Report

Chinese investment rises to 7-year high - Chinese FDI in Europe: 2025 Update

Report by Rhodium Group and MERICS

Key findings

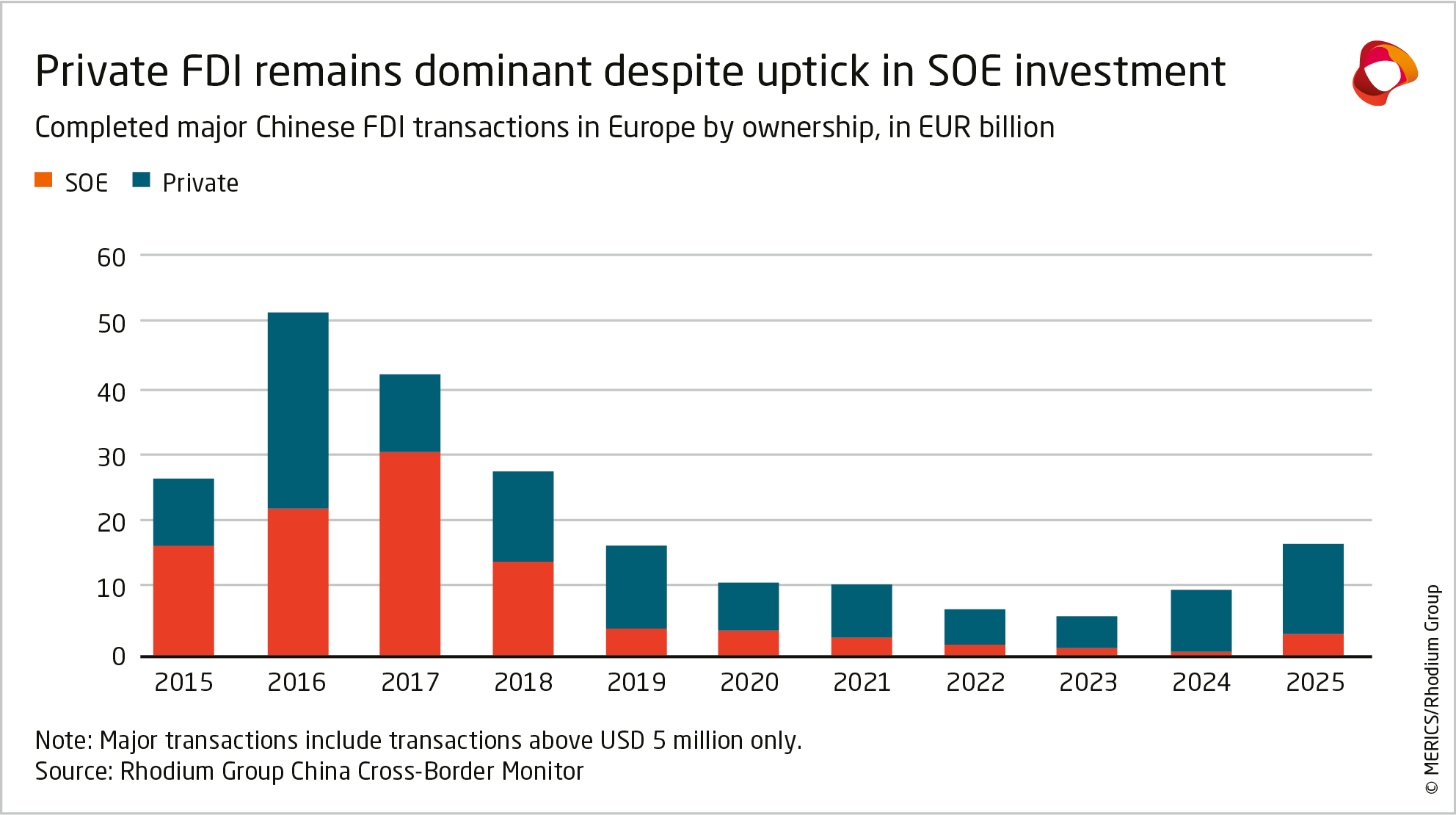

- Chinese foreign direct investment (FDI) in Europe (EU and UK) rose for the second consecutive year, reaching its highest level since 2018. It increased by 67 percent to EUR 16.8 billion in 2025. M&A activity drove the rebound, rising 89 percent year-on-year to EUR 7.9 billion. But greenfield investment remained the primary channel for Chinese FDI in Europe, increasing by 51 percent to a record EUR 8.9 billion. Europe made up nearly a quarter of global Chinese FDI in 2025, up from 17 percent in 2024.

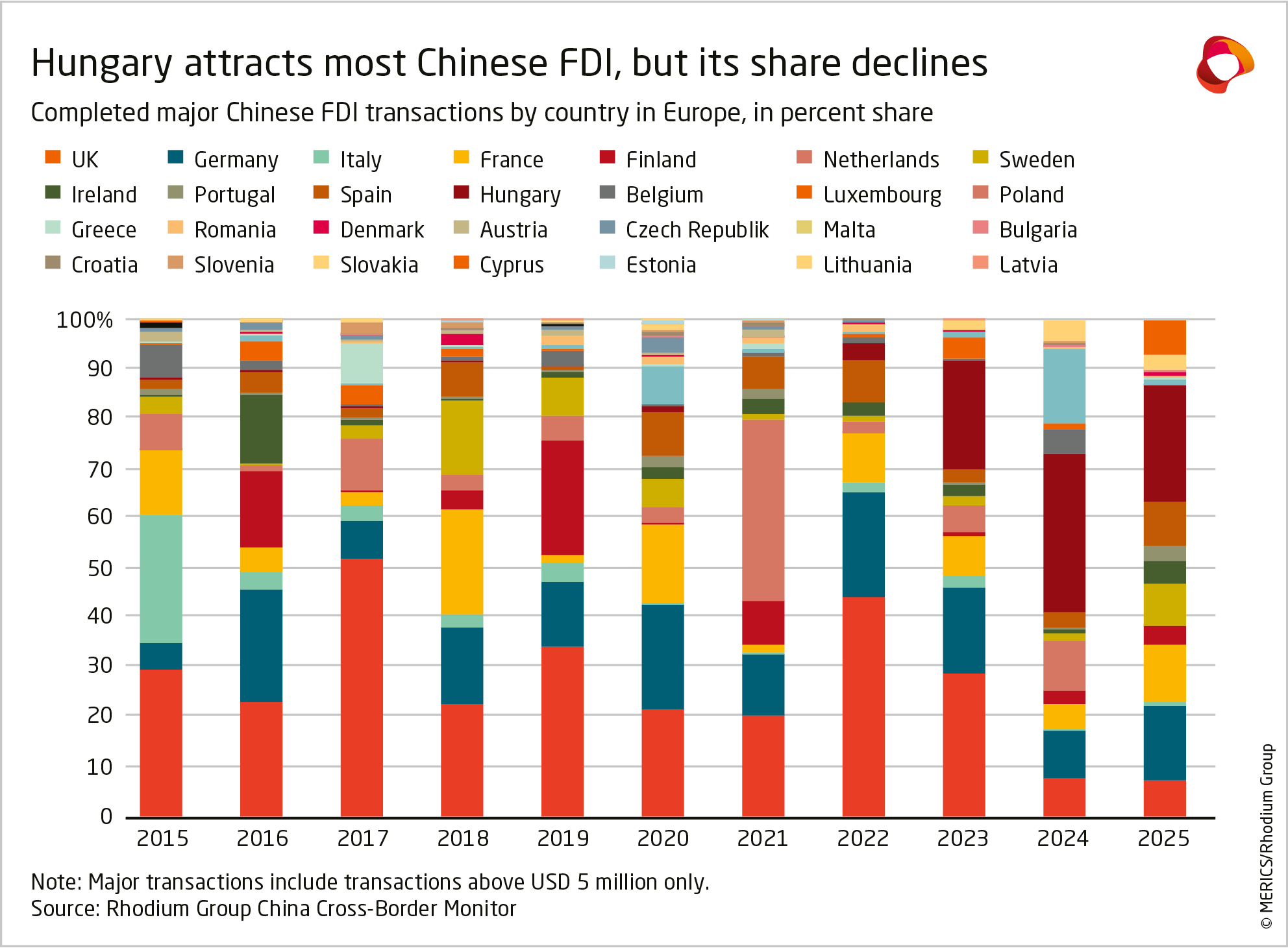

- While Hungary remains the primary destination for Chinese FDI in Europe, more investment is once again flowing into Germany and France. Hungary attracted Chinese investments worth EUR 3.9 billion in 2025, up from EUR 3.2 billion in 2024. Germany (EUR 2.5 billion) and France (EUR 1.9 billion) ranked second and third. Germany’s share of total Chinese FDI in Europe rose to 15 percent from 10 percent in 2024, while France’s increased to 12 percent from 5 percent.

