picture alliance / Long Wei / Costfoto

Content

Executive Summary: Fragmented Europe: Dealing with China as a technology and innovation power

You are reading the Executive Summary of the 2026 report of the European Think Tank Network on China (ETNC) "Fragmented Europe: Dealing with China as a technology and innovation power". Go back to the main page.

By Claudia Wessling and Bernhard Bartsch

China’s drive to become a global leader in science, technology and innovation has huge implications for the EU and its member states. On the one hand, China is becoming a strong competitor in industrial high-tech sectors and innovative science that used to be the stronghold of European actors. Advanced digital technologies made in China also increasingly pose risks to infrastructures in Europe. On the other hand, China offers itself as a resourceful counterpart for collaboration in research and development (R&D) and keeps attracting European scientists and businesses alike.

This report, the 12th compiled by the European Think-tank Network on China (ETNC), analyses how Europe is affected by China’s rise to a technological power and its increasing clout in shaping and creating innovation. Authors from 22 European countries have contributed to this study. The goal is to provide a nuanced picture of how those states interact with China in the field of innovative technologies, and to identify commonalities and differences in how they are affected.

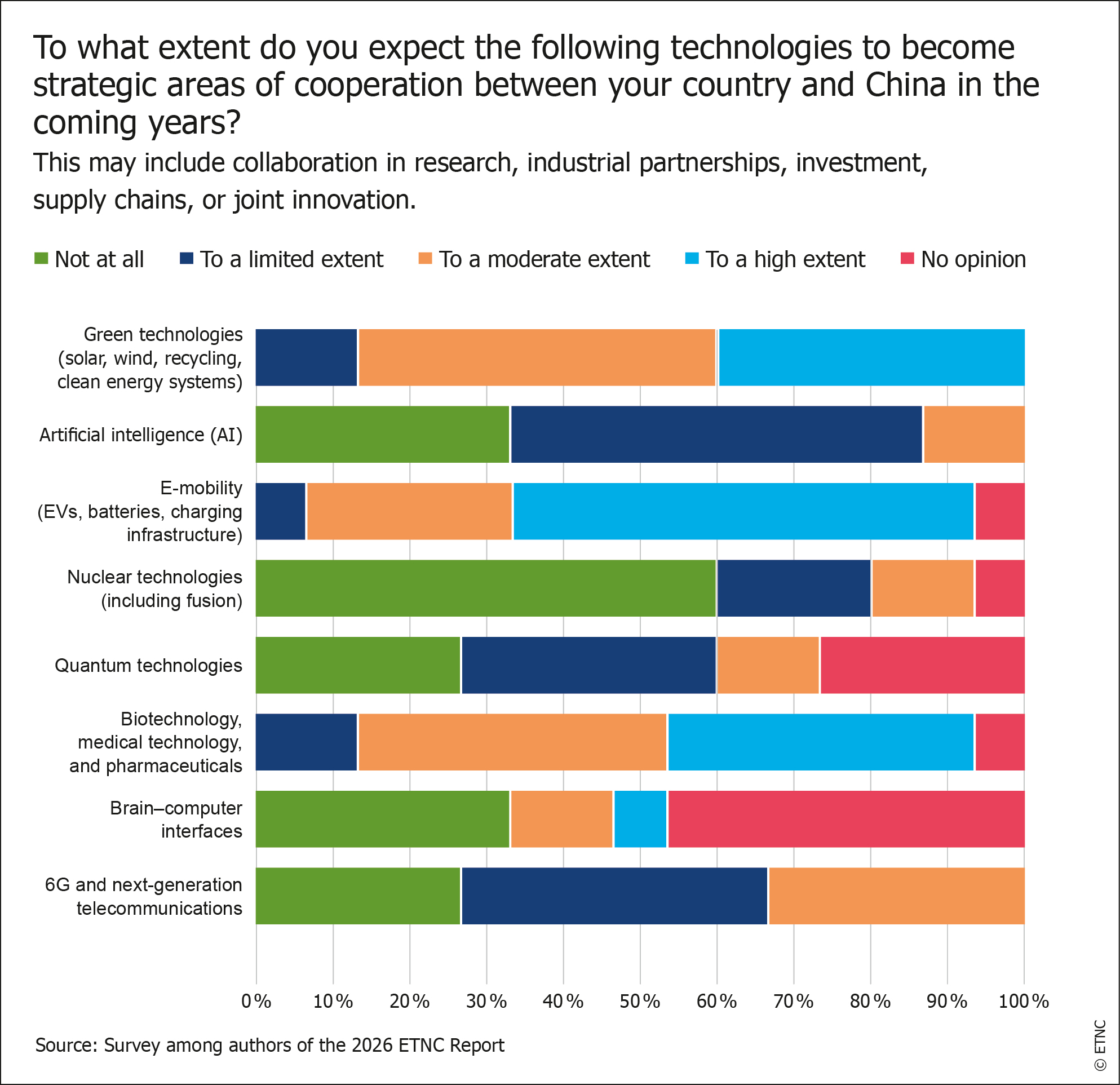

Persistent technology and innovation policies have made China a strong competitor for Europe

