picture alliance / Li Hao | Costfoto

Content

Report

In the driver's seat: China's electric vehicle makers target Europe

Key developments and challenges to European governments and companies

Main findings and recommendations

- China will become a major automotive export hub. Fueled by technological change, huge production capacity and government support China has the necessary requirements to export vehicles on a large scale.

- Europe is the main market for Chinese electric vehicle (EV) exporters. Europe has the second highest demand for EVs after China. Buyers benefit from high subsidies and a comparatively well-developed charging network. China’s automakers have government support to master European safety ratings.

- China’s government directs and pressures Chinese and China-based foreign carmakers to export. The government has relegated its ambition to primarily promote national champions in favor of absorbing global value chains. The government is also setting targets and providing information about overseas regulations to help Chinese EV makers overseas advance.

- Chinese manufacturers are moving up the value chain. Chinese car makers have leapfrogged established carmakers and can now produce desirable, safe and technologically advanced EVs. A few Chinese brands have a shot to rank among the world’s most successful carmakers.

- Chinese companies’ overseas investments and partnerships make them global competitors. Automotive competition is going to increase globally, and consequently Chinese battery manufacturers and carmakers are expanding their global footprint. Exports are only the tip of the iceberg as companies pursue different strategies to leverage international brands and access overseas markets.

- Government subsidies for China-based manufacturers could distort global markets. That China has become the leading EV market is the result of substantial government support. But Chinese exports are also directly supported by central and local governments sponsorship of new production plants, R&D centers and overseas acquisitions.

1. Electric vehicles offer a window of opportunity for China's auto exports

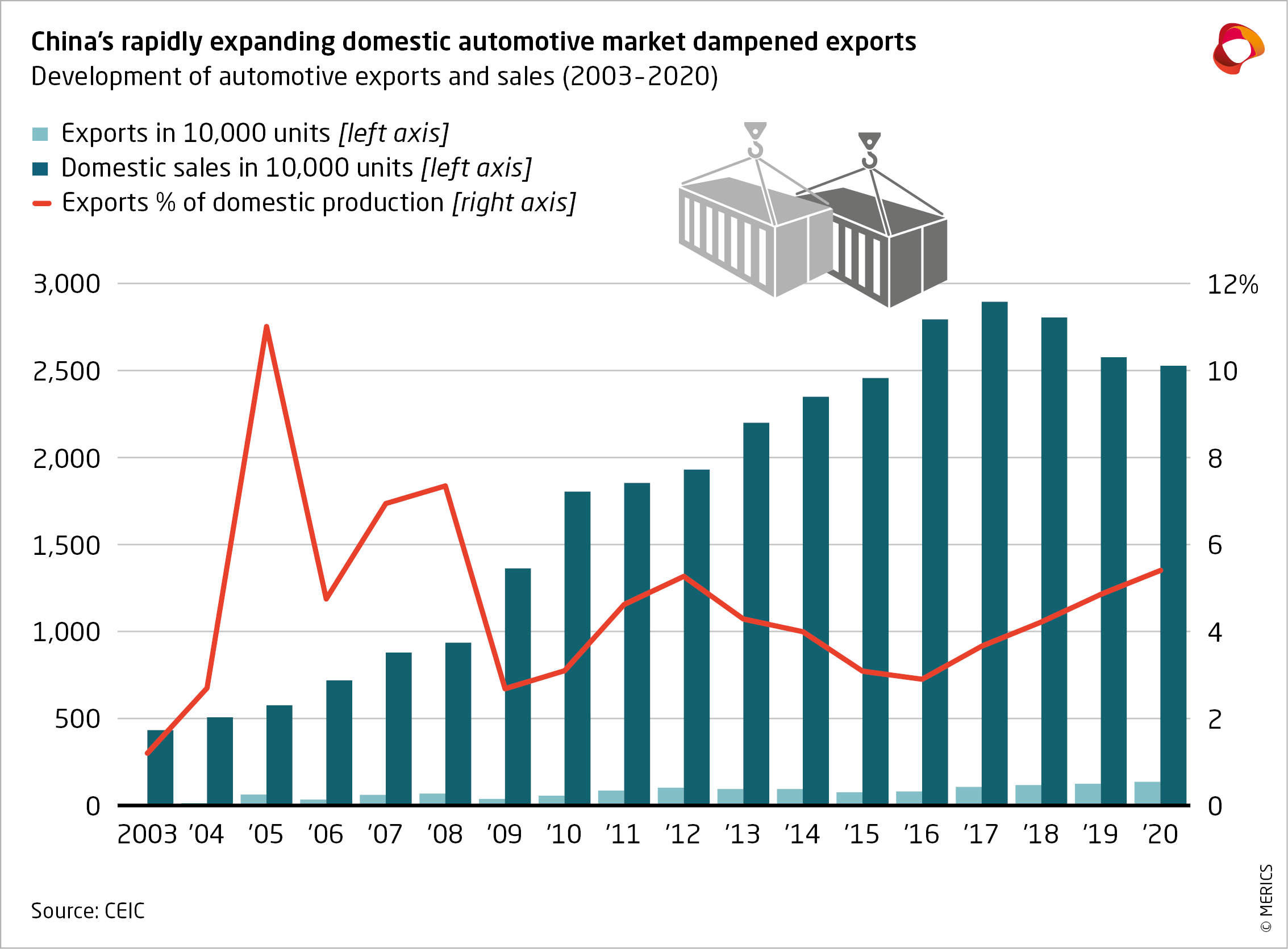

China overtook the US to become the biggest automotive market and producer in 2009. One third of all vehicles are now produced in China.1 However, this success story has not yet translated into automotive exports (see exhibit 1). That is about to change as Chinese manufacturers have set their eyes on global markets; it is a strategy in which European markets and actors play a key role.

Until recently, China-based carmakers had little economic incentive to push into overseas markets as surging domestic sales buoyed them up, tripling in eight years between 2008 and 2016 (see exhibit 2). Some Chinese SOEs started exporting on a bigger scale in the mid- 2000s, largely in response to government pressure to signal that Chinese cars were globally competitive. Unfortunately, the export push by SOEs such as Brilliance and JMC had the opposite effect. JMC’s Landwind received record-low safety ratings from Euro NCAP, a testing organization, which has stained the reputation of Chinese cars.

Next came an export push from foreign carmakers manufacturing in China (from 2015 to 2019) that saw GM export China-made Buicks to the United States. It fizzled quickly when the Trump administration placed tariffs on China-made cars. Overall, Chinese automotive exports have remained small, in both relative and absolute terms. With the notable exception of the United States, most Chinese auto exports are to emerging markets.

However, the pattern could be about to change. A mixture of technological advances and structural changes in the global automotive industry has created a window of opportunity for global expansion by China-based carmakers. Several major disruptive technology- driven trends, including electrification and autonomous driving, have the potential to fundamentally alter driving and automotive manufacturing. The automotive industry remains in flux, and established hierarchies are being called into question. Chinese policymakers recognize that it is an opportune time to jumpstart exports once more.

