picture alliance / CFOTO

Comment

DeepSeek’s success masks China’s weakening innovation model

China is turning away from a private-led system, with venture capital investment now lower than in Europe, says Jeroen Groenewegen-Lau.

DeepSeek’s world-beatingly efficient AI chatbot, dancing robots on China’s most-watched TV show and a trillion CNY (127 billion EUR) in state support for the private sector have rekindled optimism among and about the country’s tech start-ups. Such good news is balm for an industry that has been battered over the past half-decade by Beijing’s regulatory crackdown, China’s weak economic growth and the US’s tech and trade war. But it cannot mask the challenges facing China's state-led innovation model – not least the retreat of foreign direct investment.

China’s venture capital (VC) has been declining since 2021 and dropped another 32 percent year-on-year to 33 billion USD in 2024, according to the investment website Crunchbase. This means that China's inbound venture capital was just one-fifth the size of the 178 billion USD invested in US companies – and even lagged behind the 51 billion USD flowing into a sluggish European market. What a difference five difficult years can make: China’s VC market was one and a half times larger than Europe’s in 2020, but only two thirds the size in 2024.

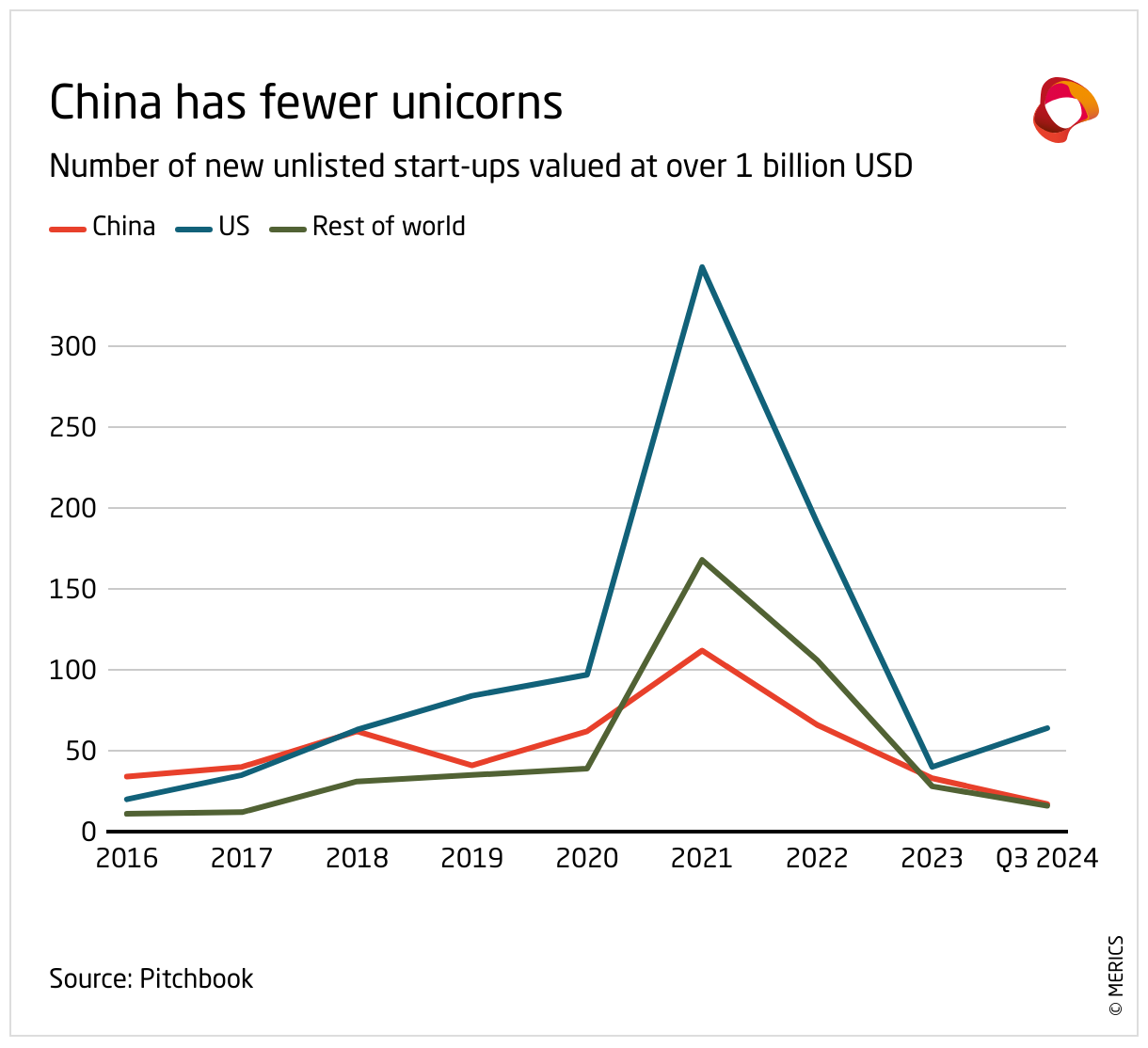

Dissapearing unicorns

The first generation of turn-of-the-millennium tech companies, such as Baidu, Alibaba and Tencent, were followed a decade or so later by a raft of second-generation companies, such as ride-hailing firm Didi, fast-fashion platform Shein and TikTok-owner Bytedance. But the frequency and intensity of the emergence of new tech giants has noticeably declined in the 2020s. China was by 2024 producing about two new unicorns – companies worth 1 bn USD or more – a month – twice the rate of Europe, but only 40 percent the rate seen in the US.

Declining foreign direct investment in China is a key driver of this trend. The first generation of Chinese unicorns attracted foreign venture capitalists – and invaluable advice on how to scale up – as they sought to list on US exchanges, offering their early-stage investors a lucrative exit. But Beijing has insisted since around 2020 that strategic tech companies must be Chinese owned – effectively scuttling Didi’s US listing in 2021 – and Washington in 2025 banned US VCs from investing in Chinese AI, semiconductors and quantum computing.