In 2024, China surpassed the US in R&D spending, and has, in recent years, made great strides to innovate in sectors like energy, e-mobility and increasingly also robotics. China is not only building its 5G technology into telecommunications infrastructures across the globe, it also actively shapes the future standards in this sector. China looks set to become a key player in AI development, both in basic research and industrial or consumer applications. According to the technology tracker of the Australia-based think tank ASPI, China leads in 66 of 74 underlying research systems of new technologies tracked.

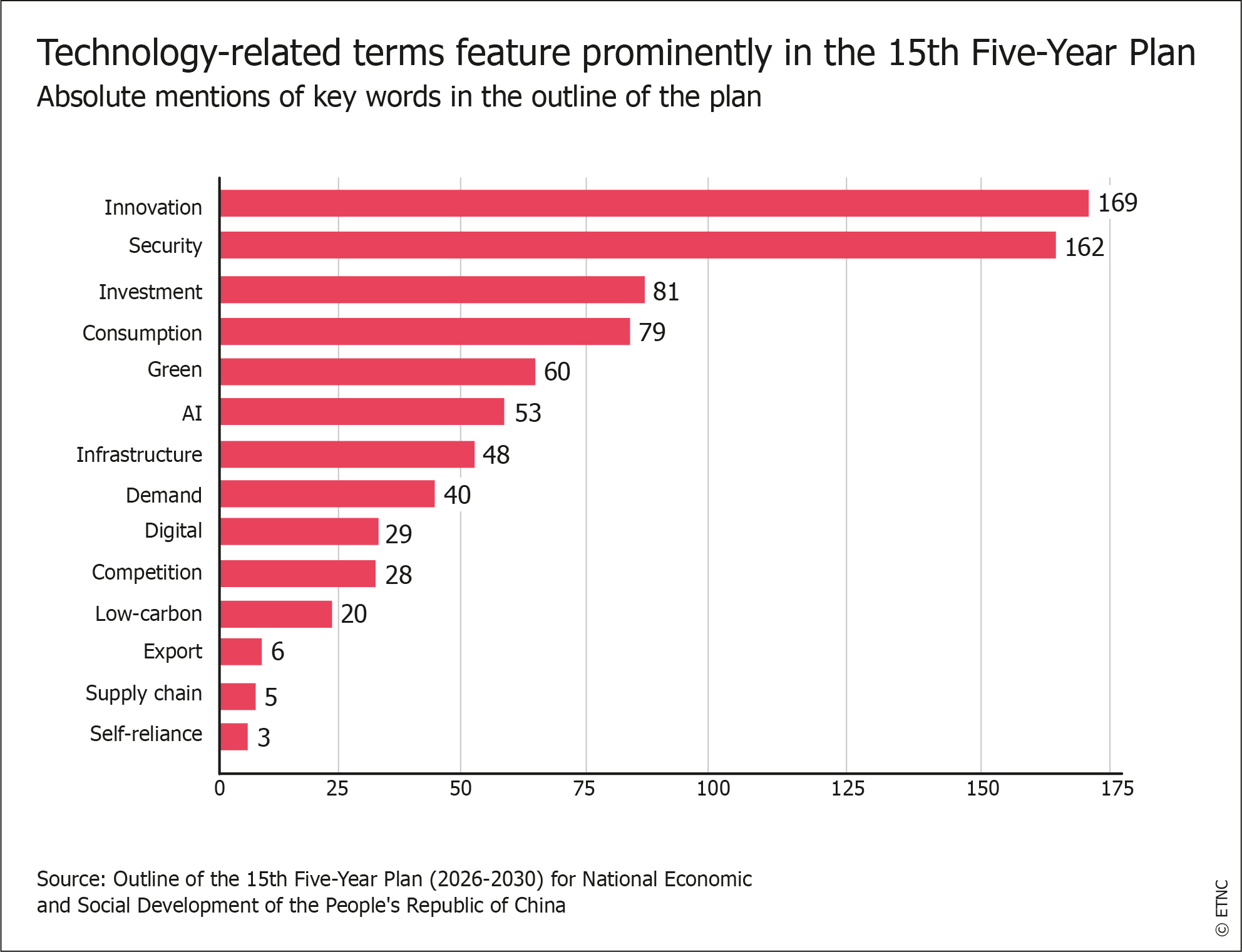

The 15th Five-Year Plan (FYP), published at the National Peoples’ Congress in March 2026, marks a significant intensification of China’s challenge to Europe’s technological competitiveness in the coming years. The plan outlines bold strategies and steps to become a leader in high-tech fields and upgrade China’s industry. Technological self-reliance is a key goal of the plan, with China aiming to become stronger and more self-sufficient in AI development, by improving the related research and the required ICT infrastructure of hard- and software systems.

