picture alliance / ZUMAPRESS.com | Ren Yong

Tracker

China Economic Indicators

The post-Covid recovery disappoints in Q2

MERICS Economic Indicators Q2/2023

Q2 analysis: China’s economic recovery is looking fragile despite higher growth in Q2

China’s economy continued to struggle for momentum in 2023, disappointing hopes for a strong rebound after protracted Covid-19 lockdowns. Although GDP expanded by 6.3 percent in Q2, the relatively high growth data was largely due to base effects, as growth in the same three months of 2022 was a mere 0.4 percent. Weak demand has also put the economy on the verge of deflation. The initial optimism about the strength of the recovery of China’s economy has subsided.

China’s Q1 performance led to initial optimism which has begun to wane. Growth forecasts from prominent investment banks have proved overly optimistic, prompting downward revisions. Annual GDP growth was widely projected at around 6 percent but the revised forecasts hover closer to 5 percent, as the tough path for any sustained recovery has become clearer.

Weak household spending continues to limit the recovery, though services and travel-related sectors showed signs of improvement in Q2. But persistent worries about employment and earnings prospects have cast a shadow on household spending. In addition, record levels of youth unemployment are a pressing challenge for the government. It is becoming apparent that the rebound is not generating the white-collar jobs university graduates are seeking. The stress on families ripples far beyond the students themselves to impact sentiment in large parts of the middle class.

Restoring household sentiment cannot happened at the switch of a button. The lasting impact of a combination of zero-Covid measures, regulatory crackdowns and geopolitical risks have hit confidence. This makes it challenging for the government to shore up demand. Much more ambitious economic policy focused on stimulating consumer demand including expansive fiscal policy or tax breaks for households would be necessary.

During Q2, several other key sectors – not only retail – fell short of analysts’ expectations. The real estate market has yet to recover from the 2022 regulatory crackdown, and industrial output softened, including export demand. Sluggish growth is building pressure on the government to provide more economic stimulus measures. It has already resorted to its well-worn playbook of more investment in transportation infrastructure while the central bank is likely to unveil more monetary support, potentially through key rate cuts.

The government is struggling to find the optimal policy direction to improve sentiment and stimulate the economy. The aftershocks of 2022 – domestic and international - continue to leave their mark on the economy, creating a delicate situation as the recovery remains fragile and uncertain. It will be crucial to watch for policy decisions and how they impact sentiment and economic performance in the months ahead.

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 1

The MERICS China Confidence Index (MCCI)

The MERICS China Confidence Index measures household and business confidence in future income and revenues. The index is weighted between household and business indicators. It includes the following indicators: stock market turnover, future income confidence, international air travel, new manufacturing orders, new business in the service sector, urban households’ house purchase plans, venture capital investments, private fixed asset investments and disposable income as a share of household consumption. All components have been tested for trends and seasonality.

The MCCI was first developed in Q1 2017.

The MERICS China Confidence Index measures household and business confidence in future income and revenues. The index is weighted between household and business indicators. It includes the following indicators: stock market turnover, future income confidence, international air travel, new manufacturing orders, new business in the service sector, urban households’ house purchase plans, venture capital investments, private fixed asset investments and disposable income as a share of household consumption. All components have been tested for trends and seasonality.

The MCCI was first developed in Q1 2017.

Macroeconomics: GDP growth disappoints amid weak recovery

Exhibit 2

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 3

- Optimism about China's post-Covid recovery has waned since the first quarter, as initial growth projections of approximately 6 percent by major investment banks have been downgraded for 2023 (see exhibit 2). Although China is expected to meet its GDP growth target of 5 percent, this seemingly modest goal has become increasingly demanding to achieve.

- Although China’s GDP growth bounced back in Q2, expanding by 6.3 percent, the economy is facing major headwinds. The recovery is struggling to gain pace with the improvement in Q2 in large part attributed to low growth in the reference period last year.

- The Q2 rebound in GDP growth is likely to be a one-off as the impact of low base effects will subside in the coming quarter. A more reliable indication of things to come was seen in quarter-on-quarter growth, which was 0.8 percent in Q2, down from 2.2 percent in Q1 (see exhibit 3).

- As anticipated, the service sector was the primary driver of growth, expanding by 7.4 percent in Q2 compared to 5.4 percent in Q1. Despite the strong base effects, the sector’s growth was only marginally approaching pre-pandemic levels seen in 2018 and 2019, when growth rates ranged between 7 and 8 percent. The recovery in services and consumption is too weak to compensate for slowdowns critical areas including manufacturing and real estate.