China’s new export push is likely to focus on EVs2 and several factors indicate it may be more successful than before:

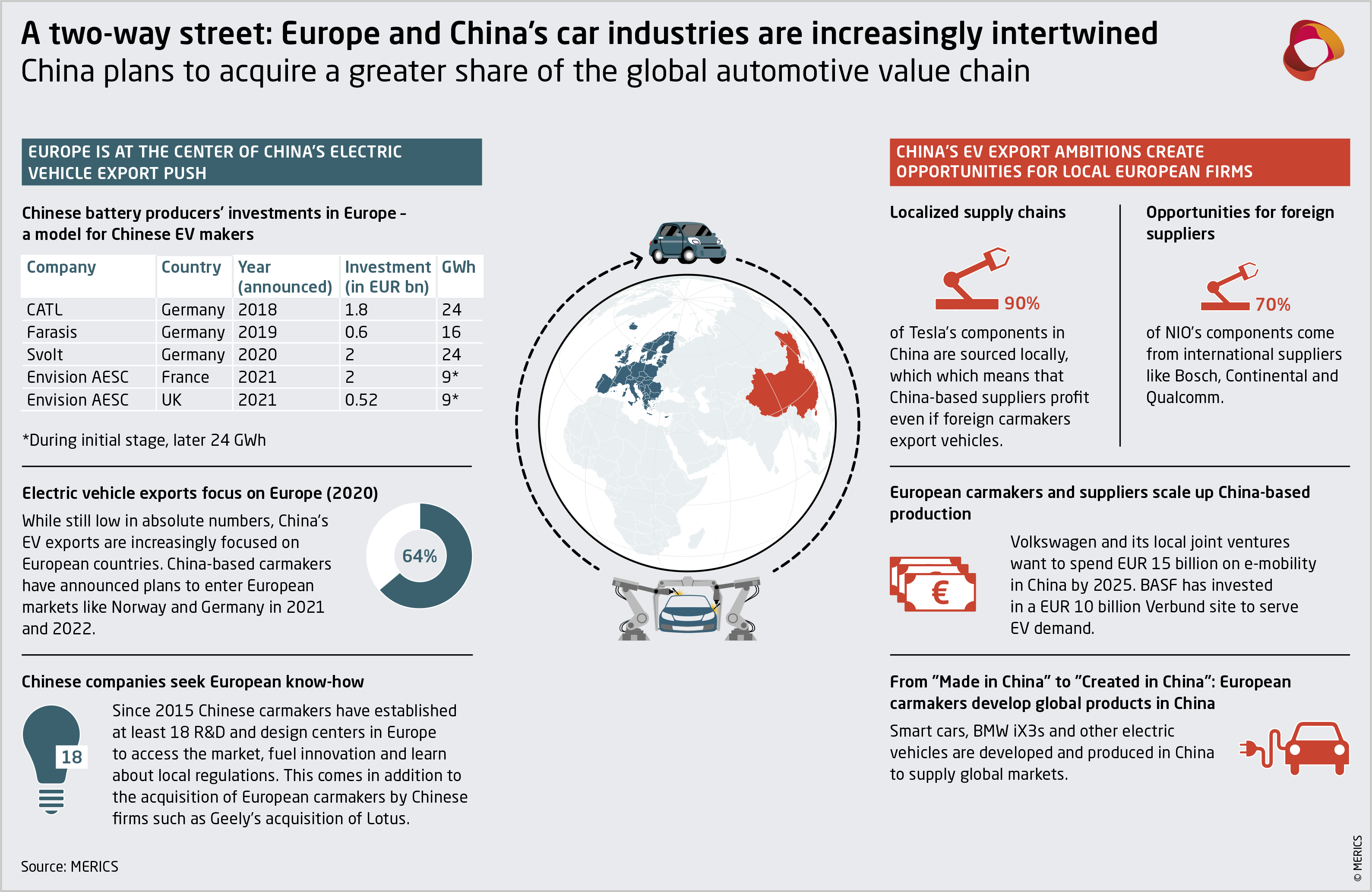

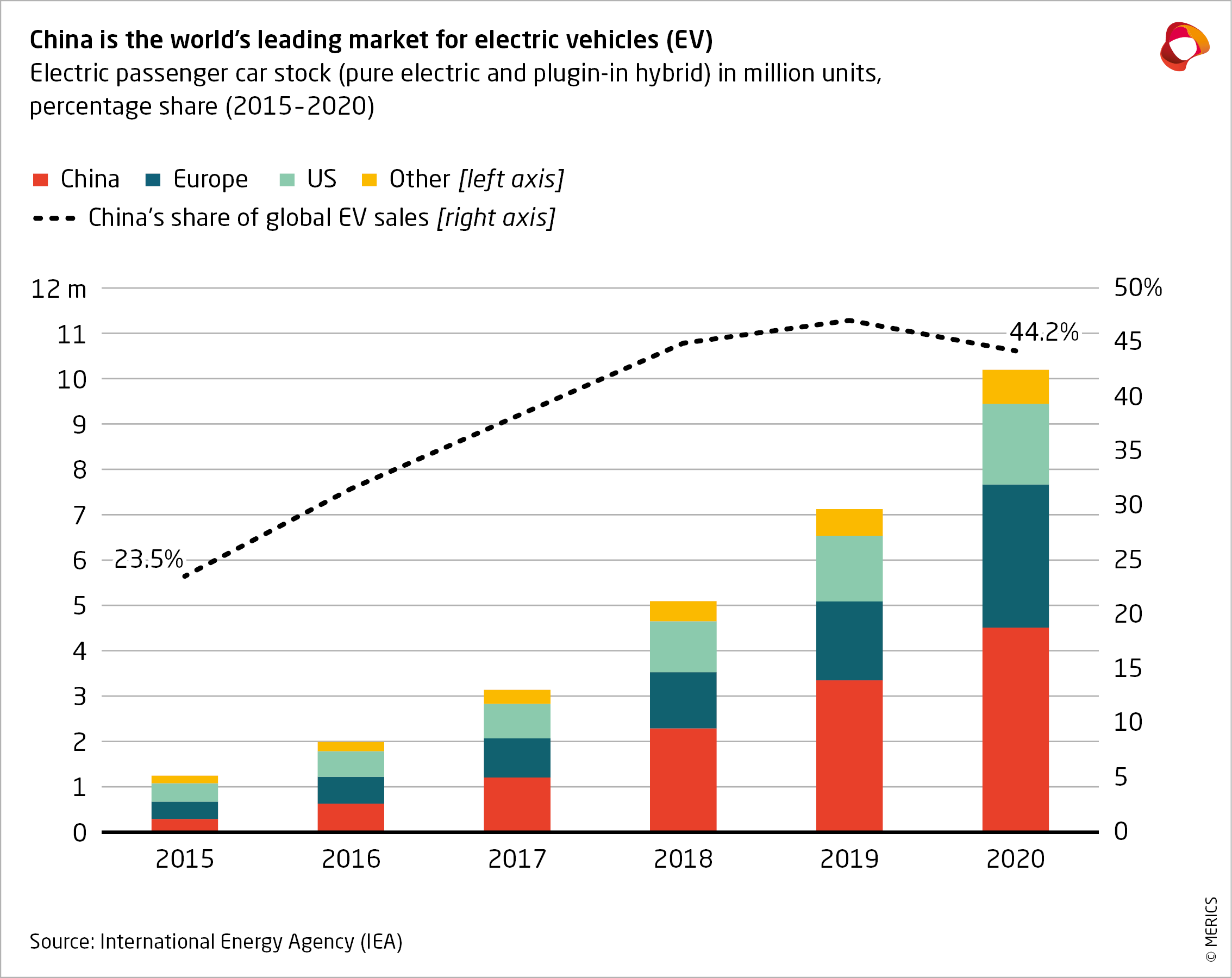

- China is the leading EV market: Aided by substantial state support, China has become the biggest EV market (see exhibit 3). Chinese EV makers have leapfrogged entrenched carmakers to become frontrunners with internationally competitive products, including in luxury segments. Internationally successful Chinese battery makers like CATL serve as a role model for Chinese EV makers.

- Slowing domestic growth: China’s economic growth has stalled in recent years, which has slackened the dramatic growth rates in its domestic automotive market too. Between 2009-2016, China’s carmakers had little incentive to export as domestic growth offered ample returns. However, as demand for EVs is increasing rapidly in other economies, China-based carmakers have an economic incentive to expand globally.

- Domestic overcapacity: China’s automotive and EV sectors already suffer from serious overcapacity, yet newcomers continue to enter the field, including tech companies like Baidu and conglomerates like Evergrande. The result is fragmentation and increasing overcapacity. In 2020, 89 Chinese EV-producers averaged sales of only 15,000 units3, while China’s vehicle capacity utilization rate has been falling – to 48.5 percent in 2020 – which puts pressure on EV makers to export to achieve economies of scale.

