picture alliance / CFOTO

Content

Report

The sky is the limit: China's rise as a transportation superpower challenges the EU

Key findings

- China is set on becoming a global "transportation powerhouse”: Its ambitious vision of being a global leader in advanced transportation industries such as rail, shipping and commercial aerospace presents Europe’s manufacturing sector with a significant challenge.

- China is already a global front-runner in rail, high-speed rail and shipbuilding: In the rail, high-speed rail (HSR) and shipbuilding sectors, China has largely pushed European producers out of its domestic market following a period of technology transfer and import substitution. Since then, Chinese firms have secured a substantial share of the global market and are challenging European producers in third markets.

- China wants to repeat its success in high-speed rail in the commercial aerospace sector: China is now attempting to replicate its HSR successes in commercial aerospace, which is Europe’s last and most crucial bastion of technological superiority in advanced transportation equipment. The successful maiden flight of China's C919 single-aisle jet in 2023 shows China’s progress.

- Problems with copying the high-speed rail playbook: China has encountered major hurdles when applying the same industrial policy model it used for HSR to commercial aerospace. These obstacles arise from market dynamics, technological limitations, and political considerations.

- European companies have a temporary breathing space: European companies continue to play a pivotal role in China's commercial aerospace projects, which earn them substantial profits. Nevertheless, they must remain vigilant, as Beijing's ultimate objective is to supplant them and compete with them globally.

1. China’s rise as a global transportation power squeezes Europe

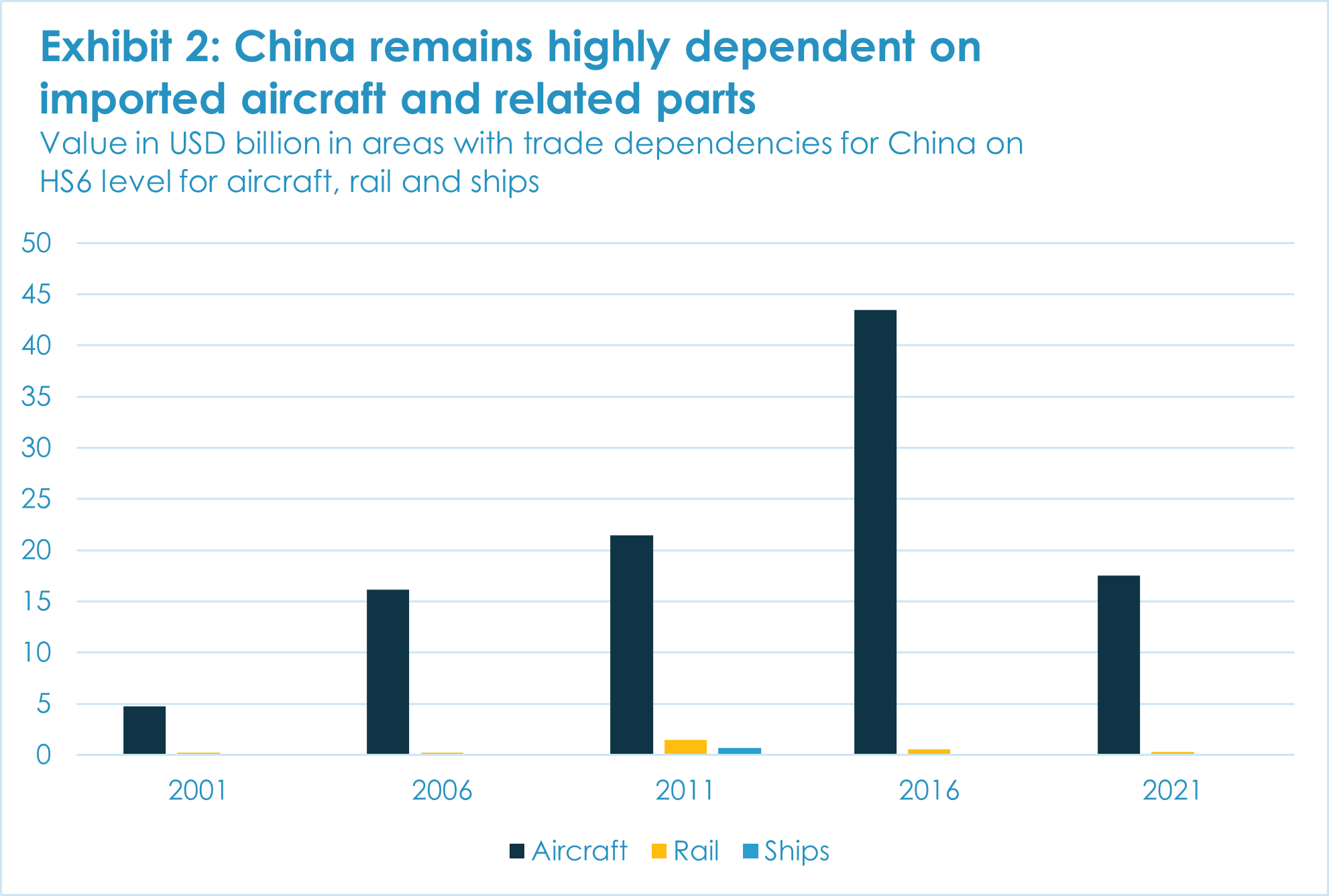

Beijing’s desire for China to become a global “transportation superpower” in railways, shipping and aviation presents the EU’s manufacturing sector with a critical challenge. China has long relied on significant transportation equipment imports from the EU, averaging 18.7 percent of its total imports between 2016-2022. Most of this was vehicles and parts, while imports of aircraft, trains, and ships (including components) accounted for 3.8 percent of total imports. But Chinese players are now moving up the value chain in those sectors, posing a major challenge for European manufacturing. There are implications for European companies in the Chinese market and in third markets too.