The Five-Year Plan also emphasizes the need for “landmark achievements” and a marked increase in the number of technology fields in which China strives to become a global leader. One case in point is green tech: Beijing wants to double its world-leading solar and wind capacities in the next decade.

In addition to renewable energy, China also invests heavily in emerging sectors such as quantum technology, hydrogen, nuclear fusion as well as brain-computer interfaces. For instance, in 2025, China created the Government Guidance Fund (GGF) to provide funding of one trillion Chinese Yuan (EUR 127 billion) to emerging tech fields to include quantum computing, biotech, embodied AI and next-generation wireless networks1.

Securing control of innovation value chains is another key strategic goal. China will prioritize the procurement of innovative products from domestic origin to support the development of its high-tech industry. The party stresses that it expects both companies and research institutions to engage in a “new-style whole of nation system” that “concentrates resources to do great things.” In this spirit, national champions like semiconductor maker SMIC, tech giant Huawei or battery maker CATL are expected to play along and to co-innovate with tech unicorns, small- and medium-sized enterprises, and research labs in comprehensive industrial clusters.

Apart from targeted innovation policies, the Chinese government has also been using technology transfer, comprehensive subsidies and industrial policies to nurture its own development. The EU and its member states, as of now, are still crucial for China to achieve many of its goals, because their universities offer top-notch research and their highly specialised companies (called “hidden champions” in some regions) produce high-tech components China still needs to import. But the E-mobility and solar sectors show that the tables are beginning to turn and that China is becoming a strong competitor.

The EU’s approach is shifting from unconditional openness to stronger emphasis on economic and research security