- National champion status: Chinese carmakers are eager to export to become the next national champion. In the rail sector, where China also wants to compete globally, the government has forced major SOEs to merge to give CRRC a competitive edge due to sheer size. A similar consolidation will occur in the EV sector once government subsidies end, so successful exports could give Chinese EV makers a chance to stand out.

- Strong presence of foreign MNCs: Foreign multinational carmakers are starting to use China as an export hub. They are attracted by China’s leading and dynamic EV market, local technologies and innovation capabilities and proximity to battery suppliers. China’s government actively supports them in their export plans.

China’s bet on electric vehicles and the involvement of foreign carmakers appears to be starting to pay off. The latest data shows that monthly exports have steadily increased since September 2020, with a record of 150,100 units exported in April 2021 (see exhibit 4). In April, EVs accounted for 16 percent of China’s passenger car exports, of which 14,000 were Tesla models.4

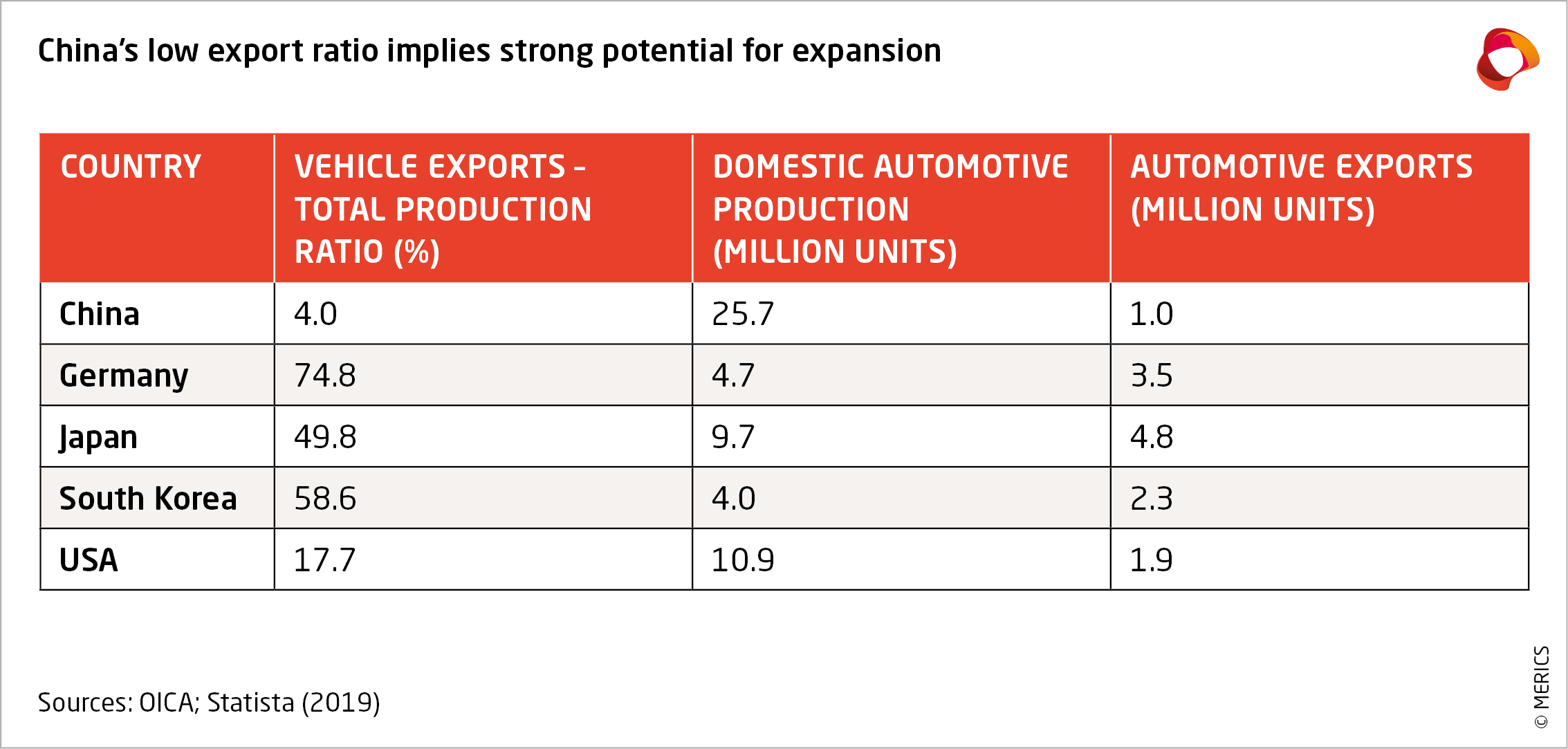

China’s huge domestic market means it is unlikely ever to export as much of its output as Germany, Japan, or South Korea. However, it is feasible that China will export 10 to 15 percent of its output within the next five to ten years, provided that both Chinese and foreign carmakers start to use China as an export base. If China’s domestic market stays at around 25-30 million units, that could translate to 2.5 to 3.5 million exported units per year.