China’s goal to move up advanced transportation equipment value chains is aided by its comprehensive industrial policies and targeted strategic support measures. The automotive sector is undergoing massive shifts as Chinese companies expand their market position. They already dominate domestic EV sales and are beginning to make inroads into global markets. A rapid rise in exports meant Chinese-made vehicles surpassed Germany’s vehicle exports in 2022. China is on track to surpass Japan as the world’s largest vehicle exporter in 2023.1

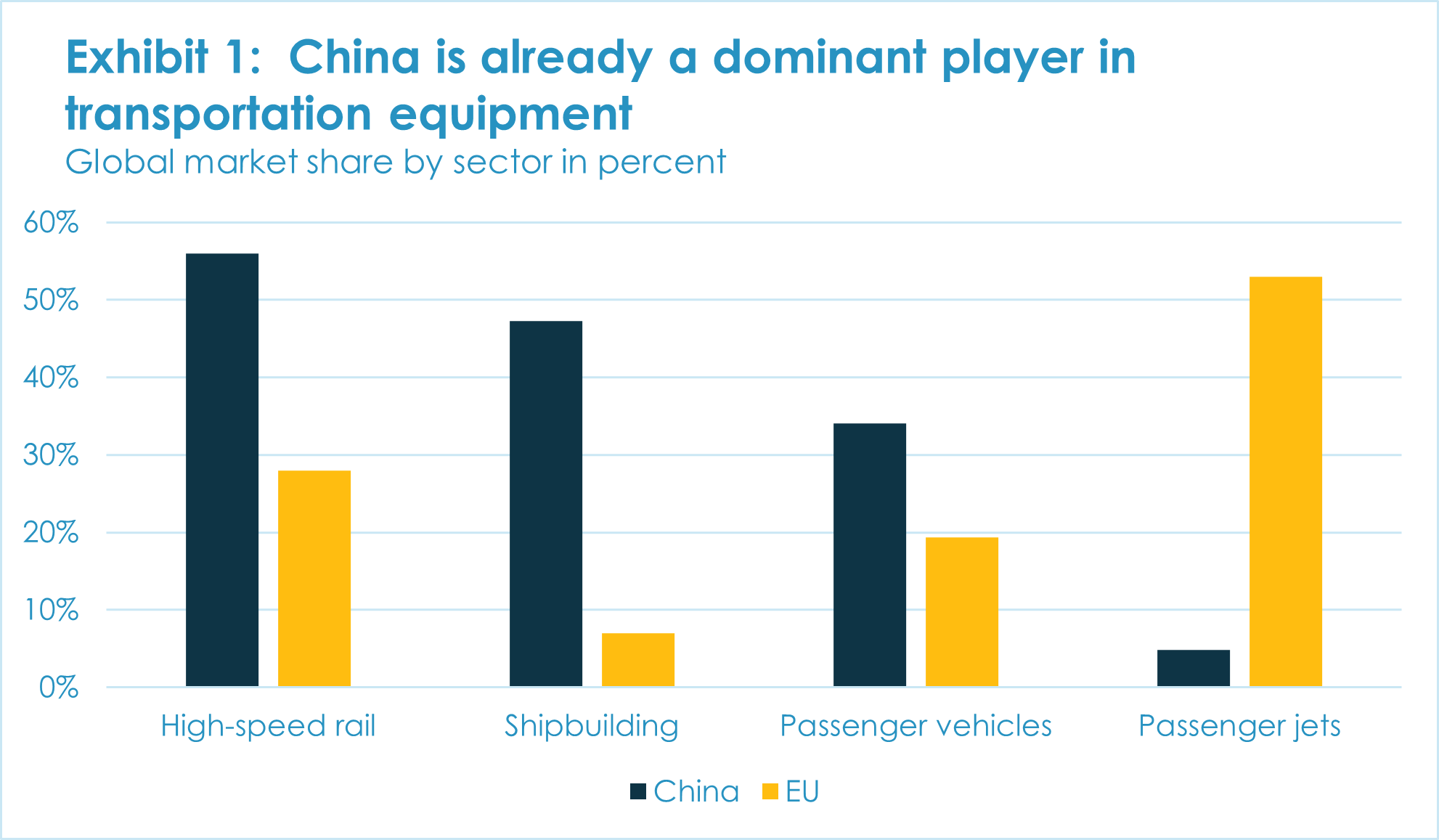

China is already the world’s largest shipbuilder, producing 47.3 percent of global gross tonnage in 2022. Six of the world’s top 10 shipbuilders are Chinese.2 A similar dominance is apparent in rail: the output of China Railway Rolling Stock Corporation (CRRC) dwarfs that of other Asian and European HSR producers. CRRC held 56 percent of global market share in 2022, while French firm Alstom was a distant second, with 15 percent of the global market.3

Chinese policymakers aspire to see domestic firms break into the world’s most complex industries, which are still predominantly led by foreign firms. To this end, they are applying the same policy mix used in HSR to other sectors, notably commercial aerospace – the last remaining transportation sector where China still lags.