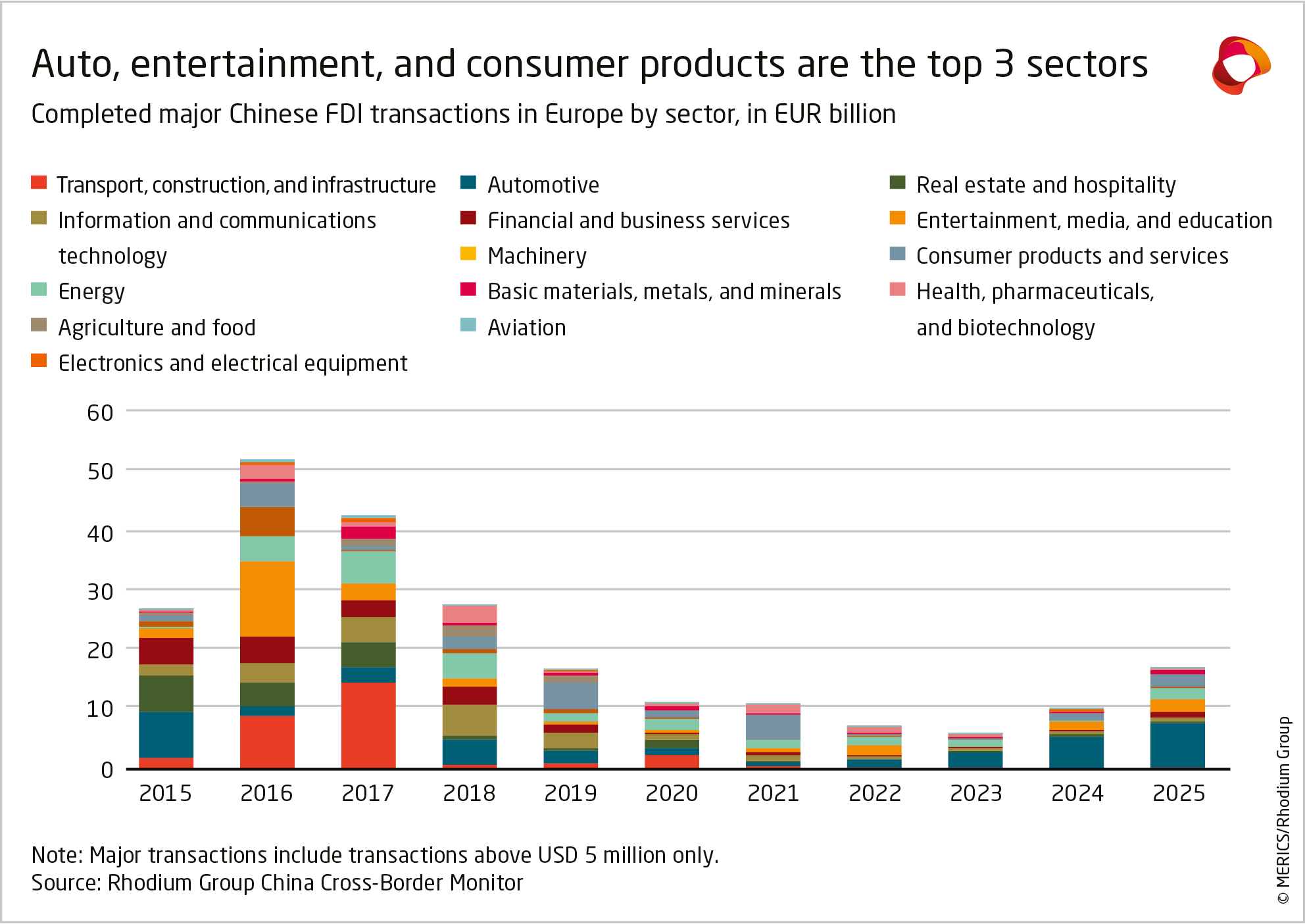

- The automotive sector attracted more Chinese FDI in 2025 than any other industry. Investments in the sector totaled EUR 7.6 billion, with 93 percent of them focused on the EV supply chain. The auto sector’s share of total Chinese FDI in Europe stood at 45 percent, down from 52 percent in 2024. The entertainment sector ranked second, pulling in EUR 2.3 billion or 14 percent of the total, followed by consumer products and services at EUR 2 billion or 12 percent.

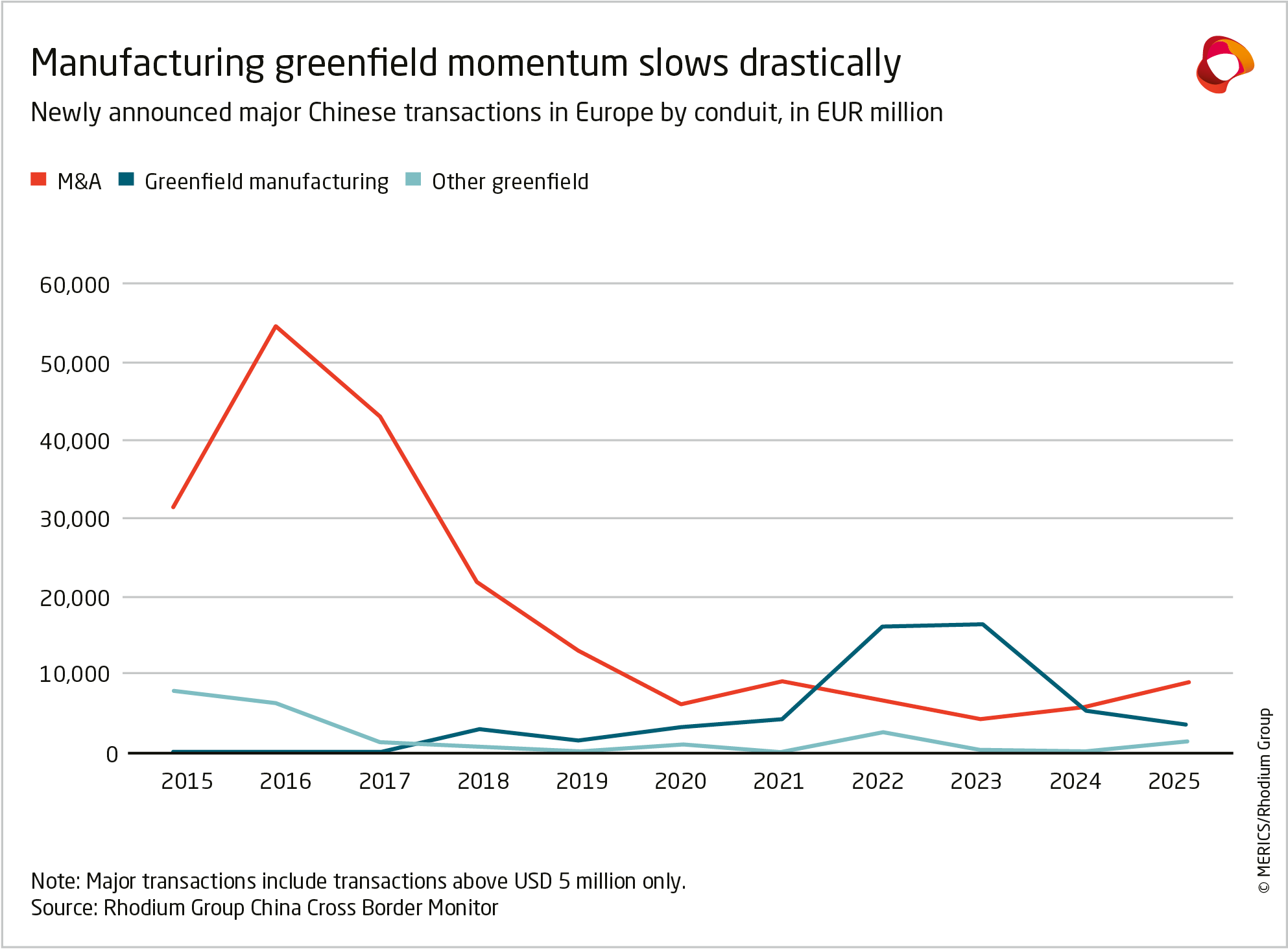

- Although completed greenfield investment reached a new peak in 2025, a decline in the value of newly announced transactions points to slowing greenfield momentum in the years ahead. In 2025, just EUR 5.2 billion in new Chinese investments in plants and equipment were announced, down from EUR 5.7 billion in 2024 and a steep drop from EUR 16.9 billion in 2023.

- While Chinese greenfield investments are poised to slow, exports to Europe continue to rise, underlining the increasing threat to European industry. Chinese goods exports increased by 9 percent in 2025 in value terms, with particularly strong growth in sectors that had previously attracted significant Chinese FDI. Battery exports to Europe increased by 43 percent, auto exports rose by 15 percent (and by 29 percent in volume terms) and wind equipment exports surged by 65 percent.

- Going forward, Beijing’s focus on building up domestic industrial capacity and keeping core technologies and know-how at home will continue to weigh on outbound foreign direct investment (OFDI). Meanwhile, persistently weak domestic demand and low profit margins in China, as well as an undervalued yuan, will encourage Chinese firms to continue to use exports as the main channel for selling their goods abroad.

1. Chinese investment in Europe surges to highest level since 2018

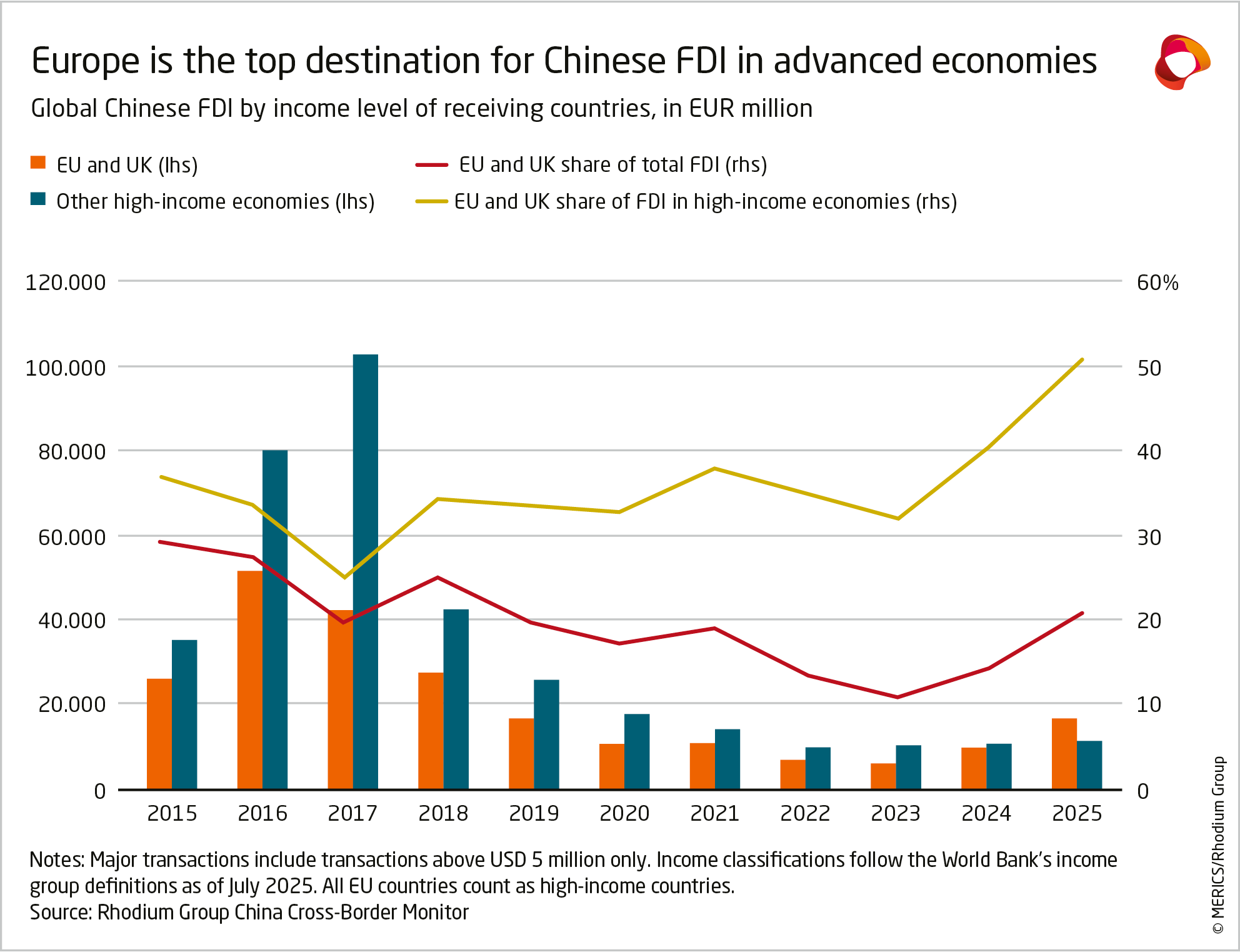

1.1 Europe has become the top destination for Chinese FDI in advanced economies

Chinese global overseas foreign direct investment (OFDI) increased by 18 percent year-on-year, reaching EUR 69 billion in 2025.1 It was the third consecutive year of growth in OFDI since 2023. Nonetheless, overall levels remain subdued at around 38 percent of the 2017 peak (EUR 182 billion). Chinese firms’ rising competitiveness in higher value-added sectors is supporting greenfield expansion. But tight capital controls in China and heightened regulatory scrutiny in destination markets continue to keep M&A activity in check.