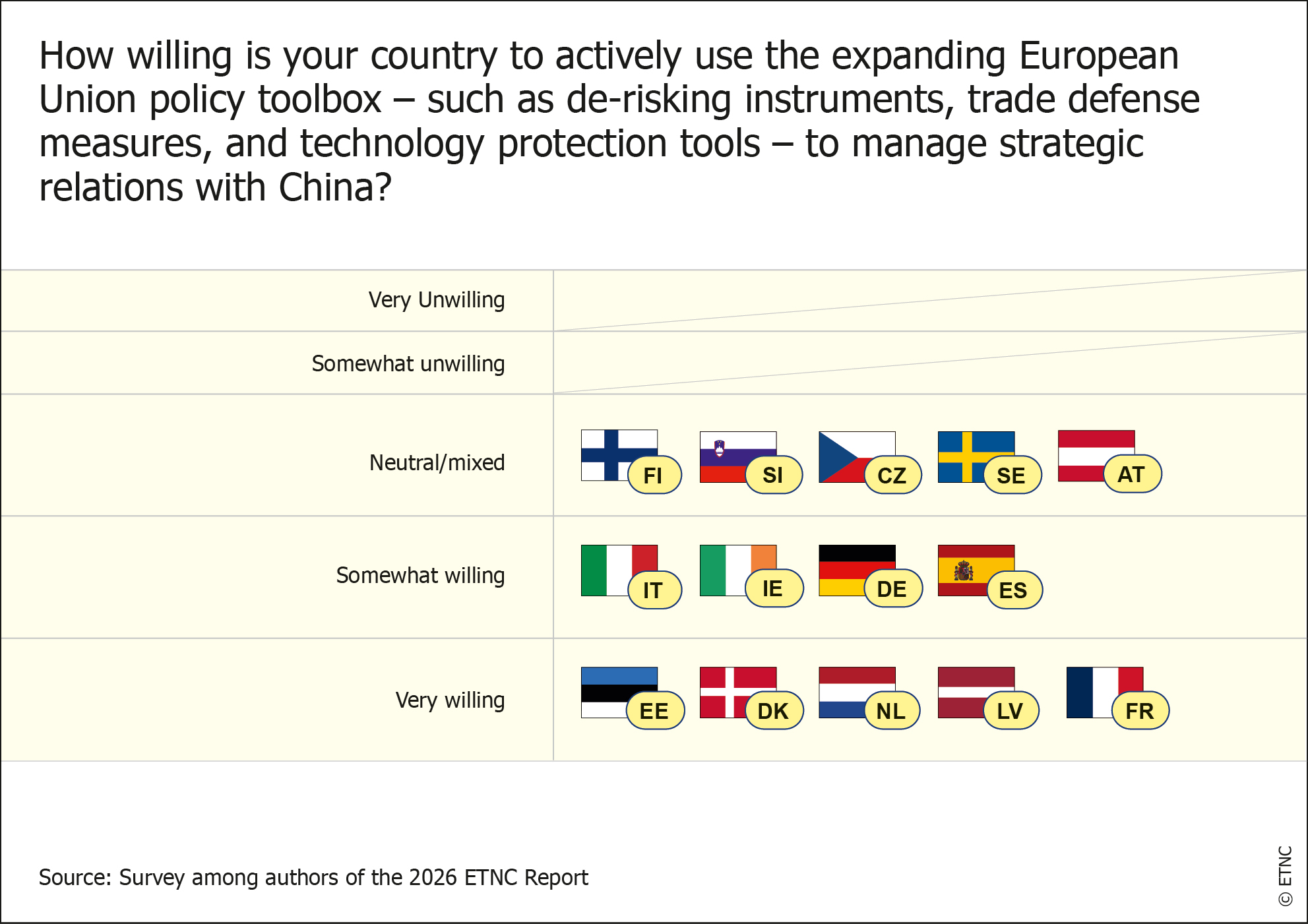

In recent years, the EU’s approach to China in science and technology has shifted from unconditional openness to a logic of ‘de-risking’ and economic as well as research security. The Economic Security Strategy published by the Commission in 20232 reflects the shared risk perception. The EU remains determined to reduce dependencies on China, in particular in strategically relevant sectors or critical infrastructures. However, when it comes to the details of implementation, alignment among EU capitals is still lacking and, in business, national actors continue to follow their own strategies of economic engagement with China.

The same lack of alignment can be seen in the research sector, where universities and institutions of higher education across Europe are actively collaborating with Chinese partners across disciplines, especially in the STEM fields. The EU is taking an increasingly cautious stance: while in the past Chinese partners participated (via their own funding) in Horizon research projects, the next funding cycle (2026-27) effectively excludes Chinese legal entities from participation in some key areas.3

