lives. Such research might include public opinion on other measures within the social credit policy framework, including how people perceive policies that implicate the family or friends of a “social credit offender” who may also have their scores affected.

Overall, we believe it likely that the social credit initiative will receive a more positive evaluation in China than in Germany or other European countries. However, this survey’s preliminary findings show that the picture is more complex than previously thought. While cultural factors may contribute to a somewhat wider acceptance of the policy, no easy generalizations are possible.

- Endnotes

-

1 | Genia Kostka (2019): “China’s social credit systems and public opinion: Explaining high levels of approval,” New Media & Society, in press. Also see Genia Kostka (2018): “China’s social credit systems are highly popular – for now,” MERICS blog, 17 September 2019,

https://www.merics.org/en/blog/chinas-social-credit-systems-are-highly-popular-now.

2 | Mareike Ohlberg, Shazeda Ahmed, Bertram Lang (2017): ”Central planning, local experiments– The complex implementation of China’s Social Credit System,“ MERICS China Monitor, 12 December 2017.

3 | G. J. Hofstede, and Michael Minkov (2010), Cultures and organizations: software of the mind, McGraw-Hill Education, 3rd edition.

4 | Fearfulness of crime has already been found to be at high levels in China, e.g., by Yuning Wu and Ivan Y. Sun (2009), “Citizen Trust in Police the Case of China”, Police Quarterly, 12(2), 170-191. For the three items of crime, terrorism and illegal drugs abuse, Chinese stated on average for 2.55 of them that they “caused great worry”. The comparatively low trust level in Chinese society towards outsiders (i.e. people outside family and friends) has been studied, e.g. by Jan Delhey, Kenneth Newton, and Christian Welzel (2011), “How General Is Trust in `Most People’? Solving the Radius of Trust Problem”, American Sociological Review 76(5), 786–807.

5 | Mareike Ohlberg, Shazeda Ahmed, Bertram Lang (2017): ”Central planning, local experiments – The complex implementation of China’s Social Credit System,“ MERICS China Monitor, 12 December 2017.

6 | The cultural differences may not necessarily lie between East Asia and “the West”, as Germany is well-known to put a surprisingly large emphasis on data protection, see Sabine Devins (2017): Why Germans are so private about their data, Handelsblatt, 10 February

2017.

7 | In a “trust game”, people are asked how much of a certain amount they would give to another person if this amount gets tripled and the other person can freely decide how much (if any) of it to return. Masaki Yuki, William W. Maddux, Marilynn B. Brewer, Kosuke Takemura (2005): Cross-Cultural Differences in Relationship- and Group-Based Trust, Personality and Social Psychology Bulletin, Vol. 31:1, pp. 48-6.

8 | Pointing towards a possible German media bias in favor of data protection.

9 | Mareike Ohlberg, Shazeda Ahmed, Bertram Lang (2017): ”Central planning, local experiments – The complex implementation of China’s Social Credit System,“ MERICS China Monitor, 12 December 2017.

Author(s)

Author(s)

Content