Since 2024, investment in the EU and UK has been a key driver of the rebound in global Chinese FDI. The region’s share of total investment has continued to rise, from 17 percent in 2024 to nearly a quarter in 2025. Among high-income economies, the EU and UK now account for around 60 percent of total FDI. Chinese investment in other advanced economies has stagnated at EUR 10–11 billion annually since 2022, with the US flatlining at a decade-low of around EUR 3 billion. The divergence reflects the size and relative openness of the European market, particularly in consumer sectors and clean technologies.

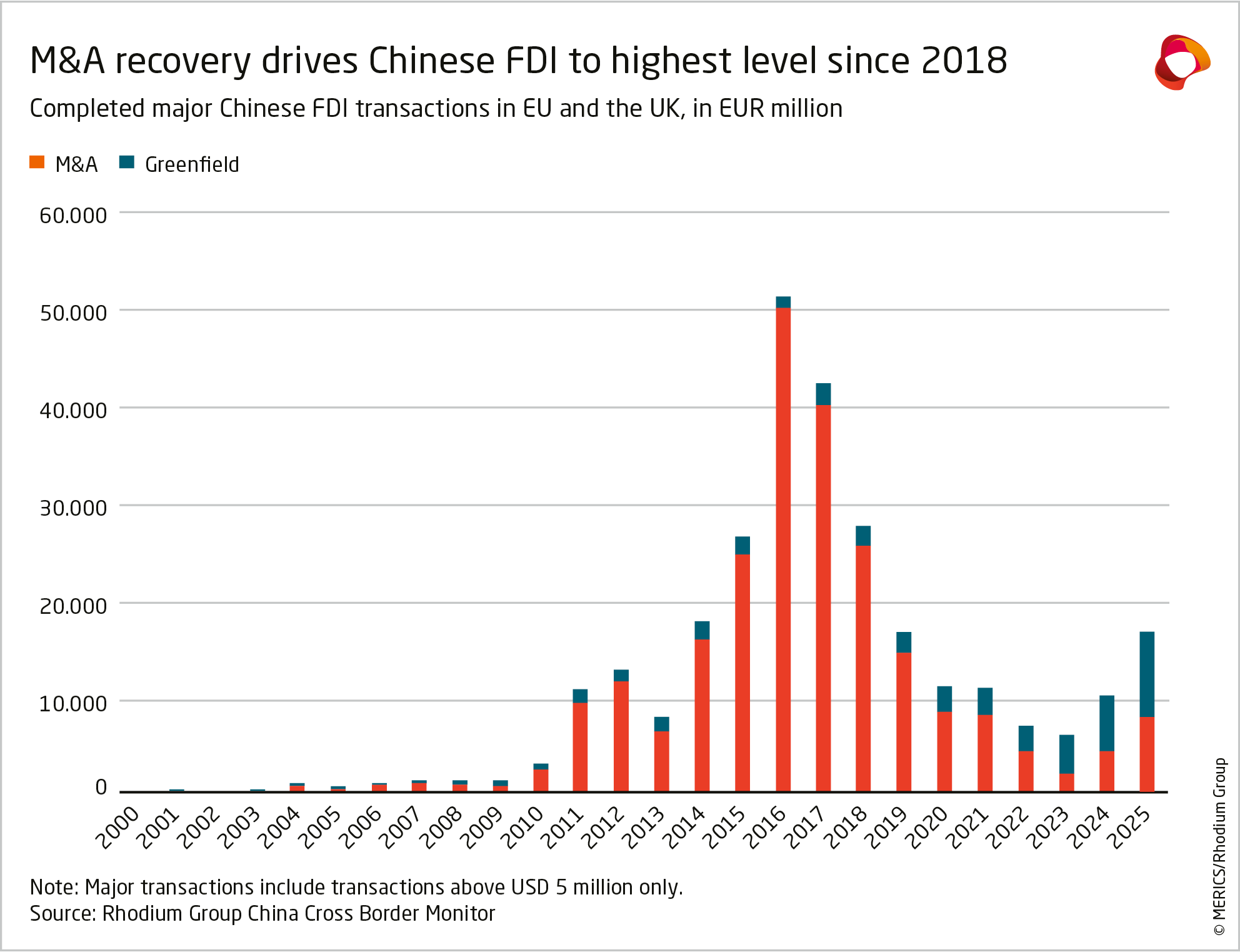

1.2 M&A recovery drives growth in Chinese FDI

Chinese outbound investment in the EU and the UK rose by 67 percent in 2025 to EUR 16.8 billion, up from EUR 10.1 billion in 2024. It is the second successive annual rise, following seven straight years of decline.

The revival was driven by much stronger M&A activity, which increased by 89 percent year-on-year to EUR 7.9 billion, marking a strong recovery from post-COVID lows. It put M&A almost back on parity (47 percent of total Chinese FDI in Europe) with greenfield investment. Some 44 percent of total M&A value was driven by three large transactions in consumer goods and gaming: Hongshan’s EUR 1.2 billion acquisition of consumer audio electronics manufacturer Marshall Group AB in Sweden; Tencent’s EUR 1.1 billion acquisition of video game studio Easybrain in Cyprus; and Tencent’s EUR 1.1 billion purchase of a 25 percent stake in Ubisoft’s Vantage Studios in France.

Greenfield investment also showed strong growth, reaching a new record of EUR 8.9 billion, a 51 percent increase compared to 2024. Growth was driven by construction starts for new CALB, CATL, and Gotion battery manufacturing facilities, expanding the pipeline of EV-related investments. Automative investments remained dominant, but their share declined from 85 percent in 2024, to 77 percent in 2025, due to modest diversification into such sectors as ICT and energy, including new investments by TikTok and the State Development and Investment Corporation (SDIC).