2. China's EV expansion centers on Europe

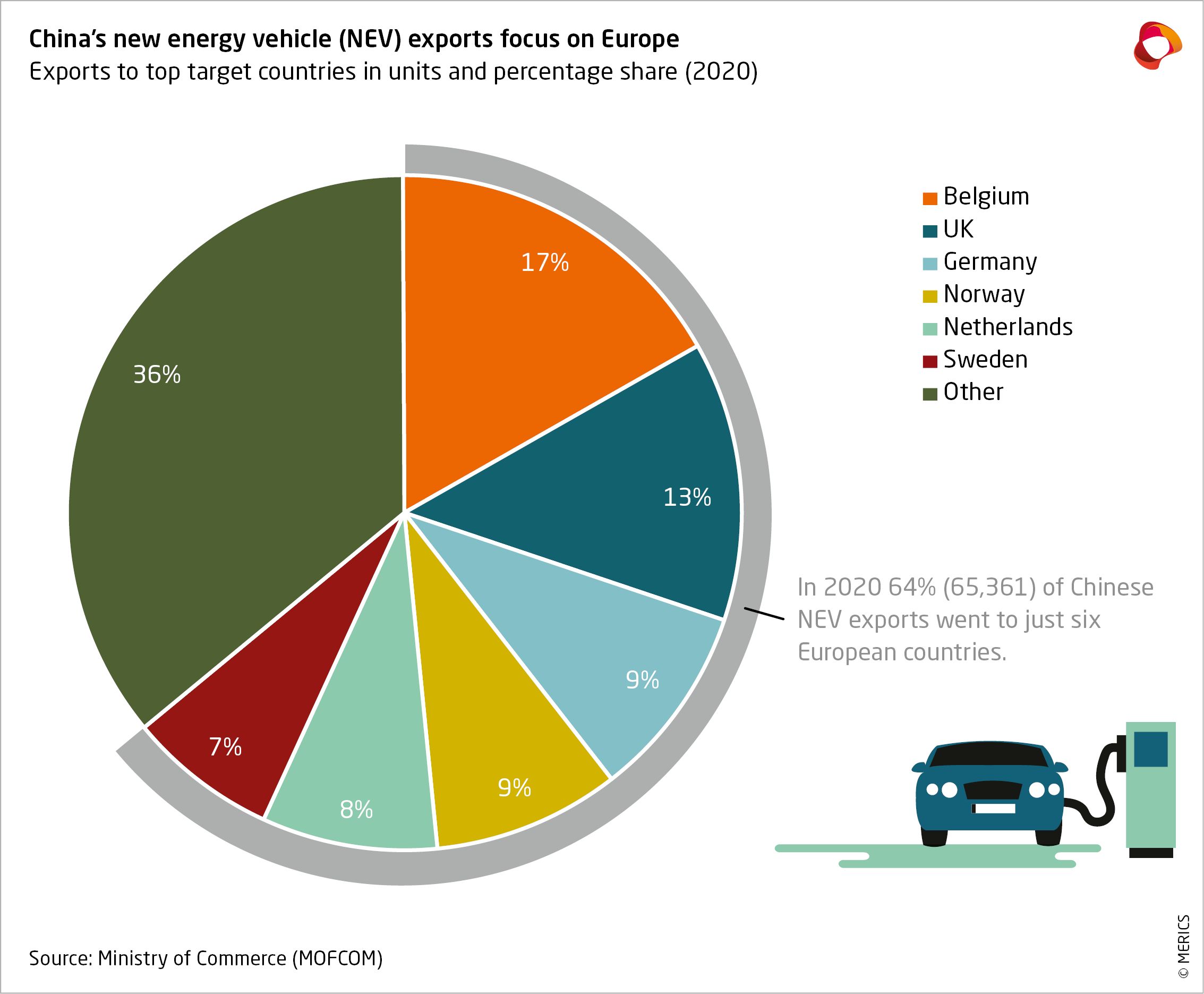

Europe has become the main destination for China’s EV export push (see exhibit 5). Chinese EV makers are now trying to replicate domestic success in Europe, where an ambitious green agenda necessitates widespread EV adoption. European countries now offer high purchasing subsidies for EVs and there is increasing momentum for a European phase out of internal combustion engine (ICE) vehicles.5 Aside from China, Europe also has the most advanced charging infrastructure.6 Chinese EV makers use Norway as bridgehead to Europe, because EV adoption is most advanced there; 80 percent7 of new vehicles are EVs and various benefits and subsidies are in place to promote supply and demand, including no import taxes on EVs.8

Politics also matter. China’s government shares the EV makers’ view that it is crucial to make inroads into developed markets for prestige and branding. In addition, while European governments are increasingly concerned about the economic rise of China, they remain more welcoming to Chinese actors than the United States. Europe continues to be an attractive investment location for Chinese companies.

Chinese carmakers have established R&D and design centers in Europe to facilitate their entry into European markets. Doing so enables them to prepare for European regulations and to tailor software and design solutions to European customers. These R&D centers also work as a feedback-loop to China and can influence design decisions back home; for instance, NIO uses its Munich team to design its vehicles (see exhibit 6).

China’s government has learnt from the failed export push in the 2000s; it now helps Chinese carmakers to test their vehicles under European conditions. In 2019, the China Automobile Engineering Research Institute (CAERI) set up the first Euro NCAP co-approved test facility outside Europe. The new testing facility was established in Chongqing’s Liangjing New Area, a pilot area focused on promoting Chinese automotive exports. It enables Chinese carmakers to finetune their vehicles before exporting to Europe, thereby avoiding disastrous safety ratings. A second Chinese Euro NCAP testing facility has been established in 2021.9

3. China's government and EV makers aim to use their first mover advantage to explore overseas markets

China’s central government, local governments and Chinese companies are united in their drive to expand globally – albeit for different reasons. The government has set overarching global expansion and export targets and offers guidance and subsidies to carmakers in China. Chinese carmakers are pursuing different strategies such as exports or overseas greenfield investments to enter overseas markets.

3.1 Government guidance is driving the globalization of China’s automotive sector

For the central government, the automotive industry is of strategic importance as its crucial to both the economy and national security. The government invests heavily (an estimated USD 58.7 billion between 2009 and 2017)10 in this sector due to its dual-use nature. So far, the investments have paid off, as China is now home to the world’s leading EV market. Next, it wants China to absorb larger parts of global value chains (GVCs). That is the entire range of activities required to bring a product to the consumer, including R&D and production of key components such as batteries and smart car technologies.

Both this current export push and the previous one in the 2000s were guided by the central government. In the mid-2000s, the goal was to turn several automotive production hubs, such as Chongqing and Shenyang, into export bases. The central government has now given the provinces a freer rein. That means it is up to provincial governments to take initiative, publish automotive policies and incentivize local carmakers to export. Meanwhile, the central government encourages carmakers to establish overseas R&D centers, acquire foreign carmakers and use the window of opportunity offered by China’s EV dominance to build exports (see Annex 1).

3.2 Provincial governments push local carmakers to go abroad to gain growth for their regions

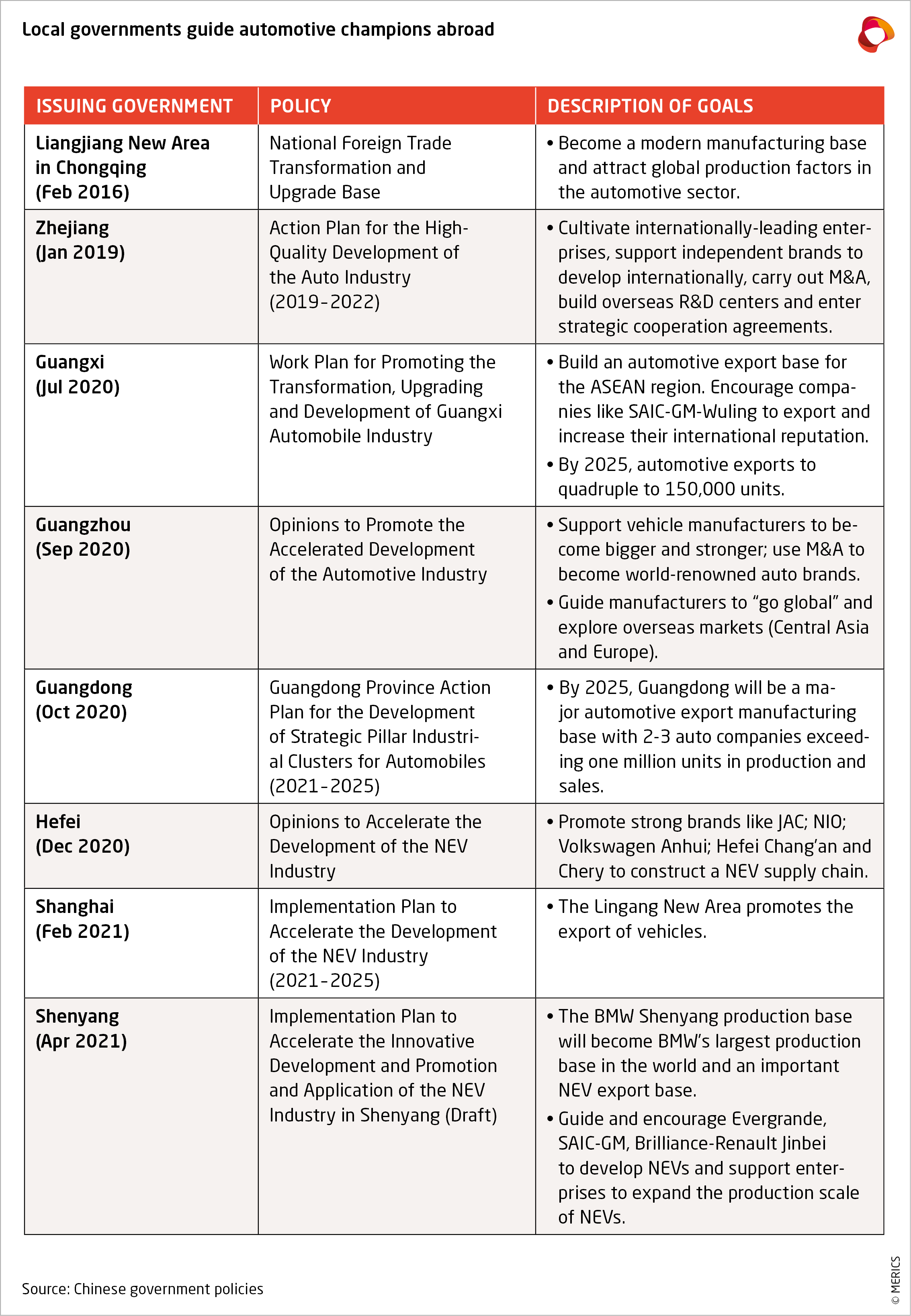

While the central government has refrained from consolidating the EV sector, local governments are not hesitating to pick winners. They are eager to gain status with central government by fulfilling targets, but their main incentive is to increase local investment and create jobs. They guide and encourage their local champions to go abroad to further drive sales and earn prestige (see Annex 2). As long as production occurs in their turf, local governments are not too concerned about the ownership of their local champion.