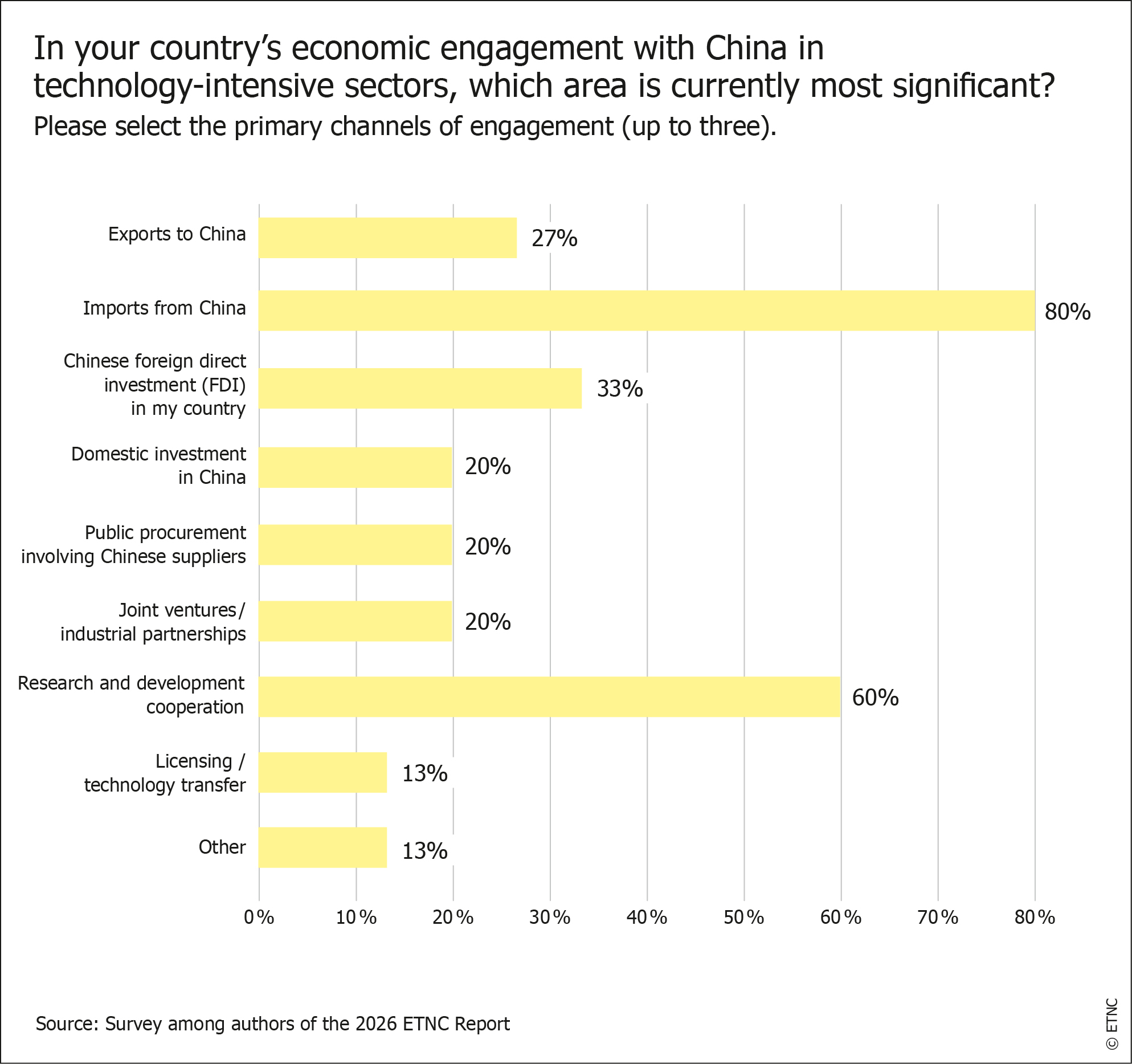

A challenge for implementing the economic and research security4 agendas lies in the fact that China is increasingly a supplier of technology to Europe. The dynamics in the semi-conductor and automotive sectors capture a dilemma: European businesses remain drawn to China’s innovation ecosystem and market, even though Beijing’s self-reliance campaign that is fueling localization in China is also increasing dependencies and driving de-industrialization in Europe.

On the policy side, increasing competition and fears of European dependency in high-tech sectors have contributed to the diplomatic tensions in recent years. In Brussels, risks stemming from the EU’s collective reliance on China as a technology supplier are considered a top priority on the de-risking agenda. EU policies trying to navigate these challenges and regulation such as the updated EU Cybersecurity Act, the Industrial Accelerator Act, the Critical Raw Materials Act etc., albeit country-agnostic in essence, regularly elicit criticism in China.

In recent years, however, both sides have also made efforts to diffuse tensions. The 2025 EU-China summit held on the 50th anniversary of mutual relations, both sides issued a joint statement on climate change. The fight against climate change and for the protection of the environment is, on the political level, still seen as a positive agenda for China and the EU.

Moving forward, in an increasingly complex geopolitical situation, the EU will face difficulties in translating its de-risking strategy into action, including achieving greater technological autonomy and reducing dependencies on China.

The risks stemming from deep technological interdependence with China are arguably recognized and taken seriously by most EU governments. Brussels seems to be preparing for a more hardline de-risking approach towards China, referring to the current state of affairs as “not sustainable.”5 But the policies of the current US administration are making it costlier for Europe to reduce its strategic vulnerabilities and implement high-stakes policies at both EU and member states’ levels.

European states face similar issues with Chinese tech power, but pursue different approaches