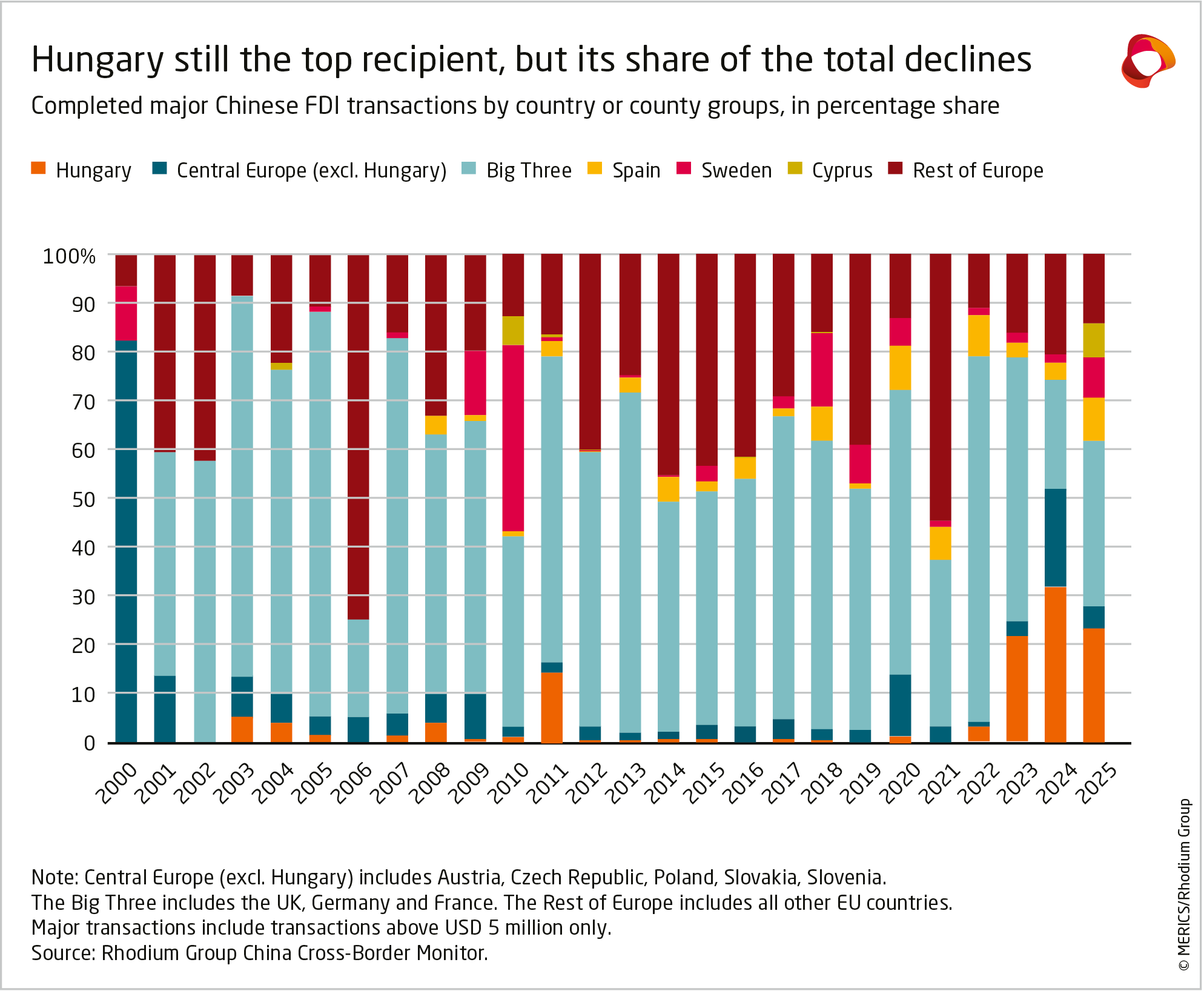

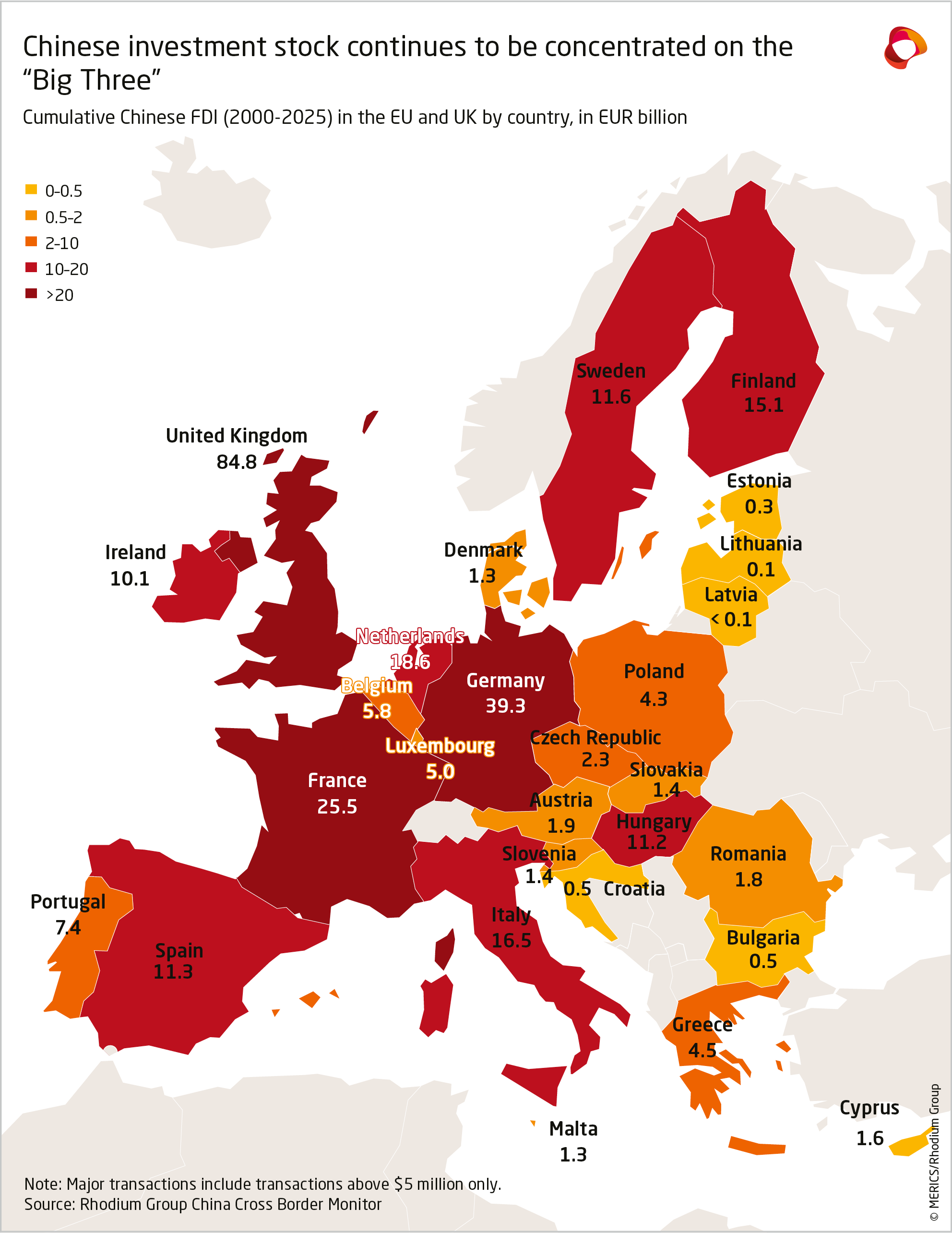

1.3 Hungary is still the top recipient, but its share has fallen

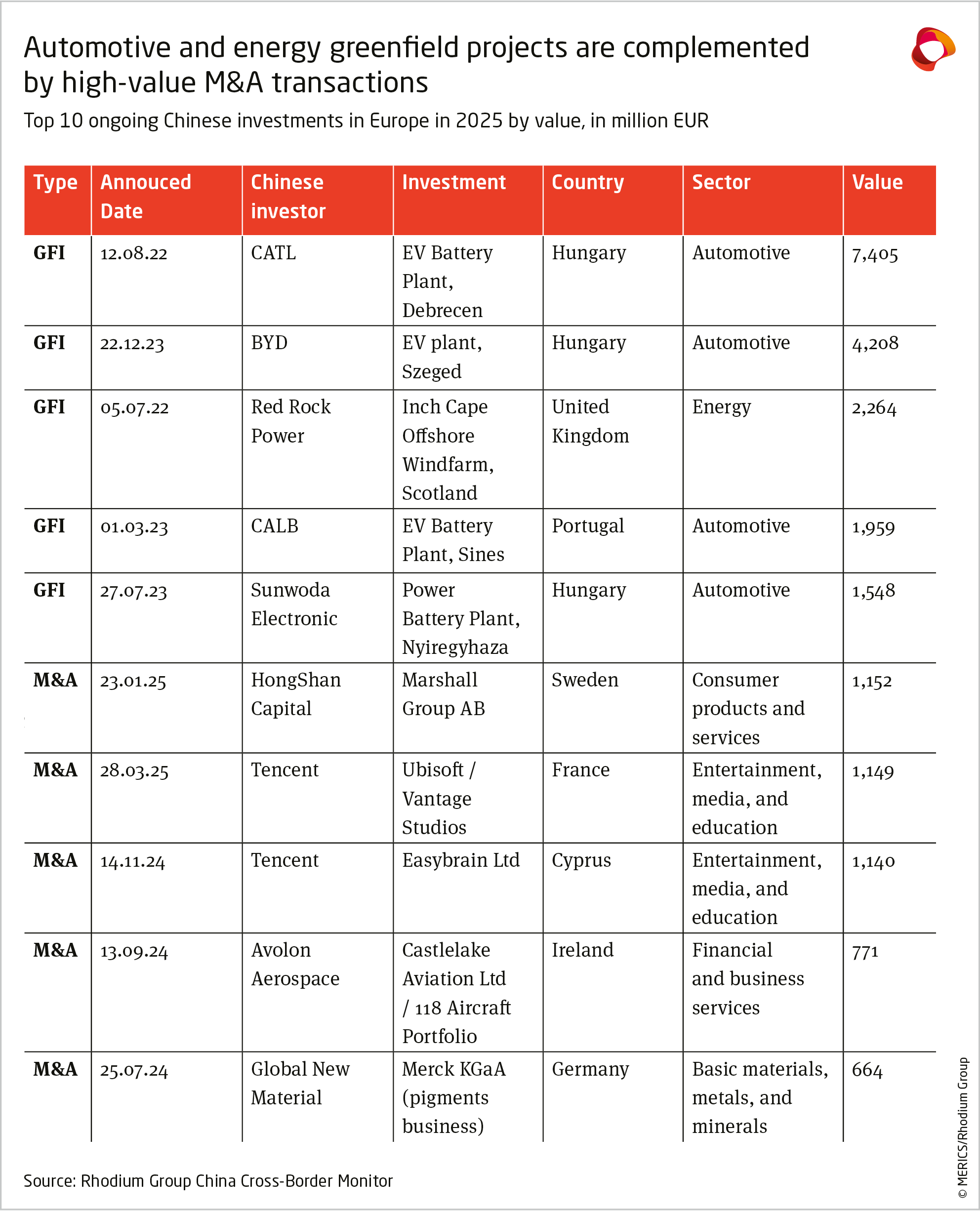

Investment in the EV supply chain meant Hungary retained its position as the top destination for Chinese FDI in 2025. Chinese FDI to the country rose from EUR 3.2 billion in 2024 to EUR 3.9 billion in 2025. Last year, three of the ten largest ongoing Chinese investment projects in Europe—CATL, BYD and Sunwoda Electronic—were in Hungary.

However, Hungary’s relative position weakened, as its share of total Chinese investment in Europe dropped from 32 percent in 2024 to 23 percent in 2025. No billion-euro investment announcements were made in 2025 – only smaller ones such as an R&D center for BYD (EUR 198 million) and Zhejiang Huashuo subsidiary Halms Hungary’s investment in an EV component factory (around EUR 200 million).

Germany and France ranked second and third. Germany raised its share of Chinese investment from 10 percent in 2024 to 15 percent in 2025. France boosted its share from 5 percent in 2024 to 12 percent in 2025. Completed investments almost tripled to EUR 2.5 billion in Germany, while they nearly quadrupled in France to EUR 1.9 billion. The “Big Three” economies (Germany, France and the UK) saw their combined share of Chinese investment grow from 23 percent in 2024 to 34 percent in 2025. Key projects in the Big Three included Red Rock’s offshore windfarm in Scotland, Luxshare’s acquisition of Leoni’s cable division in Germany and Tencent’s acquisition of 25 percent stake in Ubisoft’s Vantage Studios in France.

The rest of Europe attracted 43 percent of Chinese investment in 2025. Several countries received significant Chinese FDI, including Spain (EUR 1.5 billion, with more than a third coming from China Three Gorges’ acquisition of the Mula solar plant), Sweden (EUR 1.4 billion, dominated by HongShan’s purchase of the Marshall Group) and Cyprus (EUR 1.1 billion, all from Tencent’s takeover of Easybrain).