Local governments in Guangdong’s capital of Guangzhou and in Hefei, Anhui province, have thrown their weight behind local champions which they support financially and in the case of NIO even saved from bankruptcy. Xpeng Motors is a Guangzhou-based EV maker, while NIO is headquartered in Shanghai but has built its vehicle-production R&D center in Hefei. Local subsidies have helped the EV makers to scale up production to serve global markets (see exhibit 7). And BMW is being wooed by Shenyang city in north-eastern Liaoning province, which wants to become an important export base for the German carmaker.

3.3 Chinese EV makers accelerate export plans to tap into overseas EV demand

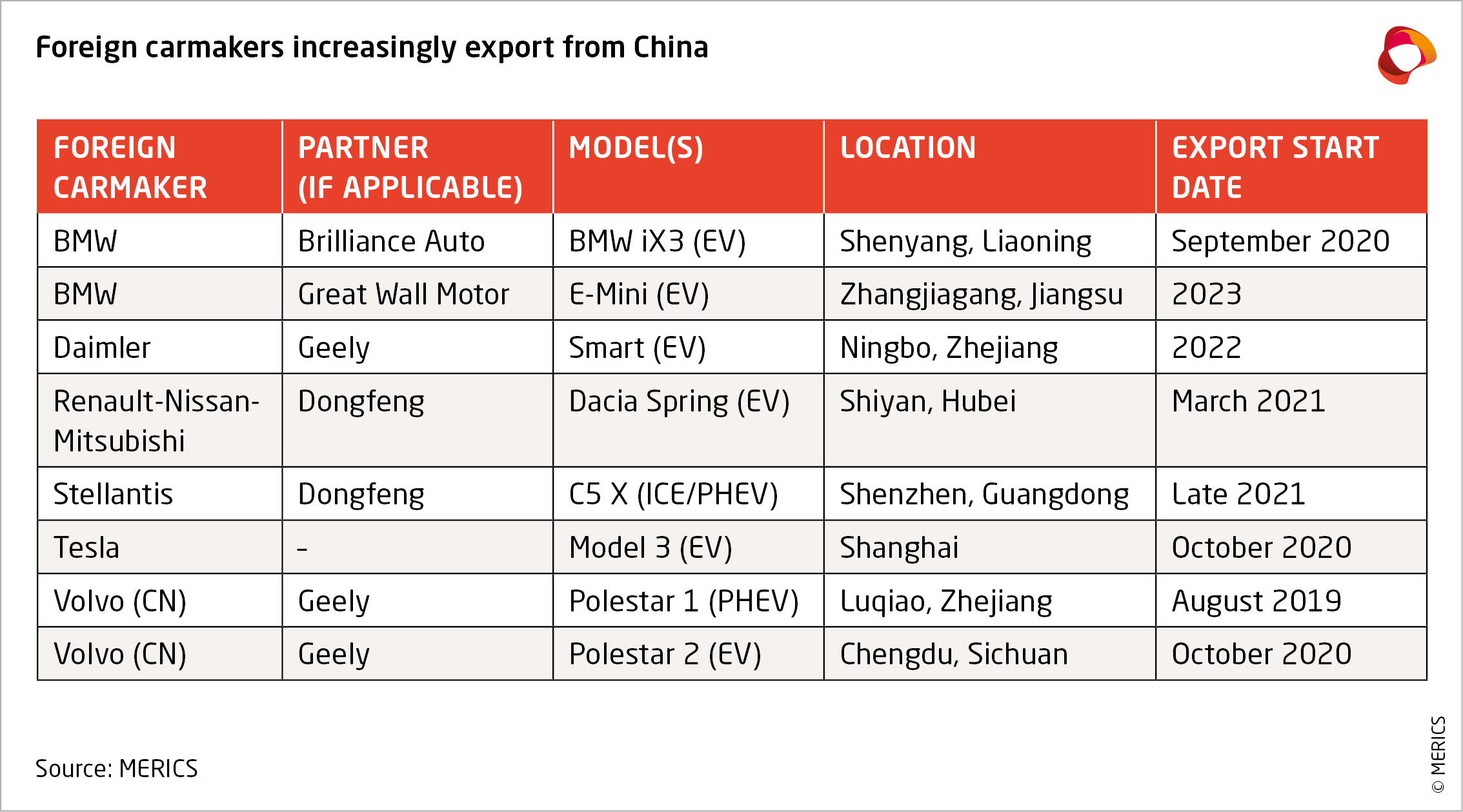

In recent months, Chinese EV makers have announced export and global expansion plans. Developed markets in Europe and North America are the main targets (see exhibit 8 for Europe). The ownership of Chinese carmakers has diversified since the previous export push. EV makers are overwhelmingly private, although state ties remain strong. Chinese EV makers pursue different strategies to expand globally, ranging from exports to acquisition of foreign companies.

3.4 Chinese Carmakers’ “Going Global” Strategies

Strategy 1: Exports

Exports can enable Chinese EV makers to enter markets quickly and have comparatively low initial capital requirements. Exporters benefit from local subsidies and higher capacity utilization of their factories in China, though margins are trimmed by the costs of logistics and tariffs (the EU has a 10 percent tariff on EVs). Export strategies generally rely on a local partner for sales and service infrastructure, which lessens the exporter’s understanding of local market conditions. Naturally, exports can also become potential targets in trade disputes.

Examples: Chinese EV maker WM Motor is not yet exporting but has already started to build export collaborations with well-known global partners. It has paired with Enel X11, a subsidiary of Italian power company Enel, to provide after-sales services for WM vehicles, smart charging solutions and help with vehicle-to-grid applications. WM Motor also has a tentative agreement with Uber which could see it supply EVs to Uber drivers in 10 European countries.12

Strategy 2: “Exports +”

To reduce their reliance on local partners and improve their understanding of overseas markets, Chinese carmakers have begun to supplement their export strategies with initial overseas operations. These may include R&D centers, showrooms or warehouses. EV makers who take this two-pronged approach can tailor products to overseas customers while continuing to benefit from subsidies and greater capacity utilization in China.

Examples: NIO plans to set up its own sales and service network in Europe13 and transfer its NIO App to Europe.14 NIO has announced to open showrooms in Norway (NIO houses) featuring its battery swapping station to win over customers by highlighting its technological capabilities. By the end of 2022, its battery-charging and swapping system is expected to be available in Norway. In July 2021, Certification agency TÜV Rheinland issued certifications allowing NIO to sell and operate its swapping stations in all EU member states. The EV maker wants to make 1,000 of them operational outside of China by 2025.15

Strategy 3: Overseas production

Overseas production can help companies avoid tariffs, trade conflicts and transportation costs and foster political relations with local governments. Chinese battery makers have started to build plants in Germany to get closer to their customers (i.e., foreign carmakers), which provides a template for export strategies of China’s EV makers.

Examples: In Italy, China’s giant automaker FAW Group is setting up a luxury EV maker in the north Italian city of Reggio Emilia, Silk-FAW. The joint venture brings together state- owned FAW and Italian engineering and design company Silk EV. They aim to produce an EV racing car under the Hongqi marque, whose name translates as “Red Flag” and is steeped in CCP tradition. The JV plans to invest more than EUR 1 billion over three years. Production is expected to begin in 2023.

The EU’s periphery has caught the attention of another giant Chinese state enterprise, Changan. In Georgia, Changan and local AiGroup will open an EV plant in 2022, with a capacity of 40,000 units, half of which are destined for export to the EU.16 For Chinese carmakers, Georgia is an attractive investment location due to its cheap workforce, geographic position on the Belt and Road Initiative (BRI) and free trade agreement with the EU which gives EVs tariff-free access to EU markets.