If successful, the strategy could have a significant impact on Europe’s manufacturing base and competitiveness. Chinese imports from EU-based aerospace suppliers would decrease, and its producers would begin to challenge European producers in third markets. Today, China’s aggregate import dependence in transportation industries is already limited to commercial aerospace. In other sectors, China has absorbed large parts of the value chain (see exhibit 2), thereby eroding the position of European companies.

Section 2 provides a short overview of the industrial policy context for China’s transportation superpower ambitions. Section 3 and 4 recapitulate the “industrial policy playbook” China has deployed for HSR and how it applies in the aviation sector. Section 5 identified the barriers to China achieving similar successes in aviation as in HSR.

Despite their differing technological and market features, a better understanding of China’s strategies in rail and aviation offers lessons in how Beijing approaches building its position in advanced transportation equipment manufacture, and the likely impact on European players.

2. China wants to be a transportation superpower by 2035

Beijing has made it a key policy priority to strengthen China’s grip on manufacturing by moving up industrial value chains, thereby elevating Chinese multinationals globally.5 Under President Xi Jinping, achieving full control over strategic value chains, rather than merely moving up them, has grown in importance and is an integral part of China’s industrial policies.6 In 2016, the government introduced guidelines on supporting companies to strengthen their position in global value chains and enhance their innovation capabilities.7

The playbook to hit these goals has been embedded in key industrial policies since 2013, most notably the "Made in China 2025" strategy (MIC25). The manufacture of transportation equipment has a central role to play: advanced rail equipment, high-tech ships and aviation equipment all featured in the MIC25 strategy and accompanying policy documents.