What to watch: Without a major government stimulus effort, China’s growth outlook remains dim for 20 Without a major government stimulus effort, China’s growth outlook remains dim for 2023.

Business: China's industrial rebound stalls amid weak domestic demand

Exhibit 4

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 5

- Industrial production in June was lackluster, with only 4.4 percent year-on-year value-added growth. China’s manufacturing sector was hurt by deflationary pressure and sluggish demand. Value-added growth for manufacturing climbed to just 4.8 percent in June, and to 4.2 percent for H1 2023. The brief rise to 6.5 percent in April was primarily driven by base effects rather than sustainable momentum.

- State-owned enterprises helped prop up growth in June, expanding by 5.4 percent. However, foreign-owned enterprises contracted of 1.4 percent, influenced by diminishing growth in automotives, outside new energy vehicle (NEV) sector, and in the consumer electronics industry.

- The production of microchips, smartphones and industrial robots in absolute terms declined by 24.9 percent, 4.1 percent and 12.1 percent respectively in June. This negative trend in high-tech products was due to weak local demand as well global electronics downcycle.

- China’s official Manufacturing Purchasing Managers’ Index (PMI) reflected negative sentiment among producers as it dropped below 50 in April and finished at 49.0 in June. Values below 50 indicate pessimism. After reaching an all-time high of 56.9 in March, China’s Services PMI has declined three months in a row but still ended in positive territory at 52.8 in June.

- China’s growth drivers included a surge in value-added output in chemical raw materials and non-ferrous metal processing, up 9.9 percent year-on-year, and 9.1 percent in June. Electrical machinery and equipment also saw sustained growth, up 15.4 percent. Although unit output in China's NEV sector continued to grow at 27.6 percent in June, it marked the slowest rate in three years, leaving behind triple-digit growth.

- Construction materials, including cement, plate glass and crude steel, displayed near-zero or negative value-added growth in Q2 2023, on top of already negative growth in Q2 2022. This was due to ongoing government-led constraints on the real estate sector and infrastructure spending.

What to watch: The Chinese government’s restraint in providing stimulus means industrial output overall will remain suppressed in the foreseeable future.

International trade and investment: Fragile recovery lacks import growth and exports are starting to falter

Exhibit 6

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 7

- China's economic recovery has not yet boosted import demand. Imports have contracted every month with the exception of February in 2023, so far. As a result, imports measured in USD fell by 6.7 percent in the first half of the year. This highlights the ongoing challenge of strengthening domestic demand and the limited impact of the recovery on global markets.

- The downturn in the global electronics sector, a crucial driver of China's manufacturing and export industries, has been a big factor in the weak import figures. Notably, the demand for essential electronics components contracted by 17.5 percent, while imports of integrated circuits fell by 22.4 percent during H1 2023. The weak data underscores the challenges facing China's export-oriented manufacturing sector in the coming months.

- The ability to rely on exports as a key support for China’s economy appears to be waning due to slower economic growth and higher inflation in major markets. Export figures measured in USD terms sharply contracted by 3.2 percent in the first half of the year. The slowdown was particularly pronounced in June, with a sharp decline of 12.4 percent. The slowdown is expected to continue in the coming quarters, suppressing economic growth further.

- ASEAN expanded its position as China's most important export destination. Exports to the region now account for 15.8 percent to China’s total exports, ahead of the EU (15.5 percent) and the United States (14.4 percent). It was also the only major region to see growth in Chinese exports, which were up by 1.5 percent in H1 year on year (see exhibit 6).

- China's vehicle exports have become increasingly significant. In H1, China exported 2.1 million vehicles, a new record. Chinese brands are actively seeking a presence in international markets with strong demand for EVs being a key factor. But Tesla has also played a prominent role as a major exporter of vehicles from China (see exhibit 7). If the trend continues, China is on track to become the world's largest vehicle exporter.

What to watch: Exports are likely to come down further from the elevated levels achieved over the past two years.