Strategy 4: Acquisition of a foreign carmaker

Acquiring a foreign carmaker enables Chinese carmakers to jump-start their global expansion. It is an opportunity to leverage well-known brands, use existing production facilities, international market experience and technological know-how. Such acquisitions are often encouraged and supported by the Chinese government. The European automotive sector remains largely open for foreign investment from China. However, FAW’s failed acquisition of Italian truck maker Iveco SpA after the Italian government declared heavy trucks a “strategic national interest” highlights that national security concerns, including issues of future economic competitiveness, may be coming to the fore.20

Examples: SAIC could expand its EV exports by leveraging the British brand MG Motor, which it acquired in 2007. The China-made ZS EV has received stellar safety ratings and is available in countries around the world.21 SAIC also produces MGs in Thailand and India for sale in Asian markets.

3.5 Significant hurdles for Chinese EV makers remain

Failure seems inevitable for most of these Chinese EV firms. As Chinese carmakers leave the home environment, each strategy comes with strengths and weaknesses. Only those that successfully overcome the following hurdles will have a chance of success:

- Lack of international experience: Most Chinese carmakers lack an overseas sales and after-sales service network. Without one, it is hard to attract customers, especially if they don’t recognize the brand or fear complicated maintenance procedures.

- The politicization of trade: China’s economic rise will bring greater overseas scrutiny of Chinese EV-makers. Foreign governments have started to adopt new measures focused on procurement,22 investment, market access or tariffs that could impact China’s EV makers.

- Navigate local regulations: The mounting automatization of cars creates new regulations on data23 that could prove difficult for Chinese EV makers to navigate. Global trends to complicate data transfers abroad can create additional costs.

- Challenge established local companies: The first-mover advantage held by China’s EV makers is disappearing fast as entrenched carmakers start to churn out EV models. In Europe, Chinese EV makers will have to compete on home ground with major automotive producers like Daimler and Stellantis, the Dutch-based group formed from the 2021 merger of Fiat-Chrysler and French group PSA whose brands include Peugeot and Citroen.

4. China incorporates foreign carmakers into its export strategy

China’s automotive export strategy also involves foreign carmakers, who view the leading EV market as a source of innovation that they can integrate into their global production layout. In fact, they have advantages such as international experience, data on European and US consumers and larger networks that make them well suited to export more successfully than their Chinese counterparts. China’s government has recognized this potential and seeks to use foreign carmakers to increase its share of global value chains.

4.1 Chinese policymakers supports foreign carmakers to absorb GVCs

China had initially hoped to imitate South Korea by forcing foreign carmakers into joint ventures (JVs). It was a strategy that built up national champions through subsidies, picking winners and restricting market access for foreign manufacturers. However, China’s SOEs have struggled to use JVs to build self-owned brands. Foreign carmakers now account for 60 percent of China’s domestic automotive market. Their dominant position has created an impetus to include them in China’s export strategy. If successful, the benefits of this strategy would stretch across the entire value chain including upstream industries such as steel, machinery, chemicals and electronics.

China has relegated its ambition to build national auto champions in favor of absorbing GVCs, fostering industrial upgrading and stimulating domestic innovation. The Made in China 2025 (MiC25) strategy launched in 2015 and the mid-to-long-term Automotive Plan (2017) specifically called for Chinese brands to become world leaders. However, more recent policies have shifted to prioritize using foreign carmakers as a catalyst to transform China into an automotive export hub:

- The 15-year New Energy Vehicle (NEV) Development Plan (2021-2035) outlines the “Open Development Concept” which aims to “bring [foreign carmakers] in” and help foreign and Chinese carmakers to “go out” and expand globally.

- Under the Dual Circulation Strategy (2020), China’s policymakers want to utilize the huge domestic market as a magnet to attract global production factors.

- The 14th Five-Year-Plan (FYP) (2021) seeks to attract and better utilize foreign investment.

- In March 2021, on a tour in Fujian Province President Xi Jinping drove that message home: “If you contribute to innovation in China, China will fully support you, regardless of where you come from.”24

China’s policymakers are gradually removing JV requirements in order to make it more attractive for foreign carmakers to use China as an export hub. For instance, Tesla was able to become a wholly foreign owned entity and to start construction on its huge “Gigafactory” in Shanghai in 2018. Without JVs, foreign carmakers can operate more autonomously and take home a greater share of their profits, incentivizing them to produce and export more.

4.2 China’s innovative market attracts foreign carmakers to use it as an export hub

Previously, foreign carmakers mainly produced in China to sell in the Chinese market, but their motivations are starting to change. Lured by China’s attractive EV market, foreign carmakers are starting to use the country as an export hub (Exhibit 10). For Tesla, China is already the “primary vehicle export hub.”25 BMW and Volvo have also started exporting to Europe, while others like Daimler are ramping up production and research capacities for export purposes and more are interested. For instance, GM26 has expressed interest and the Changan-Ford JV’s executive vice president Zhao Fei has said that “China will become one of Ford's most important export bases in the world in the future.”27 Volkswagen has not yet announced plans to export from China to Europe, but in 2018 it trialed exports to southeast Asia.28 In a nutshell, foreign carmakers no longer view China as a market where you can sell foreign, sometimes outdated, technology but now as one at the forefront of innovation. This change mainly stems from China’s industrial policy that, to leapfrog advanced manufacturing countries, has guided consumers and producers to focus on EVs.

Foreign carmakers are drawn to help transform China into an export hub for the following reasons:

- Innovative market: Foreign carmakers regard China as a “significant market for new technologies and an important purchasing market,”29 according to Daimler. And BMW chairman Oliver Zipse recently hailed China as a key source of innovation.30 To benefit from the dynamic market, foreign carmakers are integrating China into their global R&D and production layout. They build new R&D facilities and production centers and enter EV or autonomous driving related development partnerships with Chinese companies to increase the quality of their products for global markets. They also use China as a testing ground for global products. In 2019, Renault and Dongfeng released the electric K-ZE in China and now Renault is planning to export the Dacia Spring EV (based on the K-ZE) from China to Europe.31

- Evolving tech ecosystem: China’s tech ecosystem is developing rapidly under the auspices of tech giants like Baidu and Alibaba and the Chinese government’s “new infrastructure initiative”. This digital and smart infrastructure push is highly relevant for automotive firms as it includes public financing in the realm of USD 1.4 – 2.5 trillion for 5G base stations and EV charging stations.32 No wonder then, that foreign carmakers want to participate. The digital infrastructure allows them to test and deploy innovative electric and autonomous models. BMW has entered a partnership with State Grid Service EV, a SOE, to provide charging piles in China and to develop and promote charging standards globally.33

- Highly competitive manufacturing system: Foreign carmakers have in recent years invested heavily in their Chinese production facilities. This has resulted in state-of- the-art plants that use Industry 4.0 technologies34 incorporating ever-higher levels of digitalization and AI. Volkswagen opened its new Anting plant near Shanghai in 2020, the group’s first mass-production site for EVs using VW’s innovative EV modular production system. VW plans to start EV production at another new plant in Hefei in 2023. The benefits are amplified by proximity to important suppliers such as battery makers like CATL and lower production costs in China.

- Supportive government: Government policies and support underpinned the emergence of China’s EV charging infrastructure and consumer demand for EVs. China’s government also provides foreign companies with loans, subsidies and preferential taxes if they base production and R&D there; some provinces hand out additional benefits to carmakers based on production volumes. In March 2020, the National Development and Reform Commission (NDRC) assisted foreign-invested companies in resuming production.35

- Production capacity: For Korean carmaker Kia, exporting from China became a necessity (31,900 units in 2019) after its China sales shrank by 20 percent in 2019, leaving some production plants at below 50 percent capacity. Other carmakers, such as VW, have deliberately added production capacity despite a stagnant Chinese automotive market. Such moves could signal export intentions.