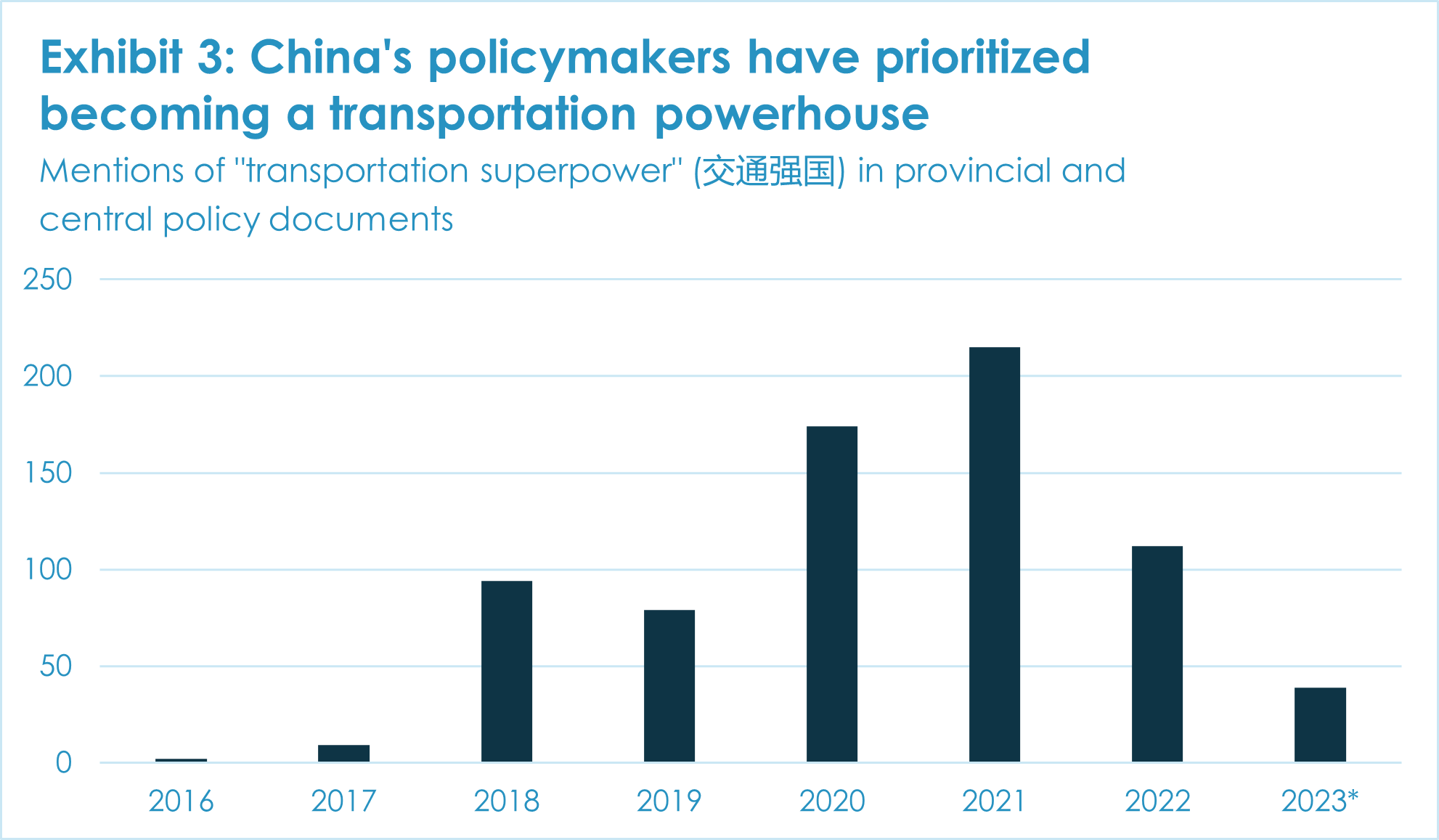

The ‘transportation superpower’ concept (交通强国) first emerged in 2016 and appeared over 700 times in key policy documents by September 2023 (see exhibit 3).8 The “Outline for Building a Powerful Transportation Country” (交通强国建设纲要) issued by the party’s Central Committee and the State Council in September 2016 unleashed a wave of policy documents using the term, signaling greater support for advanced transportation equipment. Mentions of transportation superpower peaked in 2021, indicating the focus had shifted from agenda-setting towards implementation. The flurry of policymaking meant state-owned enterprises (SOE) and private actors benefited from preferential policies and easier access to finance.

The policies emphasize building world class transportation infrastructure and enhancing China’s ability to manufacture advanced transportation systems by 2035. Beijing’s industrial planners have set ambitious targets for railway and shipbuilding and more modest ones in aviation.

Specifically, the targets include:

- Railway equipment: Achieve major breakthroughs in 30,000-ton-class heavy-duty trains and 250-km/h-class high-speed wheeled freight trains.

- Shipbuilding: Strengthen independent design and construction capabilities for large and medium-sized cruise ships, large liquefied natural gas ships, polar navigation ships, intelligent ships and new energy ships.

- Commercial aerospace: Improve the spectrum of civil aircraft products, and make significant progress in large civil aircraft, heavy helicopters, and general aviation vehicles.

China has made remarkable progress towards these goals: In July 2023, the CR450, CRRC’s debuted its next generation HSR capable of speeds over 450 km/h. Other efforts are pushing technological boundaries by experimenting with ultra-high-speed maglev trains (up to 1000 km/h). Rail is China’s most advanced transportation system by far, but new achievements in aerospace and ship building were also noticeable in 2023. Commercial Aircraft Corporation of China (COMAC) put the C919 into regular passenger service in May with China Eastern, while China State Shipbuilding Corporation (CSSC) completed sea trials for the first domestically built cruise ship, the Adora Magic City.