1.4 Automotive sector still the leader, while energy linked greenfield investment up sixfold

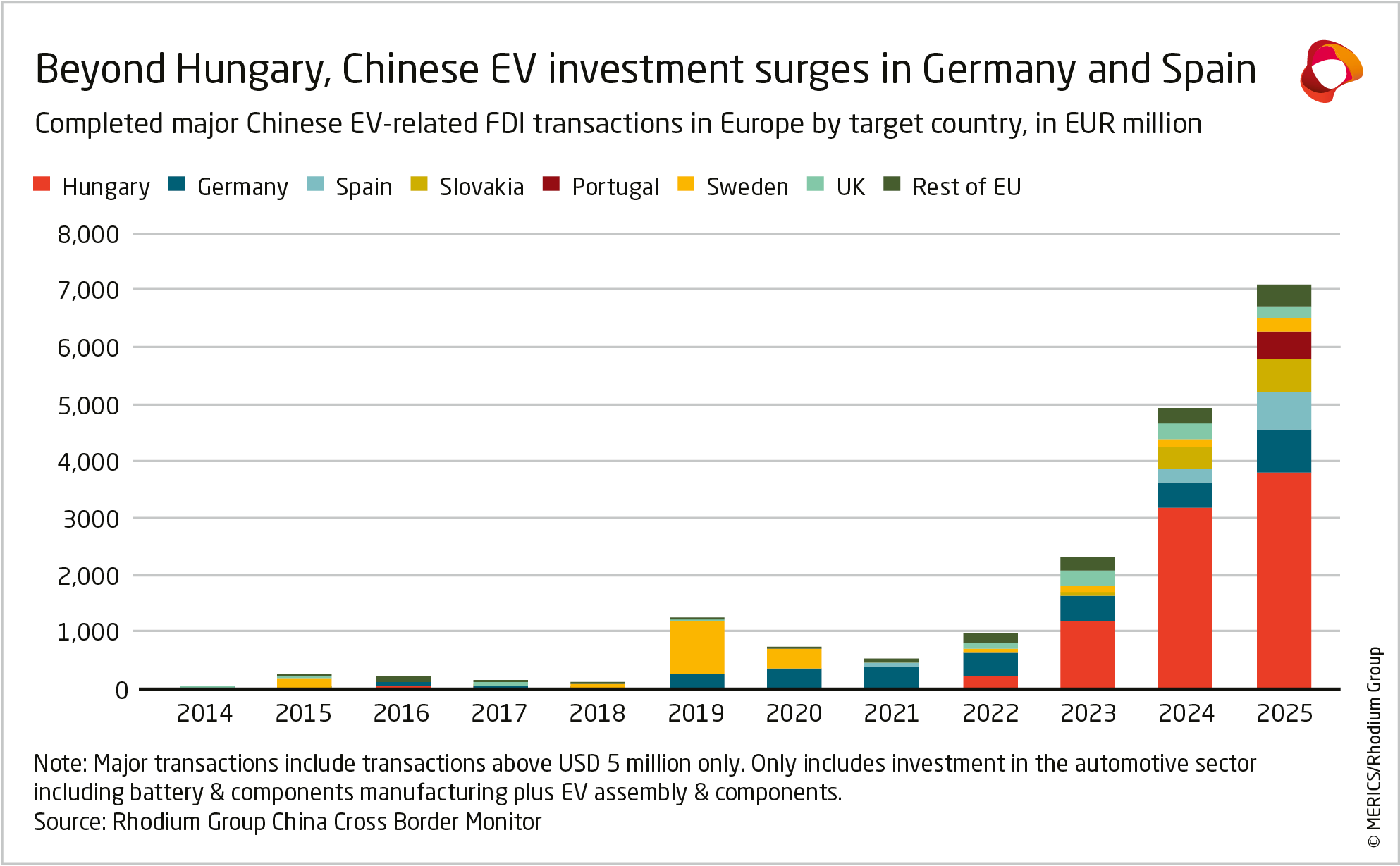

The three top sectors for Chinese FDI in Europe remained unchanged in 2025. The automotive sector received the largest share of Chinese FDI in Europe, pulling in EUR 7.6 billion in 2025, up 46 percent from EUR 5.2 billion in 2024. This made 2025 the second strongest year on record for Chinese automotive investment in Europe, after EUR 7.9 billion in 2015. The EV supply chain continued to dominate, making up 93 percent of Chinese automotive FDI in 2025 (vs. 94 percent in 2024). Among the largest new EV-related projects breaking ground were CALB’s EUR 2 billion battery factory in Portugal, CATL’s EUR 2.1 billion battery plant in Spain, and Gotion’s EUR 900 million battery plant in Slovakia. Thanks in part to these projects, battery investment exceeded EV manufacturing investment.

As in recent years, the bulk of Chinese EV investment in Europe went to Hungary, which attracted EUR 3.8 billion in 2025, up 18 percent from EUR 3.2 billion in 2024. But momentum shifted towards Germany, which saw investment rise 88 percent, and Spain, where it increased by 147 percent. Germany ranked second after Hungary for EV-related investment with EUR 783 million, while Spain ranked third, receiving EUR 642 million. Major projects included CATL’s new project in Spain, as well as Gotion’s ongoing project and new projects by Li Auto and Xiaomi in Germany.

The automotive sector’s importance declined slightly in relative terms, as its share of Chinese investment in Europe fell from 52 percent in 2024 to 45 percent in 2025.

Crucially, in 2025 there was another fall in the value of newly announced EV projects, which slipped to EUR 4 billion, down from EUR 5.3 billion in 2024, after plunging by two thirds from a record EUR 16.3 billion in 2023. Chinese EV investment in Europe is likely to remain stable for some years, as projects have multi-year construction periods and several broke ground in 2025. But it could decline sharply over a longer time horizon if fresh EV investment stays at these low levels (see section II).

Entertainment was the second most important sector in 2025, drawing in EUR 2.3 billion or 14 percent of Chinese FDI in Europe, an increase of 52 percent compared to the previous year. The consumer products and services sector ranked third with EUR 2 billion or 12 percent, up 93 percent on 2024.

Despite the high growth in these sectors, they are ill-suited to replace the automotive sector as a stable anchor for Chinese FDI in Europe. Both are dominated by M&A transactions, which tend to fluctuate on an annual basis. Investment in the entertainment sector in 2025 took the form of only two transactions, Tencent’s investment in Vantage Studios and its acquisition of Cyprus-based Easybrain.

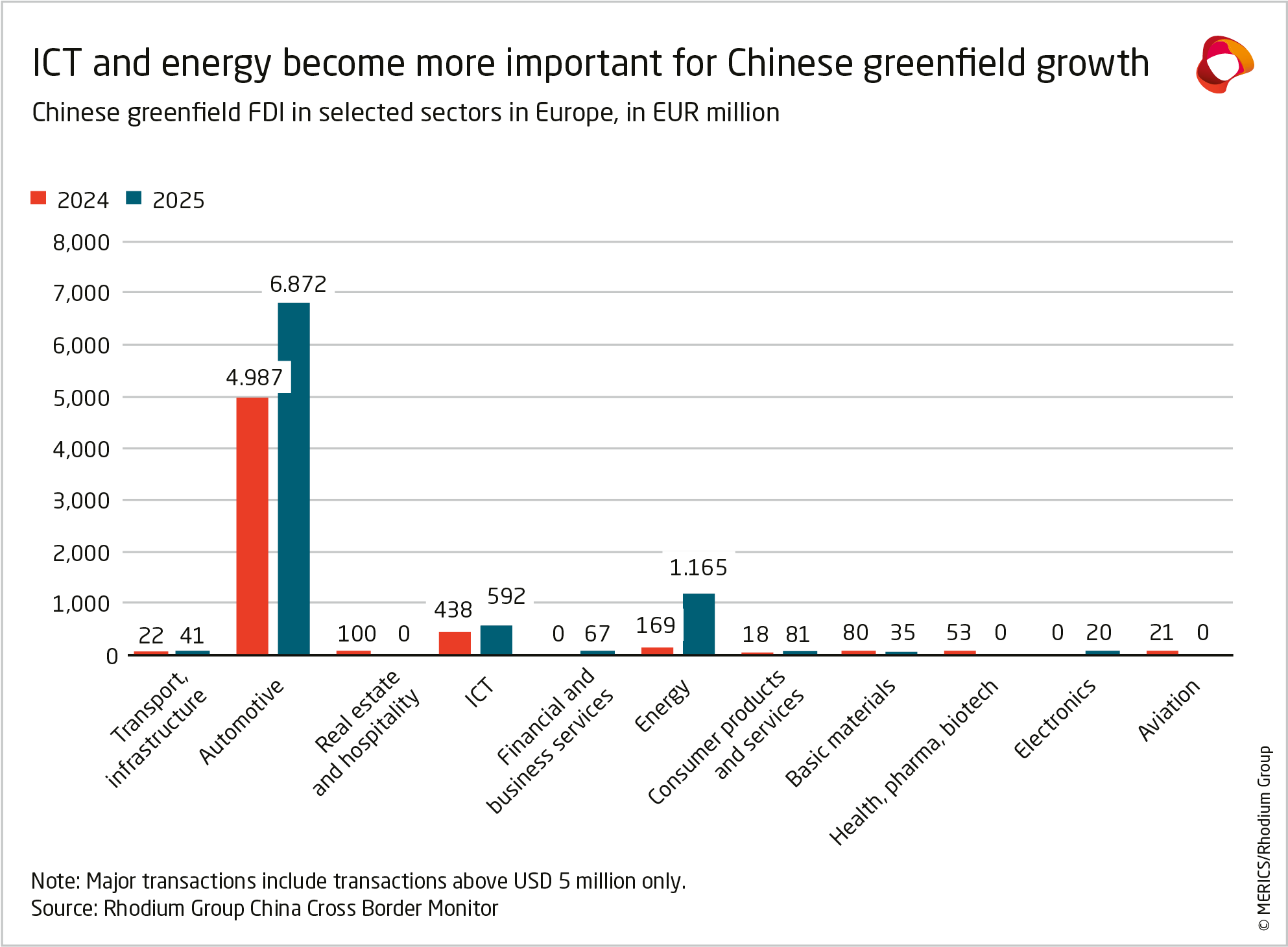

As in 2024, ICT and energy were the second and third largest sectors for Chinese greenfield investment. They displayed stronger momentum in 2025 than before. Greenfield investment in ICT grew by 35 percent to EUR 592 million, while in the energy sector it surged more than sixfold to EUR 1.2 billion. Red Rock’s Inch Cape offshore windfarm was paramount for the energy sector, contributing EUR 754 million. Other examples are Red Rock’s Benbrack onshore windfarm, also in Scotland, and DAS Solar’s solar module factory in France. In ICT, important projects included the construction of TikTok’s datacenter in Finland, Wingtech-owned Nexperia’s production plant in Hamburg, and Huawei’s completed but still empty phone manufacturing plant in France.

2. In focus: Investment momentum slows as Chinese firms favor exports

Chinese greenfield FDI in Europe has surged since 2023; it averaged EUR 6.3 billion annually in 2023–2025, up from EUR 2.8 billion in 2020–2022. However, momentum has stalled. Announced greenfield FDI fell from an average of EUR 18 billion in 2022–2023 to EUR 5.5 billion in 2024–2025. The slowdown worsened in 2025: over the last three quarters, newly announced projects averaged just EUR 440 million, compared to around EUR 3 billion per quarter since 2022.

As a result, the value of newly announced greenfield investments in 2025 fell back below announced M&A activity, reversing a three-year trend in which greenfield investment dominated. The deceleration is notable as continued headwinds in China’s domestic economy (weakening GDP growth, subdued consumption, thin corporate margins, and persistent deflationary pressures) would typically incentivize firms to expand into higher-margin overseas markets.

Momentum may be slowing because Chinese firms are favoring exports over foreign investment. Although newly announced greenfield investment is declining, Chinese exports to Europe continue to grow. Export values rose by 9 percent in 2025, with particularly strong growth in sectors which were previously the focus of Chinese FDI. Battery exports to Europe, for example, rose by 43 percent, while auto exports increased by 15 percent in value (and 29 percent in volume) and wind equipment exports surged by 65 percent. Medtech exports also recorded solid growth, rising 8 percent in value.

In key sectors, exports far outweigh planned local production. To date, only a handful of Chinese auto OEM projects in Europe have been confirmed: BYD in Hungary, Chery and Leapmotor in Spain and Geely-owned Volvo’s existing and planned European production. If Volvo is excluded, these investments remain modest in scale. Initial production from the three Chinese OEM plants is expected to be only around 215,000 units annually in 2026–2027, potentially ramping up to 500,000 units by the end of the decade. By comparison, China exported 922,000 vehicles to Europe in 2025, so exports, rather than local production, remain by far the dominant sales channel for Chinese OEMs in Europe.