- Focus on regional integration: China is eager to conclude free trade agreements (FTAs) that can help it become an automotive export hub. In 2015 China and Australia signed an FTA under which Australian automotive tariffs were cut from five to zero percent.36 China and ASEAN concluded the Regional Comprehensive Economic Partnership agreement in 2020, and in the 14th FYP China has reiterated its intention to join additional FTAs.

China’s goal of absorbing GVCs, and thereby upgrading and strengthening its economy, is aided by foreign carmakers manufacturing for export there. BMW’s joint venture with Brilliance Auto is a strong example of what the Chinese government hopes to achieve. In April 2018, the NDRC announced the timetable to lift JV requirements in the automotive sector. Three months later, BMW Brilliance announced it would expand capacity at its two Shenyang plants to export the full-electric iX3 from China. Soon after, in October 2018, BMW increased its stake in the JV to 75 percent. In September 2020, the first iX3 rolled off the Shenyang production line. The benefits of the export push extend across the supply chain. Vehicle development is taking place locally as the JV partners have run a R&D center in Shenyang since 2017. Local suppliers and national champions can also profit: CATL supplies cells to the JV’s new battery center.

4.3 Foreign carmakers have an opportunity to export successfully from China

Foreign carmakers are establishing themselves as important exporters. According to China’s Ministry of Commerce (MOFCOM), foreign carmakers’ JVs accounted for nearly 30 percent of China’s total automotive exports in 2020, up from 27 percent in 2019. This data excludes Tesla, a wholly foreign-owned entity that in May this year exported 14,000 EVs and 11,500 in June which amounts to 57.5 percent of China’s total EV exports.37

Indeed, foreign carmakers are well-positioned to outperform their Chinese competitors. While China’s EV makers can churn out high-quality vehicles, foreign carmakers are catching up fast. They possess international experience, data on European and US consumers, and a global sales and after-sales services network. Most importantly, compared to newcomers like NIO and Xpeng, they have the necessary scale to produce and ship thousands of vehicles per month. Politically, they are less pressured to prioritize exports for exports’ sake, a factor that may bear down on Chinese EV makers. Hence, the export strategies of foreign carmakers are more likely to be attuned to actual market opportunities.

To support China’s industrial upgrading and fuel economic growth, the central government wants to attract more foreign investment, particularly in the automotive sector and in innovation. MOFCOM is drawing up a five-year plan dedicated to increasing foreign investment. Amid increasing geopolitical friction, China’s policymakers have refrained from punishing foreign companies in the auto sector, which they view as important growth engines.

5. China's EV sector will change global production patterns

China’s push to become an EV exporter is set to transform the global automotive sector. China’s market has been shaping automotive trends for some years now, setting up trends that have rippled out into wider changes. China has surpassed its early status as the world’s manufacturing hub and is emerging as a global center of automotive innovation that will profoundly influence overseas markets.

- Auto exports signal China is moving up the value chain: Overseas demand for high- quality, made in China goods, such as vehicles, is rising as acceptance has grown.38 In the EV sector, Chinese models have achieved high safety ratings and use technologies like battery swapping and autonomous driving that entrenched carmakers have not yet been mastered. For customers, China’s advances are beneficial as increased competition helps to improve the quality of EVs overall. As first movers, Chinese EV makers also have an opportunity to influence global standard setting.

- Chinese exports could shake up Europe’s auto sector: Chinese EV exports could deepen the divide between European companies present in China and those who are not. Firms that lack a presence in China will face greater competition from Chinese brands. They will also risk losing out on the attractive dynamism of China’s EV sector and access to the biggest EV market. Carmakers most likely to be hurt include Stellantis, which has a weak foothold in China, and smaller suppliers who cannot afford the upfront costs to localize their production in China. Others who are actively supplying both foreign and Chinese carmakers in China, like Bosch and Continental, stand to gain from this export dynamic. An estimated 70 percent of NIO’s suppliers are foreign companies.

- Europe’s competitiveness as an industrial location may be at risk: The European Commission regards the automotive sector as “crucial for Europe’s prosperity.” However, Chinese automotive exports could distort markets and threaten Europe’s industrial heartlands. Motor vehicle manufacturing employs 3.5 million people in the EU, they are the most directly threatened. For now, European EV sales rankings are topped mainly by European-made electric vehicles or Teslas. However, subsidy-supported Chinese EV exports are on the rise globally so Europe’s export-oriented auto sector may encounter problems.

- EVs first, ICE second? China could position itself to absorb traditional internal combustion engine (ICE) GVCs. While the global market share of EVs is rising rapidly, not all countries or regions want or will be able to phase out ICEs soon. So far, China has not committed to a national phase out. This could be for strategic reasons. If European governments ban ICEs, carmakers may look for ways to shift production closer to consumers. Geely and Daimler are already considering engine exports from China. And in 2022, JV restrictions in the ICE sectors will be lifted, paving the path for foreign companies to shift ICE production for exports to China.

- Tough choices ahead - European carmakers will need to balance production between China and Europe: While European carmakers are doubling down on production in China, they will not shift entirely. Despite the attractive market environment in China, they worry about increasing their dependency on the Chinese government, especially as the CCP is extending its reach into private firms. They also fear push-back in Europe, where labor unions have voiced opposition. Production in Europe has benefits and can curtail fears about cyber-espionage and data transfer that production in China entails. Foreign carmakers will decide on a strategic case-by-case basis which cars they produce for export in China.

- Harmonizing the quest for absorbing global value chains and building national champions: For now, the EV market is growing rapidly, leaving ample room for foreign and Chinese carmakers to exist side-by-side. However, competition will increase rapidly as more players are entering the field and China is beginning to phase out subsidies. For now, China’s government is content to let foreign carmakers occupy a large share of the market in exchange for locating value chains in China. However, foreign carmakers should keep in mind that if China’s government relegates their ambition to build national champions in favor of taking a greater share of global automotive supply chains, that choice is likely to be a temporary one.

Annex

- Endnotes

-

1 | International Organization of Motor Vehicle Manufacturers (OICA). “2020 PRODUCTION STATISTICS.” https://www.oica.net/category/production-statistics/2020-statistics/. Accessed: July 27, 2021.

2 | This text follows the Chinese definition of new energy vehicles (NEVs) when speaking about electric vehicles. That definition includes battery electric vehicles (BEVs), plug-in hybrid electric vehicles and fuel cell electric vehicles (FCEV).

3 | Note: In 2020, 89 producers acquired New Energy Vehicle (NEV) points in China’s NEV quota system according to this list from the Ministry of Industry and Information Technology (MIIT). The average is calculated by dividing the EV production number in 2020 (CEIC data) by these 89 producers. MIIT

(2021). 关于2020年度乘用车企业平均燃料消耗量与新能源汽车积分情况的公示(Announcement on the average fuel consumption of passenger car companies and the points of new energy vehicles in 2020). April 9. https://www.miit.gov.cn/zwgk/wjgs/art/2021/art_b9af4dc446ec41bda9b843cb7716f31b.html. Accessed: July 27, 2021.4 | China’s Passenger Car Association (CPCA) (2021). 【月度分析】2021年4月份全国乘用车市场分析 ([Monthly Analysis] National Passenger Car Market Analysis in April 2021). May 11. https://www.cpcaauto.com/ newslist.asp?types=csjd&id=11761. Accessed: July 27, 2021.

5 | Randall, Chris (2021). “Nine European nations call for EU combustion phase-out.” March 11. https://www.electrive.com/2021/03/11/nine-european-nations-call-for-eu-combustion-phase-out/. Accessed: July 27, 2021.

6 | McKerracher, Colin (2021). “EV Charging Data Shows A Widely Divergent Global Path.” March 23. https://www.bloomberg.com/news/articles/2021-03-23/ev-charging-data-shows-a-widely-divergent- global-path. Accessed: July 27, 2021.

7 | Holland, Maximilian (2021). Norway Plugin Electric Vehicles Take Over 80% Share In April. May 4. https://cleantechnica.com/2021/05/04/norway-plugin-electric-vehicles-take-over-80-share-in-april/. Accessed: July 27, 2021.