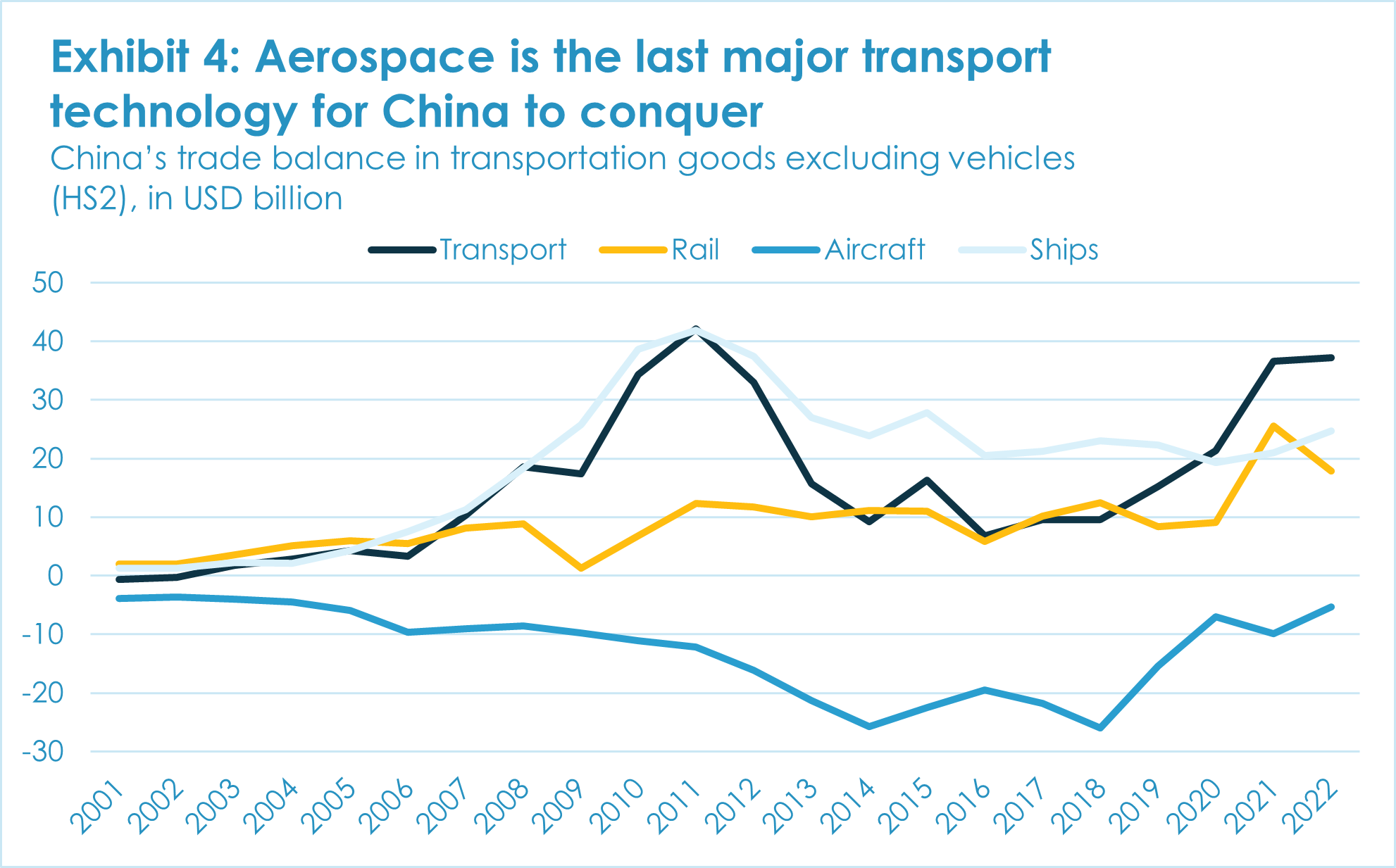

China’s increased competitiveness in transportation is also reflected in its trade balance. Surpluses have been rising for rail and ships.9 Aerospace is the only sector with a persistent trade deficit. The trade deficit fell to USD 5.4 billion in 2022, from the 2018 peak of USD 26 billion but the drop was mainly due to the collapse in new aircraft deliveries.

These successes cannot hide China’s heavy reliance on foreign suppliers and partners; access to foreign technology remains vital. The C919 and Adora Magic City are emblematic of this dependence, as critical technologies and expertise from international companies played crucial roles.10

Key policy documents state that China aims to replace foreign producers in these fields gradually. In April 2023, the Ministry of Transport, for instance, released an action plan for better transportation capabilities that included core technology chokepoints.11 Section 5 outlined how policy adjustments to deal with specific dependencies and technological chokepoints will run alongside China’s usual industrial policy playbook.

3. High-speed rail shows China’s playbook for strategic value chain control

State-owned enterprises (SOEs) are central to Beijing’s ambitions to control strategic value chains in advanced (equipment) manufacturing as their dominance and vertical integration provides direct control and they can readily align with national strategic priorities.

China’s rapid accent in rail demonstrates the power of this vertical integration. Critical inputs such as steel, rail infrastructure construction, rolling stock manufacturing and railway services operations were in the hands of SOEs. State-run firms were the primary suppliers and consumers in the rail sector, facilitating a seamless transfer of state guidance and support. SOEs also have ample access to funding within China’s state financial system, advantaging them over private enterprises. This matters in capital intensive sectors such as rail – and is not unique to China.

China’s HSR development used the following playbook, premised on vertical integration:

- Create market demand through state support: China's success hinged on the strategic creation of demand and capitalized on its huge market. Advances in rail took off with the massive infrastructure stimulus unleashed in the global financial crisis in 2008/9, which tripled rail infrastructure investment to CNY 749 billion by 2010. This synergistic approach catalyzed economic growth and cemented China’s appeal as a center for international partnerships and technology transfer. This was especially true for the relatively niche HSR sector.

- Build up domestic industry with the aid of foreign companies: Foreign companies were welcomed to participate in market developments and fill the technological gap. Alstom, Bombardier, Siemens, and Kawasaki Heavy Industries were required to transfer technologies to Chinese partners via joint venture (JV) agreements. Mutually beneficial partnerships allowed international firms access to a vast market, while China accelerated its path to technological leadership. To access foreign technology, Beijing also encouraged overseas M&A and licensing agreements.

- Strengthen innovation system to develop indigenous technology: The Ministry of Railways coordinated with two firms, CSR and CNR (which later merged), to boost indigenous innovation. Industrial policy support went to promote science and technology research projects involving universities, research institutions and national laboratories. The results are visible in CRRC’s patent registrations, up from 88 patents in 2006 to 1800 in 2019.12

- Crowd out foreign companies in China: Chinese companies absorbed, integrated and finally replaced foreign technology. Foreign partners helped develop the first HSR trains but by 2010 China had introduced an indigenous one, the CRH380. Although still reliant on foreign patents and standards, these used Chinese designs. By 2017, when the CR400A was introduced, access to foreign technology was less relevant. Market opportunities for foreign companies faded as Chinese reliance on them evaporated. Highly enduring bearing steel is among the few exceptions as it requires imported screws from Japan.13

- Push into global markets: With dominance in the domestic market and substantial manufacturing capacity for rail systems, China’s firms are set on international expansion. Rail networks are a substantial part of the Belt and Road Initiative (BRI), securing large rail project deals in Africa (e.g., in Ethiopia and Kenya) and HSR systems in Indonesia and Thailand.