2.1 Geopolitical uncertainty and macroeconomic conditions

There are several reasons why exporting to Europe remains more attractive to Chinese firms than investing on the continent. Geopolitical uncertainty is the first: 2025 was an exceptionally unpredictable year for foreign investors. The uncertainty around tariffs, trade negotiations, critical supply chains and major power tensions contributed to subdued investment. Many firms, including Chinese ones, adopted a wait-and-see approach. According to UNCTAD2, the value of global greenfield investment was flat, while the number of new project announcements fell by 16 percent.

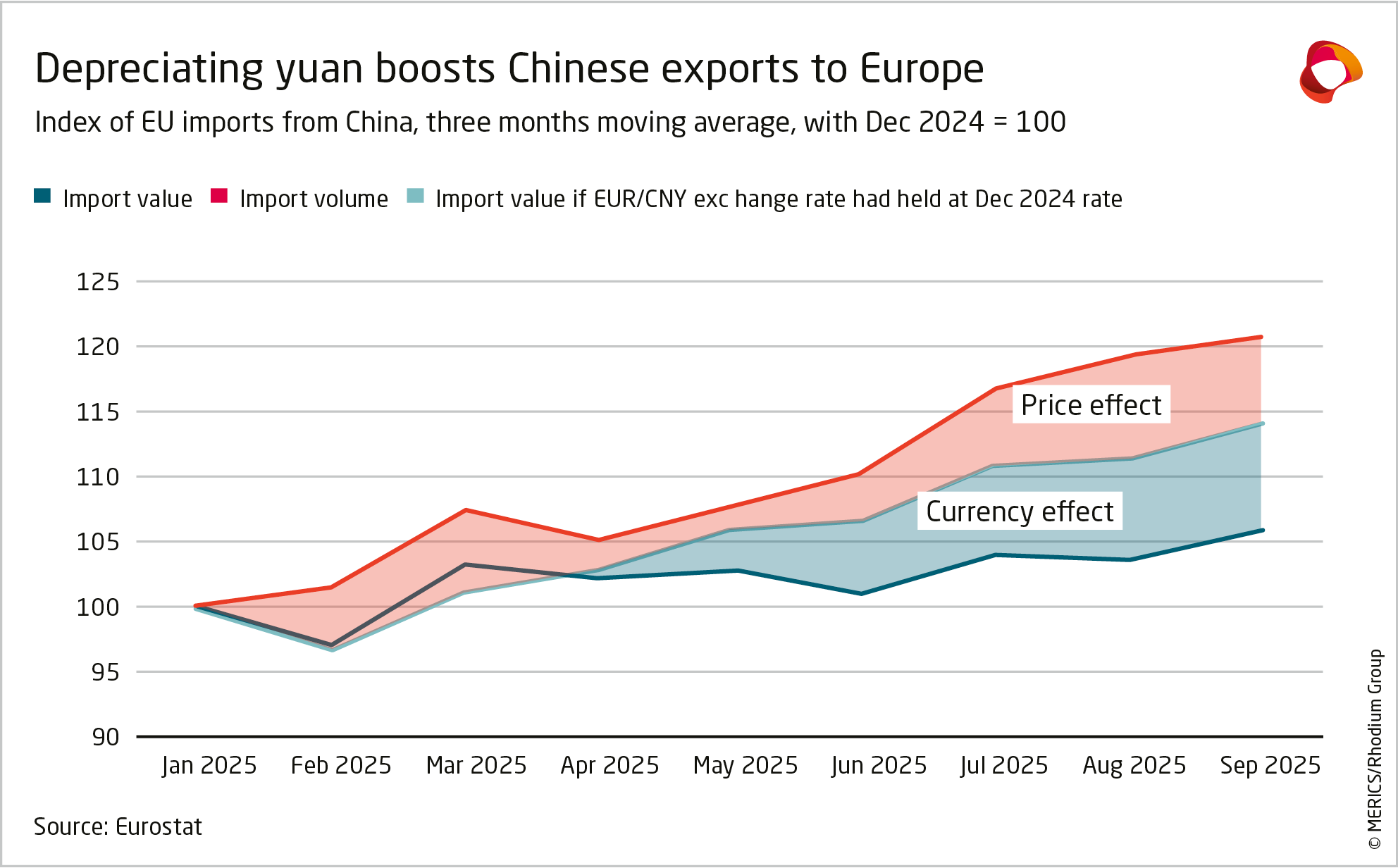

Second, macroeconomic conditions strongly favored exports over FDI. China’s currency weakened throughout the year and, according to an IMF report published in February 2026, was 16 percent3 undervalued. Against the euro, it dropped by 8.4 percent in 2025, with sharper declines at several points during the year. Combined with deflationary pressures in China, this significantly boosted export competitiveness (exhibit 9), offsetting4 some of Europe’s trade defenses. At the same time, a weaker currency raised the cost of overseas investment in RMB terms.

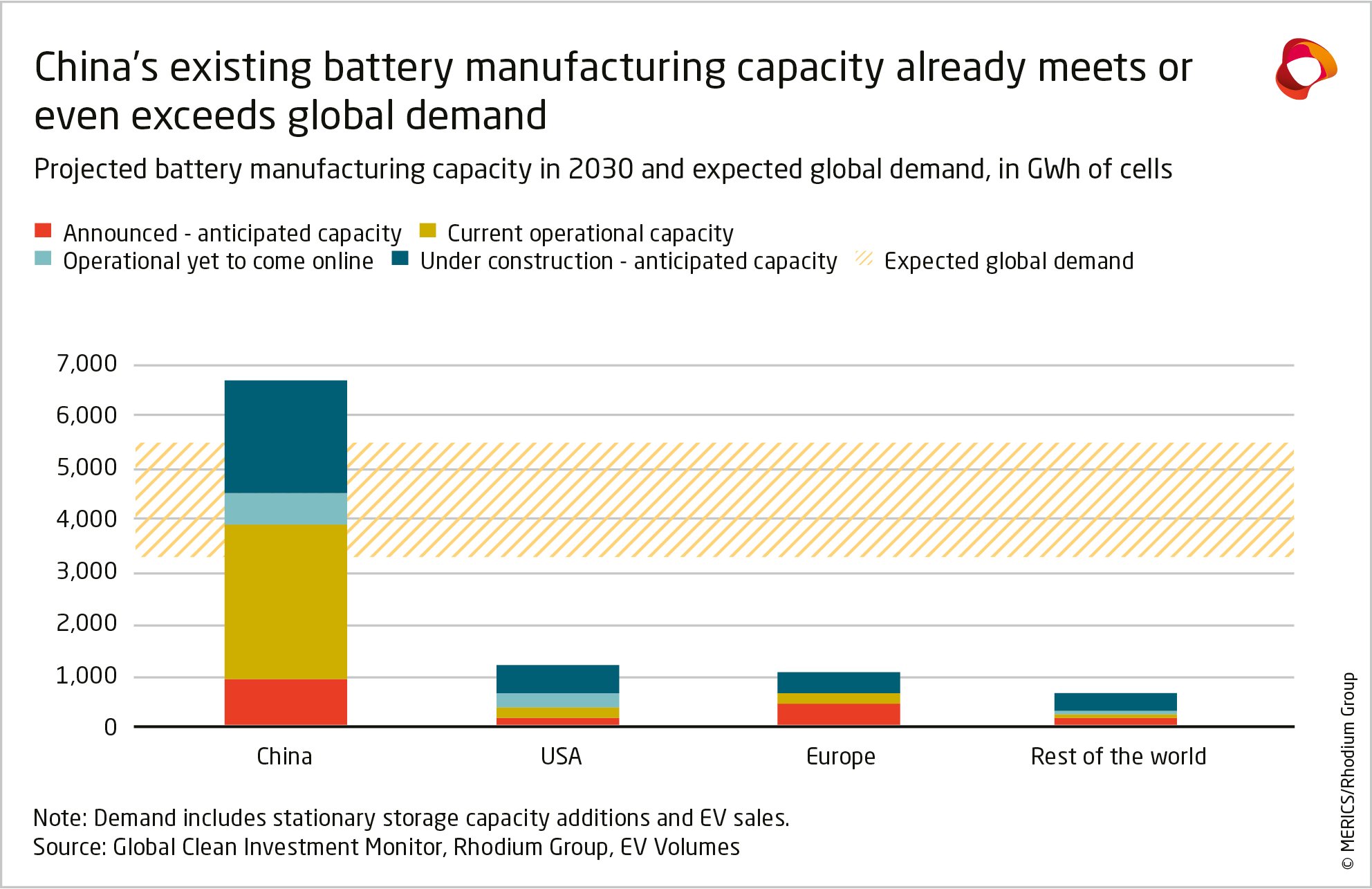

Beyond currency effects, Chinese firms possess ample domestic production capacity. In several sectors (batteries, EVs, solar), China-based output already meets or exceeds global demand, reducing the need for new overseas capacity (exhibit 10). Meanwhile, intense competition among many Chinese exporters weakens incentives for any single firm to commit to costly investments in Europe. The auto sector illustrates this dynamic. More than 21 Chinese OEMs are now present in the EU, but only nine have sold over 1,000 EVs/PHEVs in 2025 (up from five in 2024), and hence only a few (BYD, Chery, Geely, SAIC, and Xiaopeng) have reached the scale typically needed to justify local production. Among them, three have committed to plants, Xiaopeng has begun local assembly, and SAIC is the only “large” player yet to announce any investment.