8 | Norsk elbilforening. Norwegian EV policy. https://elbil.no/english/norwegian-ev-policy/. Accessed: July 27, 2021.

9 | China Automotive Technology and Research Center (CATARC) (2021). CATARC is Co-Approved for Euro NCAP Crash Test and Pedestrian Impact Test in China. February 18. http://europe.catarctc.com/en/ content?id=29. Accessed: July 27, 2021.

10 | Kennedy, Scott (2020). The Coming NEV War? Implications of China’s Advances in Electric Vehicles. November 18. https://www.csis.org/analysis/coming-nev-war-implications-chinas-advances-electric-vehicles. Accessed: August 17, 2021.

11 | Enel (2020). Enel X signed strategic agreement with Weltmeister to boost electric vehicle exports. December 30. https://www.enel.com/media/explore/search-press-releases/press/2020/12/-enel-x-

signed-strategic-agreement-with-weltmeister-to-boost-electric-vehicle-exports-. Accessed: July 27, 2021.12 | Zhang, Phate (2020). WM Motor, Uber reach tentative agreement, models may be exported to Europe. November 25. https://cntechpost.com/2020/11/25/wm-motor-uber-reach-tentative-agreement-models-may-be-exported-to-europe/. Accessed: July 27, 2021.

13 | Parikh, Sagar (2021). Nio ES8 Norway launch this year, ET7 to follow in 2022 [Update]. July 23. https://topelectricsuv.com/news/nio/nio-overseas-launch-plan/. Accessed: July 27, 2021.

14 | NIO (2021). NIO Announces Norway Strategy. May 6. https://www.nio.com/news/nio-announces- norway-strategy. Accessed: July 27, 2021.

15 | Randall, Chris (2021). Nio receives certification for battery swapping stations. July 9. https://www. electrive.com/2021/07/09/nio-receives-certification-for-battery-swapping-stations/. Accessed: July 27, 2021.

16 | Euronews (2019). Georgia’s EU bid stepped up with new electric car manufacturing plant. July 26. https://www.euronews.com/2019/07/26/georgia-s-eu-bid-stepped-up-with-new-electric-car- manufacturing-plant. Accessed: July 27, 2021.

17 | Gao, George (2009). Geely gets strong support from gov't for Volvo deal. December 31. http://autonews. gasgoo.com/china_news/1013528.html. Accessed: July 27, 2021.

18 | Volvo Cars (2020). Volvo Cars Made in China Exports to Europe in the First Half of the Year Increased by 1.8 Times. August 8. https://www.volvocars.com/zh-cn/about/our-company/brand-news/20200808.

Accessed: July 27, 2021.19 | Xinhua News (2021). 全国两会召开在即 李书福带来新能源汽车相关两项建议 (The National Two Sessions will be held soon. Li Shufu brings two suggestions related to new energy vehicles). March 3. http://www.xinhuanet.com/fortune/2021-03/03/c_1127160052.htm. Accessed: July 27, 2021.

20 | Reuters (2021). Italy industry minister welcomes end of talks on CNH's Iveco sale to China's FAW. April 17. https://www.reuters.com/article/us-iveco-m-a-faw-italy-idUSKBN2C40GB. Accessed: July 27, 2021.

21 | MG Motor (2021). Meet our parent company: SAIC Motor. January 29. https://news.mgmotor.eu/meet-our-parent-company-saic-motor/. Accessed: July 27, 2021.

22 | See: BYD (2020). Federal Transit Administration Clarifies Limits on Sale of BYD Buses. May 19. https://en.byd.com/news-posts/federal-transit-administration-clarifies-limits-on-sale-of-byd-buses/. Accessed: July 27, 2021.

23 | See: Council of the European Union (2019). Safer cars in the EU. November 8. https://www.consilium. europa.eu/en/press/press-releases/2019/11/08/safer-cars-in-the-eu/. Accessed: July 27, 2021.

24 | Xinhua News (2021). 习近平:抓创新不问“出身”,只要能为国家作出贡献都会全力支持 (Xi Jinping: To grasp innovation regardless of "origin", as long as they can contribute to the country, they will fully support). March 25. http://www.xinhuanet.com/politics/leaders/2021-03/25/c_1127252417.htm. Accessed: July 27, 2021.

25 | Yu Yifan (2021). Tesla makes record profit despite China headwind and chip crunch. July 27. https://asia. nikkei.com/Business/Technology/Tesla-makes-record-profit-despite-China-headwind-and-chip-crunch. Accessed: July 27, 2021.

26 | Sun, Yilei and Goh, Brenda (2020). Exclusive: GM thinks bigger in China with plan to import full-size SUVs. November 6. https://www.reuters.com/article/us-gm-china-exclusive-idUSKBN27M04V. Accessed: July 27, 2021.

27 | Day Day News (2020). Breaking the three-year “curse“ Changan Ford bottomed out?. July 14. https://daydaynews.cc/en/car/669842.html. Accessed: July 27, 2021.

28 | Volkswagen Group (2018). Volkswagen Group China plans to export With South East Asian markets as first step. January 12. https://www.volkswagenag.com/en/news/2018/01/VW_China_exports.html. Accessed: July 27, 2021.

29 | Daimler (2020). Annual Report 2019. February 19. https://www.daimler.com/documents/investors/ reports/annual-report/daimler/daimler-ir-annual-report-2019-incl-combined-management-report- daimler-ag.pdf. Accessed: July 27, 2021.

30 | Wei Xu (2021). BMW Chairman Hails China as Key Innovation Source. March 22. https://www.yicaiglobal. com/news/bmw-chairman-hails-china-as-key-innovation-source. Accessed: July 27, 2021.

31 | Automotive News Europe (2020). Renault's made-in-China Dacia EV angers French unions. October 22. https://europe.autonews.com/automakers/renaults-made-china-dacia-ev-angers-french-unions. Accessed: July 27, 2021.

32 | Wong, Dorcas (2020). How Can Foreign Technology Investors Benefit from China’s New Infrastructure Plan? August 7. https://www.china-briefing.com/news/how-foreign-technology-investors-benefit-from- chinas-new-infrastructure-plan/. Accessed: July 27, 2021.

33 | Li Fusheng (2020). BMW partners with State Grid EV Service to expand charging infrastructure. June 5. https://www.chinadaily.com.cn/a/202006/05/WS5ed9b5faa310a8b24115b1d9.html. Accessed: July 27, 2021.

34 | Volkswagen Group (2018). Volkswagen Group China builds first factory specifically designed for MEB production. October 19. https://www.volkswagenag.com/en/news/2018/10/VW_Group_China_MEB. html#. Accessed: July 27, 2021.

35 | NDRC (2020). 国家发展改革委关于应对疫情 进一步深化改革做好外资项目有关工作的通知 (NDRC’s Response to the Epidemic - Notice on Further Deepening Reform and Doing a Good Job in Foreign-funded Projects). March 9. https://www.ndrc.gov.cn/xxgk/zcfb/tz/202003/t20200311_1222902.html. Accessed: July 27, 2021.

36 | Australian Department of Foreign Affairs and Trade (DFAT). Free Trade Agreement Portal. https://ftaportal.dfat.gov.au/AUS/CHN/search/870380/8703?expanded=8708&searchTerm=870380. Accessed: July 27, 2021.

37 | Zhang, Hongpei (2021). Chinese vehicle exports grow robustly amid global chip shortage. July 1. https://www.globaltimes.cn/page/202107/1227598.shtml. Accessed: July 27, 2021.

38 | Innofact (2021). WIWO Studie: Chinesische Automarken Kommen nach Deutschland. Juni 21. https://v4.innofact-marktforschung.de/wiwo-studie-chinesische-automarken-kommen-nach- deutschland/. Accessed: July 27, 2021.

Author(s)

Senior Analyst, Rhodium Group and former Analyst, MERICS

Author(s)

Senior Analyst, Rhodium Group and former Analyst, MERICS

Content