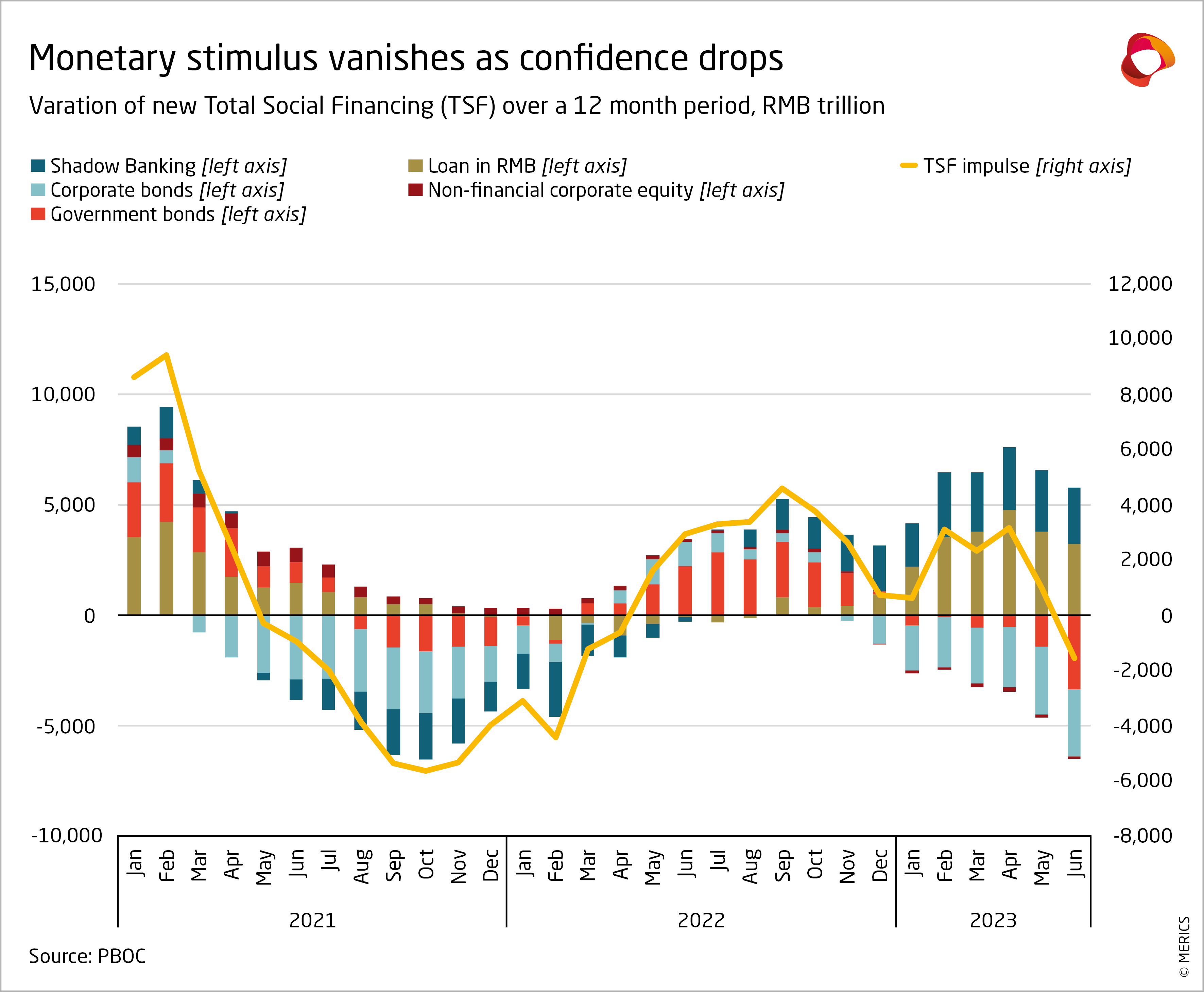

Financial markets: More monetary policy is being rolled out to support weak rebound

- China’s central bank has until now avoided a massive stimulus package that might undermine progress in de-leveraging. But weak economic growth and deflation are building pressure for looser monetary and fiscal policy. In June, the People’s Bank of China (PBOC) softened its position somewhat, announcing more stimulus measures as previous ones had not proved sufficient to support the economy.

- The shift in monetary policy meant rates were lowered by 10 basis points in June, and new lending quotas were set for SMEs. Commercial banks have also cut deposit rates, setting the stage for more monetary easing in the coming quarter.

- Financial flows to the real economy lost dynamism, weakening in June to 9.3 percent growth year on year from 10.3 percent in March (see exhibit 8). New loans to households fell to their lowest level since late 2021, reflecting the entrenched loss of confidence in real-estate.