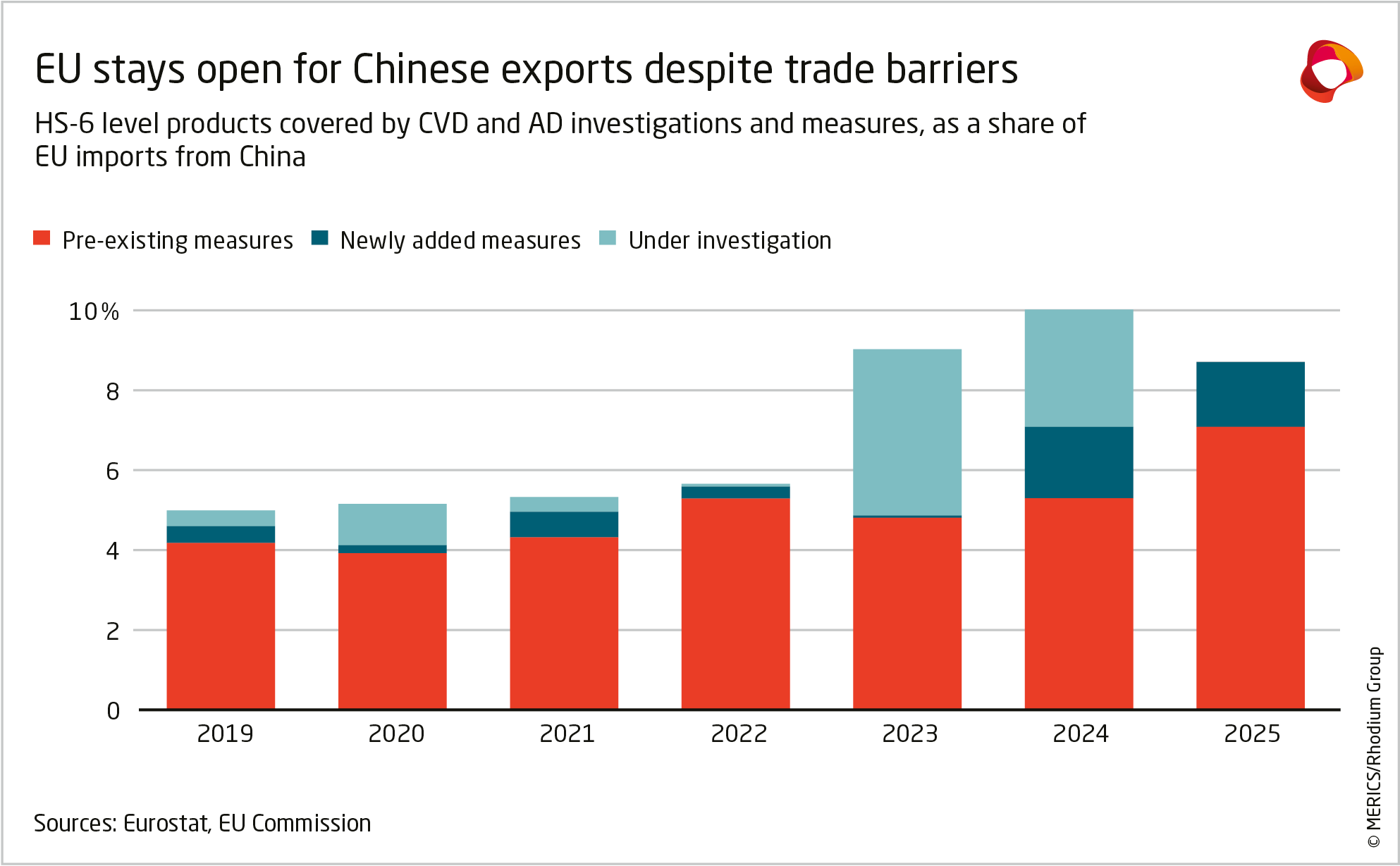

All this is in a context where Chinese firms still face relatively low trade barriers in Europe. By our calculations, EU anti-dumping and countervailing duties (AD/CVDs) only cover about nine percent of China’s exports to Europe, making the European single market a relatively open market for China-based exporters (exhibit 11).

2.2 Sluggish growth in key sectors and regulatory pushback against EVs

Third, sluggish growth in key sectors makes investment less appealing. While Chinese greenfield investment has been concentrated in EV and battery projects, there is growing pushback against green policies amid a rightward shift in the European Parliament and key member states. Last year, the European Commission acknowledged the trend by proposing to revisit the auto sector’s decarbonization pathway, allowing internal combustion engine vehicle sales beyond 2035 and greater flexibility towards interim targets. These steps suggest a slower EV rollout and weaker battery demand.

At the same time, US auto tariffs and regulatory pushback against EVs under the Trump administration are dampening demand for European-produced EVs, which limits export opportunities. These combined developments have prompted a more cautious approach by OEMs which probably contributed to the decline in EV and battery investment announcements in 2024–2025.

2.3 Europe's scrutiny of Chinese investments

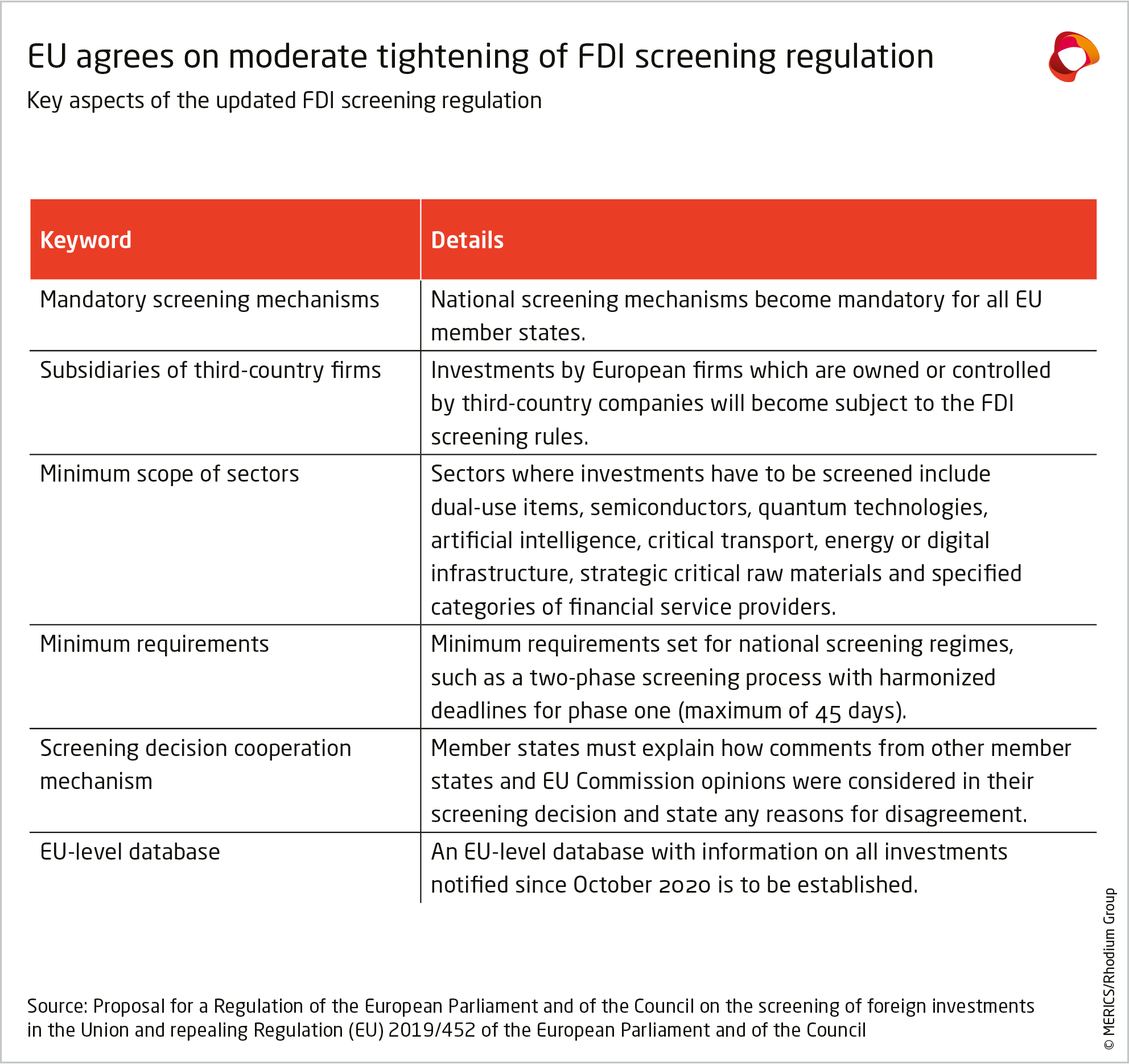

Fourth, Europe is tightening the regulatory framework for Chinese investment, which creates additional uncertainty and raises the risk that projects are delayed or abandoned. The updated EU FDI screening regulation agreed on by the European Commission, Parliament and Council in December 2025, introduces several important changes, as shown in exhibit 13. However, more assertive ideas, such as giving the Commission the power to override member states’ screening decisions, were not taken up due to opposition from the Council.