The rail equipment sector illustrates the ambitions and capabilities of China’s strategic industrial policy, whose impact is already felt globally in solar and EVs. China has shown it can scale up technological and manufacturing capabilities to become a leading – even dominant - global actor. Rapid progress in rail technology and ship building raises the question of whether China can do the same in aerospace.

4. How the HSR playbook works in commercial aerospace

Chinese policymakers are trying to emulate their success in HSR in other sectors, notably in commercial aviation. China’s latest Five-Year Plan for Civil Aviation states the industry “is vital to […] support industrial development, promote regional coordination, safeguard national security and meet the needs of the international community”.

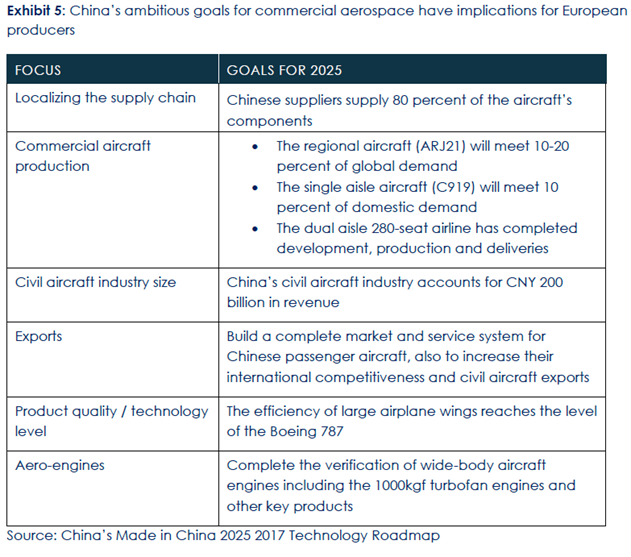

In 2017, Chinese planners outlined ambitious goals (see exhibit 5) in China’s “Made in China 2025” strategy. With two years to go, most remain out of reach (e.g.,10 percent of domestic demand met by the C919) but they paint a clear picture of China’s ambition in the commercial aircraft sector.

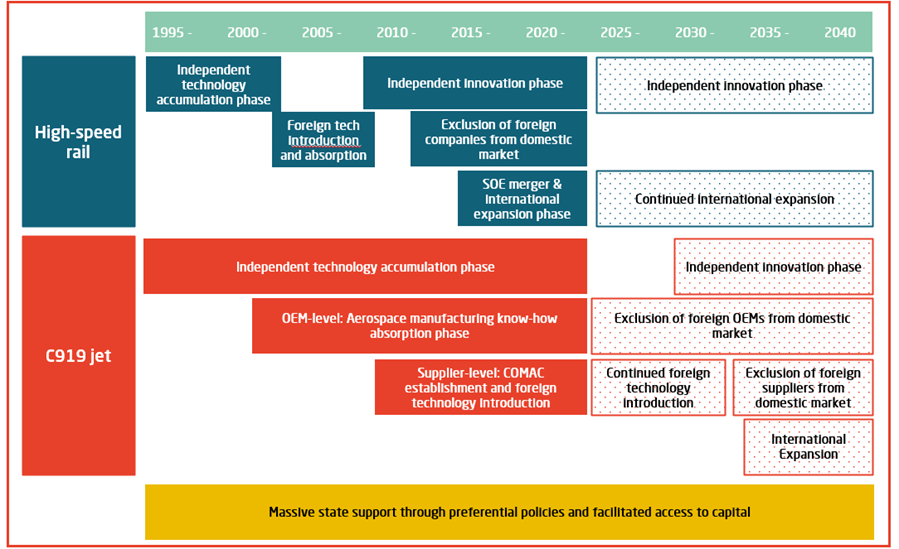

Looking at China’s single aisle aircraft project – the C919 – it is apparent how closely it follows China’s HSR playbook (see exhibit 6). Building blocks include SOEs as central actors, the government as main consumer and the key role of foreign companies in technology transfer. These similarities would suggest that China has a high chance of replicating its success story in this industry too.

1) Leveraging the state to make the C919 project a success

As in the HSR sector, China’s government is betting heavily on state intervention to strengthen supply and create demand for its commercial aircraft industry:

In 2008, China’s government established COMAC as an independent company by separating Shanghai subsidiaries from the Aviation Industry Corporation of China (AVIC) and transferring the intellectual property for China’s regional jet, the ARJ-21. AVIC remains a key player for China’s aerospace sector, both as China’s military aircraft manufacturer and as a supplier to COMAC.