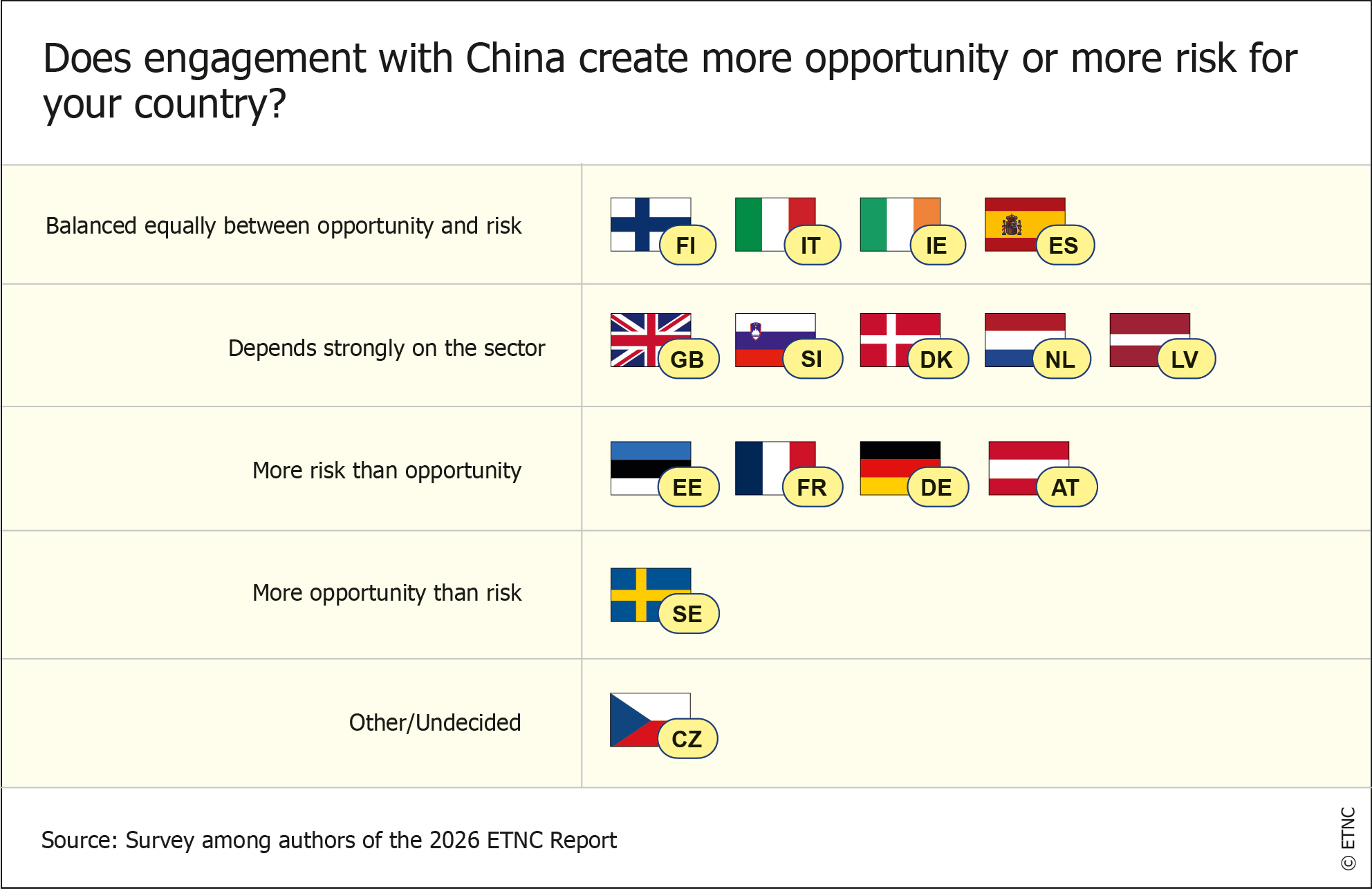

As the analyses in this report show, engagement with China as a rising technological power differs in these 21 EU member states and the United Kingdom, but each of these countries is exposed one way or the other.

For some of the countries analysed in this report, exposure to Chinese tech is focused on consumer products; for others, it is an integral part of industrial value chains or infrastructure. There are significant differences in public debates regarding the risks associated with dealing with China as a technological power – from virtually no discussions to lively debates about the delicate balance between nuanced collaboration and targeted de-risking on tech- and innovation.

The degree of exposure and engagement with China in tech and innovation often coincides with a country’s economic exposure to China writ large. France, Germany, Italy and the United Kingdom can be counted among the countries that are most affected by China’s rise in tech and innovation sectors.

For France, ensuring national and European sovereignty and competitiveness is now structuring relations with China in the technology and innovation space. While China’s capacity for technological innovation has become undeniable, the perception of risk in France is increasingly palpable. Paris is looking to boost European competence in fields that touch on sovereignty and security, such as AI or quantum applications, digital infrastructure or strategic supply chains. This limits the scope of engagement with China (as well as with the United States).

Germany’s economy is faced with an existential crisis due to increasing competition from China in key industries like automotive, machinery, and pharma. The science community continues to debate the “risks of not engaging” to the detriment of security circles, who urge for a more conservative approach to prevent unwanted tech transfer. The government’s efforts to strengthen German competitiveness are only taking off slowly; efforts for risk mitigation in both business and science are often met with resistance, because the relevant actors consider not collaborating with China a risk in itself.

In Italy, autonomous driving technology is arguably the most consequential dossier in tech and innovation relations, with Chinese state-owned enterprise SinoChem being a relative majority shareholder at tire manufacturer Pirelli. On the domestic market, Italian companies in the biopharma sector are facing encroachment by surging Chinese competitors. The country is increasingly preoccupied with the question of how continued collaboration with Chinese partners could negatively affect an already declining global share in high-tech manufacturing.

The United Kingdom and China have a long-standing collaborative relationship in science, technology and innovation. However, bilateral research and technology ties have become increasingly securitised over recent years, and the object of domestic political pressure on the UK government. As a result, future collaboration is likely to be more constrained than in an earlier phase of bilateral relations.

Austria, Belgium, Denmark, Finland, the Netherlands, Poland and Sweden can also be counted among the countries with a comparatively high degree of exposure to and engagement with China as a tech power. Their approaches to risk mitigation, however, differ considerably:

Austria’s science and technology engagement with China is characterized by quiet and steady continuity. Positioning itself as a small neutral actor, Austria has thus far avoided both enthusiastic embrace as well as dramatic rupture, seeking balance between geopolitical pressures under the umbrella of EU-level frameworks. Austria’s industrial policy roadmap until 2035, without mentioning China explicitly, places a strong emphasis on boosting technological sovereignty, economic resilience and the protection of critical infrastructure.

Belgium’s technology relationship with China is shaped by its structural strengths in innovation, institutional and regional fragmentation, and geopolitical dynamics putting its growth model increasingly under pressure. The country hosts significant innovation assets, notably in semiconductors, pharmaceuticals, and advanced manufacturing. Flanders dominates Belgium’s trade and investment relationship with China but has also applied tighter guardrails on investments and research collaboration.