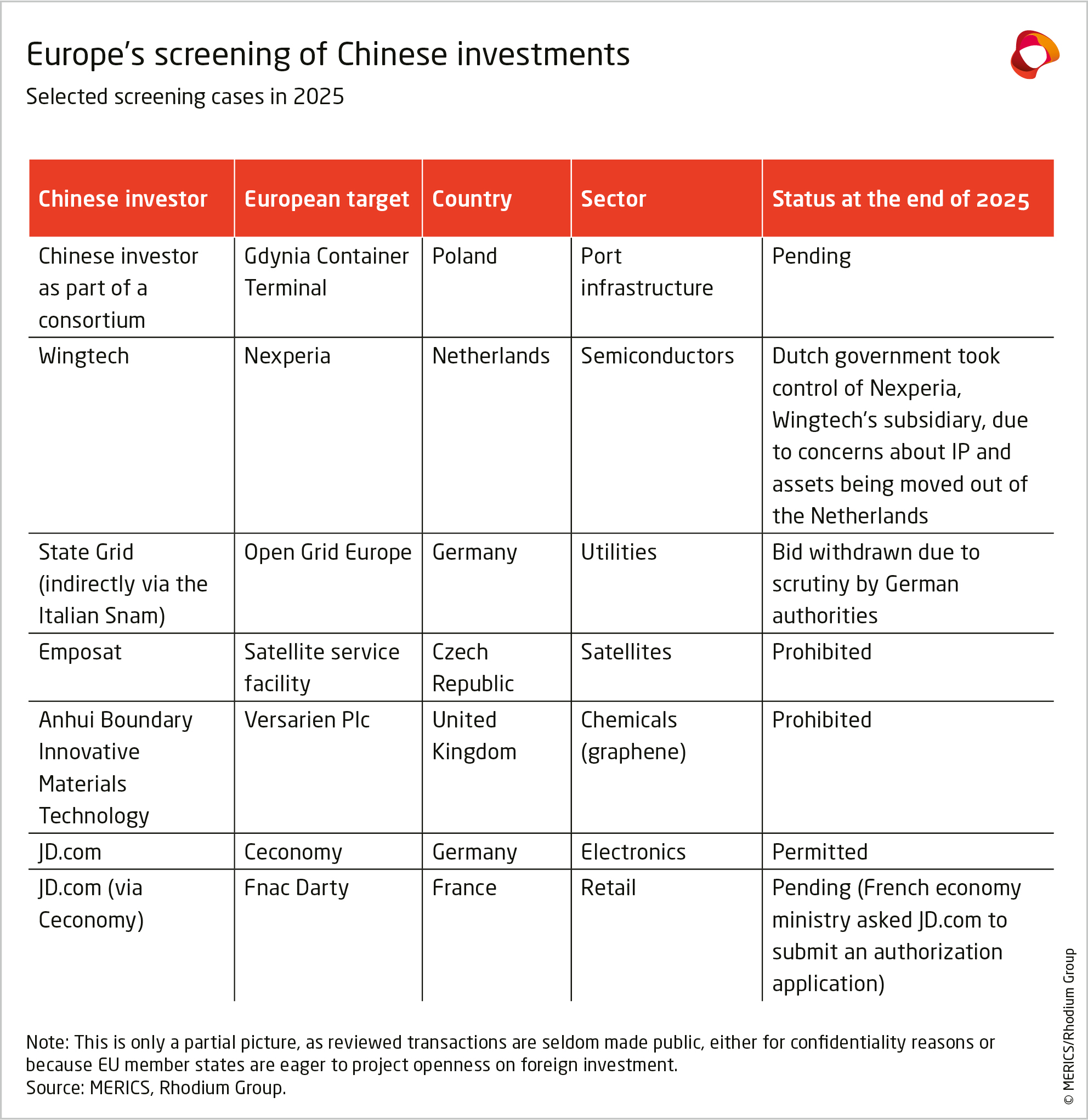

Aside from these regulatory changes, Chinese investments in the EU continued to be reviewed under the current regulation, including 33 in Germany5 alone. While few of these reviews were made public, evidence is available on a few select cases (see exhibit 14). There were national debates on several high-profile Chinese investment projects. For instance, CATL’s plan to build its new EV battery factory6 in Spain using only Chinese workers has sparked skepticism about local benefits and knowledge sharing. In France, the economics ministry vowed to ensure that retailer Fnac Darty’s household appliances continue to be manufactured locally as it became wary of the stake JD.com7 would acquire in Fnac Darty via its takeover of Ceconomy. Meanwhile, rumors about Chinese EV manufacturers taking over underutilized Volkswagen factories8 in Germany triggered concern from the unions about possible job losses.

Chinese firms may also be concerned about the risk of state intervention. In October 2025, a Dutch court placed chipmaker Nexperia under custodial management amid allegations of misconduct by its Chinese owner. While such actions may be justified from a European perspective, they could make Chinese investors think twice.

Chinese firms are also waiting to see if the European Commission will launch new cases under the Foreign Subsidies Regulation (FSR), following a December 2025 communication9 in which the EU executive promised to use such tools more proactively. The FSR allows the Commission to investigate companies if it suspects them of benefiting from foreign subsidies that distort the European market. The tool can apply to investments. In March 2025, for example, the Financial Times reported10 that the Commission was considering an FSR probe into BYD’s plant in Hungary. There has been no news about the probe since then, but even the suggestion of such an investigation could discourage Chinese firms that have benefited from state support from investing. Beijing has already signaled its concern11, indicating it is closely monitoring the EU’s use of the FSR and could retaliate if Brussels takes action against Chinese firms in sectors such as wind or security equipment.

In 2025, there were also intense debates in Europe about “conditioning” investment and imposing “made in Europe” requirements in public procurement and public incentive schemes, with Chinese investment in mind. The goal of “conditioning” would be to ensure incoming investment delivers tangible benefits to the EU such as local jobs, value creation, and technology transfers.

Local content rules are designed to protect Europe-based supply chains and, in theory, incentivize higher value investment. An update of the EU’s Cybersecurity Act could also limit Chinese firms’ market access in key connected technologies within the next couple of years. Measures such as these may have the unintended consequence of reducing the EU’s overall attractiveness to Chinese firms as an investment destination. They may choose to delay investment decisions until there is more clarity on the key elements of these proposals, which must still be approved by the European Parliament and member states.

The EU’s Industrial Accelerator Act (IAA) promotes localization: The twin ideas of “conditioning” FDI and “made in Europe” requirements were formalized in the EU’s Industrial Accelerator Act (IAA) proposal released in early 2026. The text proposes putting new conditions on investments in key sectors if the investing firm’s home country account for more than 40 percent of global production. In practice, this threshold would largely apply to Chinese firms in clean tech sectors. Linked requirements would make it more burdensome for Chinese firms to invest in Europe by raising production costs through forced substitution of Chinese inputs with European ones, increasing IP leakage risks, and adding costs for workforce localization and training. The IAA’s “Made in Europe” requirements for public procurement would create a strong de facto market access barrier to Chinese exports. This could incentivize pro duction localization in some circumstance. But it could also prompt Chinese firms to give up on parts of the European market (e.g. the corporate auto fleets), as market access becomes too burdensome. The rules could also threaten the viability of existing projects such as BYD’s Hungary plant and raise the bar for future investments. Simply put, without full localization of most of the upstream supply chain, Chinese manufacturing plants might not be eligible to count as “Made in Europe.” The effectiveness of both proposals will depend on three main factors: 1) the strength of associated market access barriers limiting exports—which would be the more at tractive entry route if investment conditions tighten; 2) the openness of key partner countries that meet the “Made in Europe” definition and so could attract Chinese investment instead of member states; 3) China’s response, particularly its potential use of leverage over essential inputs such as critical raw materials to dilute or counter these measures.

3. Outlook

In 2026, Chinese firms will continue to pursue opportunities in global markets against a backdrop of weak domestic demand and low profit margins at home. There are few signs that the Chinese leadership’s promises to boost consumption-led growth, heard at the Central Economic Work Conference in December 2025 and the March 2026 Two Sessions, will translate into the structural reforms needed to generate a durable recovery in domestic demand. Chinese growth, therefore, will remain heavily reliant on overseas markets.

The key question is whether Chinese firms will continue to rely heavily on exports for their overseas sales, or whether we will see a steady increase in levels of outbound investment. If economic, political and policy conditions – including the imposition of trade barriers – do not change substantially, we expect Chinese firms to favor exports.

On the macroeconomic front, China’s currency remains undervalued and we expect China to stick to its policy course in 2026. As in 2025, a weak RMB will boost Chinese export competitiveness, making the EU’s trade defenses less effective and investing in Europe more expensive. Meanwhile, while Chinese producer and consumer prices could rise this year on the back of the war in Iran and input shortages (e.g. memory chips), we expect the persistent mismatch between demand and supply to persist, incentivizing Chinese firms to use their China-based capacity to serve global markets.

On the policy front, we expect Beijing to continue prioritizing domestic industrial capacity over overseas expansion, where possible, thereby keeping core technologies and know-how at home.

In Europe, meanwhile, high production costs and regulatory barriers will make it challenging for member states to attract Chinese greenfield investment. Policy efforts to forcibly bring more production onshore, including through the IAA, will take 18-24 months to be in place—and the proposals might be diluted in the EU’s trilogue process between the Commission, Parliament and European Council. Until then, EU trade action could remain muted due to the risk of Chinese retaliation, notably through controls on critical raw materials, and erratic US tariff policies. This will leave European markets broadly open to Chinese exports in the medium-term. Combined with the risks attached to EU’s FDI conditioning policies and potential use of the FSR, Chinese firms may feel there are fewer reasons to invest in the EU.

A few things could offset these trends. For one, greenfield projects launched in past years will continue to put a floor under Chinese FDI levels in the years ahead. The uptick in Chinese acquisitions in late 2025 could persist in 2026 and contribute positively to the Chinese FDI topline. Exporters who have gained market share may want to cement their position through investments. Chinese firms may position themselves for the European preference rules laid out in the IAA by setting up or acquiring production facilities. It seems likely that Chinese companies will continue to channel investments towards those member states that are seen to be more closely aligned with China, such as Hungary, Spain and Slovakia.

- Endnotes

1 | According to Rhodium Group’s China Cross-Border Monitor.

2 | United Nations Trade and Development (UNCTAD). “Global foreign investment up 14% in 2025, with growth concentrated in developed economies” https://unctad.org/news/global-foreign-investment-14-2025-growth-concentrated-developed-economies. Accessed: April 22, 2026.

3 | Mayger, James and Do Rosario, Jorgelina. Bloomberg (2026). “IMF Warns China’s Economic Policies Are Causing Damage to Others” February, 18. China’s Economic Policies Are Causing Damage to Others, IMF Warns - Bloomberg. Accessed: April 22, 2026.

4 | Boullenois, Camille and Williams, Gregor and Wright, Logan. Rhodium Group (2025). “Malign Indifference: China’s Currency and the Threat to Europe” December, 18. https://rhg.com/research/malign-indifference-chinas-currency-and-the-threat-to-europe/. Accessed: April 22, 2026.

5 | Bundeswirtschaftsministerium (BMWE). „Investment Screening in Germany: Facts & Figures“ https://www.bundeswirtschaftsministerium.de/Redaktion/EN/Publikationen/Aussenwirtschaft/investment-screening-in-germany-facts-figures.pdf?__blob=publicationFile&v=1. Accessed: April 22, 2026.

6 | Foster, Peter and Borrett, Amy and Dunai, Marton and Minder, Raphael. Financial Times (2025). “China’s investment push in Europe hits a wall” October, 20. https://www.ft.com/content/093de2c1-162a-44c4-b954-15db3c856047. Accessed: April 22, 2026.

7 | Prudhomme, Cécile and Boutelet, Cécile. Le Monde (2025). “Amid Shein controversy, Chinese e-commerce giant JD.com sets sights on European market” November, 13. https://archive.is/kR6cn#selec-tion-2049.387-2109.322. Accessed: April 22, 2026.

8 | Business Insider (2025). “Chinesische Autohersteller wollen angeblich diese VW-Werke in Deutschland kaufen“ January, 27. https://www.businessinsider.de/wirtschaft/mobility/vw-chinas-autohersteller-wollen-angeblich-deutsche-werke-kaufen/. Accessed: April 22, 2026.

9 | Council of the European Union. “Strengthening EU economic security” https://data.consilium.europa.eu/doc/document/ST-16389-2025-INIT/en/pdf. Accessed: April 22, 2026.

10 | Bounds, Andy and Foy, Henry and Dunai, Marton. Financial Times (2025). “EU probes BYD plant in Hungary over unfair Chinese subsidies” March, 20. EU probes BYD plant in Hungary over unfair Chinese subsidies. Accessed: April 22, 2026.

11 | Laprévote, François-Charles et al. Concurrences (2025). “The Chinese Ministry of Commerce issues a final determination on a trade and investment barrier investigation into the EU’s FSR” January, 9.

The Chinese Ministry of Commerce issues a final determination on a trade and investment barrier investigation into the EU’s FSR - Concurrences. Accessed: April 22, 2026.

Building on a long-standing collaboration between Rhodium Group and MERICS,

this report summarizes China’s investment footprint in the EU-27 and the UK in

2025, analyzing the shifting patterns in China’s FDI, as well as policy developments

in Europe and China.

![]()

Author(s)

Director, Rhodium Group

Analyst

Senior Analyst, Rhodium Group and former Analyst, MERICS

Research Analyst, Rhodium Group

Author(s)

Director, Rhodium Group

Analyst

Senior Analyst, Rhodium Group and former Analyst, MERICS

Research Analyst, Rhodium Group