President Xi Jinping is aware of the challenge facing the technology sector. In 2024, he asked “why do we have fewer new unicorns?”, and every major political event since then has heard a call to “invest early, small, long-term and in hard sciences”. Beijing wants its banks, sovereign wealth funds and state-owned enterprises (SOEs) to fill the gap left by private investors. SOEs controlled by the central government in 2024 put 40 percent of investments into emerging technologies, five percentage points more than in 2023, and Beijing this year pledged one trillion CNY (127 billion EUR) for a government fund for emerging and future industries.

Beijing argues that seed investment from SOEs and the new fund will help attract many times more funding from the private sector. But they will also further increase the role of the state in the economy. This is, of course, entirely in character – the online response to Xi’s question about why there are fewer unicorns was simply “because of you, Chairman”. Since becoming head of the Chinese Communist Party in 2012 and head of state in 2013, Xi has consistently promoted the advantages of SOEs and party-state control over the economy.

State-led investment

As long as the state – rather than private entities subject to the free play of market forces – decides which companies develop which products and technologies, follow which development path and choose which partners, China’s economic contradictions will only grow. Despite years of government campaigns, private companies will continue to struggle to access loans and capital, while so-called government guidance funds will continue to allocate resources based on political considerations, with many projects failing to advance innovation, let alone its productivity. The number of tech unicorns will continue to decline.

These challenges have been eclipsed for now by DeepSeek and the other so-called “six little dragons of Hangzhou” – the AI-focused startups Game Science, Unitree, DeepRobotics, BrainCo and ManyCore. But the question is for how long? All of these companies have benefitted from China’s innovation policies, but they did not emerge through state procurement or government guidance funds – DeepSeek, for example, has primarily been funded by the hedge fund set up by DeepSeek chief executive Liang Wenfeng, not by Beijing.

For China to produce the next Alibaba, it should dial down its techno-nationalism, with its state-led approach to technology development. It needs to find its way back to the more inclusive and international investment climate of previous decades, in which entrepreneurs and private investors could thrive. But, despite Xi’s longing for more unicorns, there is no reason to expect China change course. The more likely outcome is more dancing robots at the next Spring Festival’s TV extravaganza. This will please the crowds but will do little to revive China’s start-up scene.

This article was first published by Science Business on April 3, 2025.

Author(s)

Lead Analyst

Author(s)

Lead Analyst