In Denmark, Chinese firms now supply much of its electric bus fleet, Chinese batteries are entering the power grid, and cooperation is expanding in areas such as green maritime technology and water management. Although the China challenge has recently figured less prominently in public debates, concerns about Chinese technology remain deeply institutionalized. Since 2018, Copenhagen has embraced the EU’s de-risking approach, tightened research guidelines, and restricted the use of Chinese-made 5G, drones and surveillance technology.

China’s clout in tech and innovation is seen in an increasingly critical light both in business and among citizens in Finland, also due to Beijing’s pro-Russian stance in the Ukraine war. In policy and expert circles, views began turning more critical around 2018, similar to many other European countries. In the 5G debate, the country has performed a U turn: while in the past, all major Finnish telecom operators had relied on Chinese equipment, it was reported in October 2025 that Finland will exclude ‘high-risk vendors’ (e.g., Huawei) from its 5G networks on security grounds.

Technology also plays a crucial role in Sino-Dutch relations. The Netherlands has a strong high-tech industry that is entangled with and dependent on Chinese players, which the conflict involving formerly Chinese-owned chipmaker Nexperia showed. Simultaneously, China is still reliant on critical technology and expertise from Dutch universities and companies like chip machine manufacturer ASML. This gives the Netherlands leverage in the relationship with China - but also makes it vulnerable to the US-China technological competition.

When it comes to Poland-China cooperation, four technology topics have recently been discussed: 5G, lithium-ion batteries, automotive and e-commerce. Rising awareness of China as a tech power led to the adoption of mitigation measures. Poland is open to Chinese high-tech investments, including EVs, but only on the condition of technology transfer and based on not simply becoming an assembly site for Chinese products.

In Sweden, Chinese-owned companies’ R&D investments have increased by almost 300 percent since 2013. At the same time, China’s dominance in several technology areas has become a controversial issue, at least since the mid-2010s. Security aspects have shaped policy adjustments in the past five years, for example in foreign direct investment screening and public procurement legislation.

Hungary, Ireland, Portugal, Slovakia and Spain are among the countries that prioritize cooperation.

In Hungary, China is positioned as both an economic partner and a potential source of technological integration, while risk discourse remains limited. Key sectors include electric mobility, battery production, advanced ICT, and applied research, though the effectiveness of agreements is constrained by regulatory gaps and Chinese restrictions on technology transfer. Changes to that position might lie ahead following the change of government after the 2026 elections.

Pharmaceuticals, drugs and investments in R&D in China are at the core of Ireland’s engagement with China in science, technology and innovation. Ireland’s policy towards China in this realm constitutes a balancing act: Ireland’s open and FDI-driven economic model, traditionally strong ties to the US, and government strategies focused on security, competitiveness and a deeper integration within the EU single market.

Similarly, Portugal’s engagement with China as a technological and innovation power is grounded in a mix of collaborative openness, economic pragmatism, and caution amidst intense geopolitical competition and rivalry. In this context, an incremental growth of Portugal-China collaborative projects and initiatives in strategically relevant technological fields is visible in domains like e-batteries, energy and ICT infrastructure.

Slovakia’s relations with China in the domain of technology and innovation have been characterized over the past five years by pendulum-swinging positions driven by differing political ideologies among governing parties. Contrary to the previous government, the coalition led by Prime Minister Robert Fico pursues cordial relations with China across all domains of interaction. Cooperation on green technologies and renewables is framed as a means towards “enhancing energy security,” while reliance on Russian fossil fuels and partnership with the US in nuclear energy persist in parallel.

Spain approaches the challenge pragmatically: it still sees Chinese investment and technological cooperation as tools for industrial upgrading and the green transition, even as concerns about resilience, security and asymmetry grow. “Selective engagement” is the order of the day for Spain: limiting risk in sensitive areas such as 5G core networks, relying heavily on Chinese capabilities in photovoltaics and storage, and trying to embed Chinese investment in EVs and batteries within broader industrial goals.

For some of the countries analysed in this report, engagement with China on tech and innovation is not non-existent, but more limited. Among them are, for different reasons, Czechia, Estonia, Latvia, Lithuania, Romania and Slovenia – each of them with their own approaches to risk mitigation.

In Czechia, Chinese investments in the Czech technology sector remain relatively small and have been constrained by security considerations and investment screening mechanisms. However, there is a distinction between discourse and practice, as investments in Chinese 5G and solar panel technologies continue despite warnings from security agencies. The Czech industry strongly relies on Chinese imports, while Chinese consumer electronics, surveillance cameras, and selected industrial technologies are widely used.