During COMAC’s restructuring, the company welcomed five additional state-owned investors: the SOE-watchdog SASAC, Shanghai Guosheng Group, Aluminum Corporation of China, China Baowu Steel Group, and Sinochem. In late 2018, a new round of state-owned shareholders joined the company. To bolster COMAC's financial resources, the government continually injects new financing by introducing new shareholders.

Research suggests COMAC benefitted from total government support worth USD 72 billion in financing through 2020.14 This excludes hard-to-measure types of support like R&D subsidies, free or below-market land, energy, raw material or labor inputs, tax benefits and of course the revenue from ARJ21 and initial C919 sales to state owned airlines which might have purchased Western aircraft if state guidance were absent (see below).15

The supply side measures were complemented by creating demand. As in HSR, the government has an outsized role in commercial aerospace procurement. China’s three biggest airlines, with a combined market share of 68 percent, are all state-owned. China Eastern was the C919’s early adopter. Crucially, the Civil Aviation Administration of China (CAAC) has the ultimate say about airline’s purchase. In 2017 a high-ranking official indicated CAAC encourages the purchase of China-made aircraft.16

2) Building up China’s C919 supply chain with help from foreign companies

China heavily relies on cooperation with foreign companies to facilitate technology transfers in commercial aerospace. Fourteen major JVs17 have been established between European and US suppliers and two SOEs, AVIC and the China Electronics Technology Group Corporation (CETC).18 While most of the C919’s body parts come from Chinese producers, the role of the JVs, (mostly formed between 2011 and 2014) is to supply technologically complex and high value-added components like landing gear or avionics. For now, engines are imported from a Franco-US JV between Safran and GE. The C919’s localization rate is currently about 60 percent.19

China has benefitted in other ways from foreign expertise in aircraft assembly. Notably, the McDonnell Douglas Corporation collaborated in 1985 to jointly produce the MD-82 in China. Airbus has had a final assembly center in China since 2008 to produce the A320, and added another in 2017, making the A330. Airbus announced plans in 2023 to increase A320 production capacity.20 Boeing set up a JV in 2017 to oversee assembly of the 737 in China. The plants provide China with valuable insights on integrating components and scaling up production. They also increase China’s manufacturing value added in the sector.

3) Promoting independent commercial aerospace research and absorbing foreign technology

The C919 project also follows the China’s successful template for government-orchestrated research collaboration between aerospace firms, research institutes, universities, and testing centers. The system promotes pooling of resources, knowledge, and expertise to surmount technical barriers and, ultimately, to build a plane with Chinese intellectual property.

The innovation system established to build the C919 embraces 36 universities. COMAC has forged strategic cooperation agreements with ten of them, steering their collective research efforts toward civil aviation technologies. China’s labs and engineering centers include the State Key Lab for Civil Aircraft Flight Simulation and the Advanced Structures and Materials Technology Laboratory for Civil Aircraft.21 Chinese universities have a dual role to play: they cultivate aerospace talent while supporting research.22

China is still some way off the level of success it has reached in HSR, though its indigenous innovation sector has had some early accomplishments. The General Iron and Steel Research Institute was founded in 2010 and partnered with steel-makers Baowu and Fushun to develop high-strength 300M steel for civil aviation landing gear, replacing previous US imports. Liebherr Aviation, the European COMAC supplier, now uses Baosteel’s 300M steel for C919 landing gear.23

4) Early stages: Replacing foreign suppliers with domestic ones

As well as 300M steel, China's pursuit of self-reliance pursuit in aerospace technology has had initial success lies in aircraft tires. This specialized domain is dominated by a few Western firms. C919 supplier Honeywell Boyun Aerosystems uses French Michelin's Air X tires. But Chinese-brand tires have proven viable on the ARJ21 jet, and they've been added to the C919's list of certified suppliers.

The strongest efforts to displace foreign entities center on engine development. The C919 uses the CFM engine, imported from the Safran-GE JV. The state-owned Aero Engine Corporation of China (AECC), formed by COMAC, AVIC, and Beijing municipal government, is developing a replacement engine – the CJ-1000A. Despite delays, AECC aims to commercialize the engine by 2030. Success would augment China's value addition in commercial aerospace and mitigate vulnerability to foreign sanctions.

The engine project’s strategic significance was underlined when AECC was added to the US entity list in 2020. The Trump administration even contemplated restricting GE's export license for the CFM engine. However, AECC will continue to rely on importing engine components like high-pressure compressors from Germany's MTU and titanium alloy hollow fan blades from the UK's Morgan Advanced Materials Group.24

COMAC's remains dependent on foreign suppliers, yet there is a clear intention to position the C919 as an alternative to Airbus' A320 family and Boeing's 737s. Plans for self-reliance extend to the regional jet sector. China has not ordered new regional jetliners from foreign producers since ARJ21 deliveries began in late 2015. As a result, Embraer closed its 13-year old JV plant in Harbin in 2016.

5) China looks to global markets

China’s smaller, regional aircraft – the ARJ-21 – has been successfully exported to Indonesia’s TransNura. China-made Airbus planes have also been shipped to international clients, including a Philippine airline and Hungary’s Wizz Air.25

Currently, COMAC remains focused on pushing the C919 in China's domestic market, leveraging government influence to steer sales. So far, it remains in early stage domestic commercialization as COMAC has delivered only two units to China Eastern.