- New long-term loans to companies over the quarter were 33 percent higher than in Q2 last year, but growth had slackened from 69 percent in Q1 and 168 percent in Q4 2022. Fewer short-term loans are another sign of rising risk-aversion among firms, down 12 percent from Q2 last year.

- The performance of China’s stock markets also reflected weak sentiment. After a good start in April, the two main boards of Shenzhen and Shanghai eventually lost 3.6 and 2.2 percent over the quarter. Plummeting investor confidence caused total stock market capitalization to lose more than 1.6 trillion yuan in value.

- Foreign investors seem to have taken a similarly gloomy view, after initial optimism. Modest positive inflows into Chinese stocks in early 2023 were completely reversed, with outflows of 69 billion yuan over Q2.

What to watch: Monetary policy adjustments will be a tricky balancing act for the new head of the PBOC – Pan Gaosheng – as local government debt troubles and pressure on the exchange rate are rising.

Investment: Investment slowdown is spreading amid weak sentiment

Exhibit 10

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 11

- Investment activity in China reflects a struggling economic recovery and weak sentiment (see also exhibit in retail). Despite cautious stimulus measures, investor sentiment remains weak; Investment growth dipped from 5.5 percent in February to 3.8 percent for the first half of 2023, its lowest growth since December 2020.

- The private sector saw a further deterioration in growth, as investment contracted for the first time since October 2020 (see exhibit 10). By the end of June, investment was down by 0.2 percent, compared to a 0.6 percent rise at the end of March. The slowdown is primarily due to sluggish activity in the service and real estate sectors.

- The real estate sector has now contracted for 15 consecutive months and its persistent weakness continues to drag down overall growth. Despite government efforts to restore confidence, the situation worsened in Q2, with a year-to-date contraction of 7.9 percent, compared to 5.8 percent at the end of Q1. The real estate sector’s economic weight means its prolonged weakness presents a significant challenge for the government as other sectors are not strong enough to balance things out.

- Investment in manufacturing continues to be a bright spot although growth has gradually slowed over the past two years, to 6 percent in H1 2023. Notably, investments in the automotive and electrical machinery sectors continue to grow at record levels (see exhibit 11). Given that double-digit growth has been going on for more than 2 years in both sectors, a slow-down in these rates is only a question of time.

- Infrastructure investment continued to out-perform overall investment, but slowed to 7.2 percent at the end of June, down from 8.8 percent at the end of March. This was mainly due to base effects when the data is set against the accelerated growth seen in the same period last year. The expansion of the railway network has played a key role, with growth reaching 20.5 percent in the first half of 2023. However, the government's cautious stimulus measures in infrastructure investment are not enough to counter the broader economic slowdown.

What to watch: The effectiveness of the government’s stimulus measures hinges on a rebound in the private sector.

Prices: Deflationary pressure increases as prices fall across the board

Exhibit 12

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 13

- China’s economy is at risk of a deflationary spiral that could impact profits, wages, and debt servicing. Both consumer prices (CPI) and producer prices (PPI) are on a downward trend, posing challenges for the government as it tries to revitalize the economy. It could face growing pressure to find ways to stimulate sluggish demand.

- Continuous falls in commodity prices played a major role in curbing consumer and producer prices. Fuel prices for consumers dropped 17.3 percent in April year on year, while producer input prices for fuel and power contracted by 11.1 percent year on year. Some of these falls are due to base effects from price spikes in 2022. As these wear off, price falls are expected to weaken in the second half of 2023.

- The underwhelming recovery in consumption since Covid lockdown restrictions ended exacerbates the risk of deflation in the third quarter. In Q2, the Consumer Price Index (CPI) fell from 2.1 percent in January to zero in June. Households may delay making purchases as they await further price falls, a trend already evident for durable goods, such as household appliances (see exhibit 12).

- Prices for travel related services, which were especially hard hit during the pandemic, also began to ease after a sharp jump in Q1: the sector’s prices dropped back from a rise of 9.4 percent in April to 6.4 percent in June, as the industry, including transportation firms, added additional capacity.

- Producer prices continue to be pushed down by weak domestic and international demand. The Producer Price Index (PPI) has been contracting since September 2022, suggesting entrenched deflationary conditions. In Q2, the situation deteriorated further as the PPI contracted by 5.4 percent –the most significant decline since the global financial crisis in 2009.