Estonia’s engagement with China is best characterized by a divergence in the recommendations made by the national security apparatus, and decisions made by the business community. In 2019, Estonia signed the 5G memorandum with the US. China’s support for Russia in its war against Ukraine likely caused the exit of the 16+1 format and BRI. Yet there has not been a full decoupling: Huawei photovoltaic inverters remain embedded in Estonia’s energy infrastructure, and Estonia’s Bolt has announced a partnership with China’s Pony.ai in self-driving technology.

China’s investment in Latvia has largely been unsuccessful. Amidst the US-China rivalry and evolving EU policy on technological security, Latvia has opted to engage with China via EU frameworks rather than China led-initiatives.

Lithuania’s position on China as a technological power has shifted from openness, in particular in fintech collaboration, to one of the most alarmist in Europe. Four technology sectors – telecommunications, surveillance tech, photonics, and greentech – have become targets of either Lithuanian securitisation or Chinese retaliatory economic coercion.

The technological paths of Romania and China also rarely intersect. Even though many Memorandas of Understanding have been signed, no real tech output has resulted from them. Nor is there any debate about potential risks of China as a tech actor. Chinese surveillance technology – CCTV cameras – were adopted in Romanian public institutions without any larger debate.

Slovenia increasingly considers China an attractive partner in technology, primarily with the goal to create additional options and reduce dependence on a slowing European industrial base. With one of Europe’s highest manufacturing shares of GDP and among the global top 10 in robot density, there is high interest in engaging with China on technological enhancement and market access. Yet, Slovenia sees itself anchored in the EU, which sets clear limits on this engagement.

To deal with China’s technological rise, European coordination is indispensable, but will be challenging for economies under pressure

Moving forward, Europe will have to face the fact that China will remain a force to be reckoned with in high tech and innovation. Securing Europe’s still strong industrial base and investing in research and development will be crucial to remain competitive in high-tech and emerging sectors.

To adapt to the growing competition from Chinese high-tech, Europe will need to closely monitor the implementation of sectoral Five-Year Plans and respond accordingly. As China’s leadership continues to project confidence in its policy of tech self-reliance, there can be no doubt that the challenge to Europe’s technological competitiveness will only intensify in the coming years.

The outlook for the EU and its member states is complex, as they find themselves between a rock and a hard place: Distrust in Chinese technology will stay, but with the transatlantic relationship challenged by Washington’s shifting policies, the implementation of policies protecting European assets might prove challenging. In addition, the ongoing crisis of the transatlantic relationship might undermine the EU’s ability to act in global technology competition, making the reduction of strategic vulnerabilities costlier for Europe.

As the Managing Director of the Asia-Pacific Department at the European External Action Service (EEAS), Erik Kurzweil, stressed in his speech at a conference in Beijing on EU-China relations in May 2026, both sides are faced with important choices that will “determine whether our two great regions drift apart or move forward together.” Kurzweil tried to strike a more conciliatory tone despite the many points of contention: “The inflection point in our relationship is not a moment of crisis, but of opportunity. The EU is ready to engage—with openness, with pragmatism. But engagement must be reciprocal and it must deliver tangible benefits for our people, our economies, and our planet.”

However, with regards to China’s rise as a technological and science superpower, the EU, its member states and European neighbors will have no choice but to keep addressing both risks and opportunities – and to carefully weigh them against one another based on sound – and swift – analysis.

- Endnotes

1 | MERICS. China’s National People’s Congress 2025. 13 March 2025. https://merics.org/en/merics-briefs/chinas-national-peoples-congress-2025

2 | Council of the European Union. European economic security. Last review 11 December 2025. https://www.consilium.europa.eu/en/policies/european-economic-security/ and

Europäische Kommission. Gemeinsame Mitteilung an das europäische Parlament, den europäischen Rat und den Rat über eine „europäische Strategie für wirtschaftliche Sicherheit“. 20 June 2023. https://eur-lex.europa.eu/legal-content/DE/TXT/PDF/?uri=CELEX:52023JC00203 | G. Manca. The EU realpolitik turn in research cooperation with China. Central European Institute of Asian Studies (CEIAS). 26 November 2025. https://ceias.eu/the-eu-realpolitik-turn-in-research-cooperation-with-china/ and

European Commission. Joint communication to the European Parliament and the Council – Strengthening EU economic security. 3 December 2025. https://www.eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52025JC09774 | European Commission. EU strengthens science diplomacy and research security to support global research cooperation. 27 February 2026. https://research-and-innovation.ec.europa.eu/news/all-research-and-innovation-news/eu-strengthens-science-diplomacy-and-research-security-support-global-research-cooperation-2026-02-27_en

5 | E. Kiorri, E. Heinz. Can the EU de-risk from China and make its trade relationship sustainable? Euronews. 6 February 2026. https://www.euronews.com/my-europe/2026/06/02/the-eu-says-its-trade-with-china-isnt-sustainable-what-does-de-risking-mean

Content