- Real estate prices remain crucial in shaping overall market sentiment. Prices fell due to a weak economy and the government's crackdown on the sector in 2022. Prices in secondary cities were especially hard hit and are only slowly recovering (see exhibit 13).

What to watch: The government will need to significantly shore up sentiment and demand to avoid deflation.

Labor market: University graduates struggle to find jobs in lackluster economy

Exhibit 14

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 15

- In Q2, the Chinese labor market faced a challenging landscape as it grappled with the aftermath of the Covid-19 pandemic and sought to reignite economic growth. Despite modest improvements in overall employment, the recovery proved sluggish, hindering robust rebound in jobs.

- In the first six month a total of 6.8 million new urban jobs were created, up by 3.7 percent compared to the same period in 2022. While this marks an improvement, job creation is still well below the 7.3 million jobs which were created in the same period on average in the five years prior to the pandemic (2015-2019). The ongoing shortfall in job creation means job seekers will continue to struggle.

- Both job seekers and existing workers face the prospect of stagnant or slow wage growth, and therefore heightened economic uncertainty (see exhibit 14). Slow wage growth is likely to further dampen consumer confidence and hamper overall economic recovery efforts.

- Unemployment declined slightly, dipping from a peak of 5.6 percent in February to 5.2 percent in June. However, unemployment has fallen significantly from the pandemic-induced peak of 6.2 percent in April last year, during the widespread Covid lockdowns in Shanghai and other cities in Q2 2022.

- Youth unemployment reached an all-time high of 21.3 percent in June, up from 19.6 percent at the end of the previous quarter in March. A record cohort of 11.6. million fresh graduates will face the daunting challenge of securing suitable employment as they enter the labor market this summer.

- The government is trying to address the issue by launching a nationwide “100-day sprint” to improve employment. Measures include online recruitment campaigns, an “employment service drive” to support job seekers and help with starting new businesses aimed at unemployed youth and recent graduates. However, it remains to be seen if these measures will be effective in easing the pressure on China’s youth.

What to watch: Youth unemployment would need to come down significantly to alleviate the social pressures arising from the sluggish labor market.

Retail: Rebound in consumption is not strong enough to lift the economy

Exhibit 16

![]() Hover over/tap the chart to see more details.

Hover over/tap the chart to see more details.

Exhibit 17

- Chinese household sentiment remains cautious in the second quarter of 2023, as reflected by the PBOC's bank depositors' index. Despite a slow improvement in consumption, the inclination towards saving is significantly higher than pre-pandemic levels (see exhibit 16). For China's economic recovery to gain momentum, a substantial improvement in sentiment is necessary.

- The government is struggling to shift stimulus measures towards consumption. Local government support such as handing out vouchers and spending subsidies are largely symbolic with little economic impact. Consumption is still not the mainstay of stimulus measures which focus more on investment and support for companies.

- Although consumption growth expanded by 8.2 percent in the first half of the year, the figures mask underlying weaknesses. The growth was largely influenced by base effects, as China had extensive lockdowns during the same period last year. Furthermore, signs of a diminishing rebound are already emerging, as June recorded the sharpest monthly drop in growth since the onset of the pandemic (see exhibit 17).

- Spending on food and beverages as was 14 percent above levels in H1 2019, with growth reaching 21.4 percent in the first half of this year. But the overall impact on consumption growth is likely to moderate as the hard-hit restaurant sector is returning to pre-pandemic levels.

- Vehicle sales contracted by 1.1 percent in June year on year, down from 38 percent growth at the start of the quarter. The slowdown was in part explained by base effects but also reflects households holding back on spending on big ticket items. In response, the government has announced purchasing tax exemptions for EVs purchased in 2024 and 2025.

- Domestically, households are returning to pre-pandemic travel levels. However, it is a different story for international travel. For example, domestic passenger volume reached around 95 percent of the H1 2019 levels, whereas international travel is only reached levels of under 20 percent.

What to watch: A more substantial shift towards aiding consumption could require tax breaks and interest rate cuts targeted for consumption.

Author(s)

Former Chief Economist

Former Senior Economist (Brussels office)

Senior Analyst, Rhodium Group and former Analyst, MERICS

Senior Analyst

Author(s)

Former Chief Economist

Former Senior Economist (Brussels office)

Senior Analyst, Rhodium Group and former Analyst, MERICS

Senior Analyst