However, China's long-term ambition is to win global sales of the C919 and any future upgrades. Foreign firms that have expressed interest in buying it include international leasing firms AerCap (formerly GE Capital Aviation Services) and BOC Aviation. Although BOC Aviation is a foreign subsidiary, it is ultimately owned by the Bank of China. Neither has yet gone beyond letters of intent.

China acknowledges the critical importance of securing regulatory approvals from such bodies as the Federal Aviation Administration (FAA) or European Union Aviation Safety Agency (EASA). In 2017, China’s CAAC and the FAA signed a bilateral agreement to streamline certification processes, but the rigorous FAA certification remains a formidable challenge.26 Its complexity has led COMAC to rely heavily on established foreign suppliers in the hope their products and expertise will facilitate certification.

The latest Five-Year Plan for China's Civil Aviation sector underscores the goal of gaining overseas airworthiness certification for Chinese aircraft.27 The CAAC wants both to improve its own capability to certify airworthiness and to export Chinese airworthiness technical standards to Belt and Road Initiative countries.

5. Barriers to replicating HSR success in commercial aerospace

It is far from guaranteed that China can replicate its success with HSR in commercial aerospace. The industry differs substantially from the HSR sector, a fact that is creating substantial roadblocks to its industrial ambitions.

China lacks market power in mature commercial aerospace, unlike in HSR

China’s market was more appealing to foreign rail companies than to their aerospace counterparts. The rapid expansion of China’s HSR network presented a substantial market that was the only one of its kind. The vision of a 12,000 km HSR network by 2020 in the government's 2004 Medium- and Long-Term Railway Plan surpassed the combined length of all HSR tracks worldwide at the time (9230 km).28 This vision became reality. Since 2007, an astounding 84 percent of global HSR track has been added in China.

China’s commercial aerospace market looks vastly different as COMAC is entering a mature market with the C919. In 2022 Airbus’ A320 or Boeing’s 737 families received combined orders for 1082 aircraft compared to 971 in 2010. Furthermore, the Chinese market – while massive – is just one of several large markets. In 2010, Airbus estimated China’s single aisle jet deliveries would make up 15 percent of global deliveries by 2030. In 2022, Airbus, Boeing, and COMAC believe China-deliveries will make up 20 to 25 percent of global deliveries until the early 2040s.

In HSR, companies were more willing to transfer their technology into Chinese JVs. China was essentially the only sales market available to them so they had to adapt to local requirements. In aerospace, China is an important but not dominant market, so Airbus, Boeing and their suppliers have - in theory - more leverage. They can potentially get away with less tech transfer because the stakes are lower for them.

The Airbus-Boeing duopoly and dual-use nature of the aerospace sector may hinder tech transfer

The duopoly between Boeing and Airbus makes it harder for Beijing to pit foreign companies against each other, whereas the HSR market’s segmented structure gave Beijing leverage to acquire foreign intellectual property. HSR firms were competing with rivals who might comply if they did not. On the other hand, aerospace suppliers could be more vulnerable. But Boeing and Airbus will take their cues from each other on technology transfer.

Again, unlike the HSR sector, commercial aircraft involve many dual-use technologies that could be subject to export controls. Foreign companies looking to supply COMAC need to consider these challenges, which may hinder China's efforts to establish itself in the medium term. For example, the C919's CFM LEAP engine is sourced from a French-US JV that requires a US license. In early 2020, the Trump administration considered halting the supply of engines through this JV.29 Other critical technologies, like flight control systems, could also face export restrictions.

Commercial aircraft are more complex technologically than HSR

The technological difficulties inherent in aircraft building also set this sector apart from HSR. Admittedly, HSR trainsets posed engineering, production, and safety challenges, and China managed to transfer and disseminate the technology swiftly. In aerospace Airbus and Boeing primarily act as system integrators and heavily rely on third party suppliers – often from other G7 countries.

Critical components such as jet engines and parts, avionics and landing systems but also advances in aerospace materials and structures, rely on an international division of labor. It will be a monumental challenge for China to master all technologies as well as production processes and build an economically efficient plane. Due to these industry features, COMAC is cautious about shifting to domestic suppliers too early to avoid reputational damage as safety standards are far more stringent and the stakes higher for the commercial aircraft industry.

Geopolitical shifts hinder tech transfer

In the 2000s and early 2010s, China's progress in the HSR sector benefited from a more favorable geopolitical climate than today's tense situation between the United States and China. Economic development took place in more open global environment that fostered foreign investment in China and tech sharing with its industries. Rail companies assessing the appeal of China’s market and risks to technology did so in the absence of major geopolitical conflicts.

Heightened US-China rivalry has made foreign aerospace firms more cautious about sharing technology with China's aerospace sector. Lessons from the HSR sector's history have only added to their hesitancy. They fear risks to intellectual property in the competitive global aerospace arena. China's aerospace advances therefore face higher barriers to technology transfer and foreign collaborations.

Challenges lie ahead for C919’s production ramp up and exports

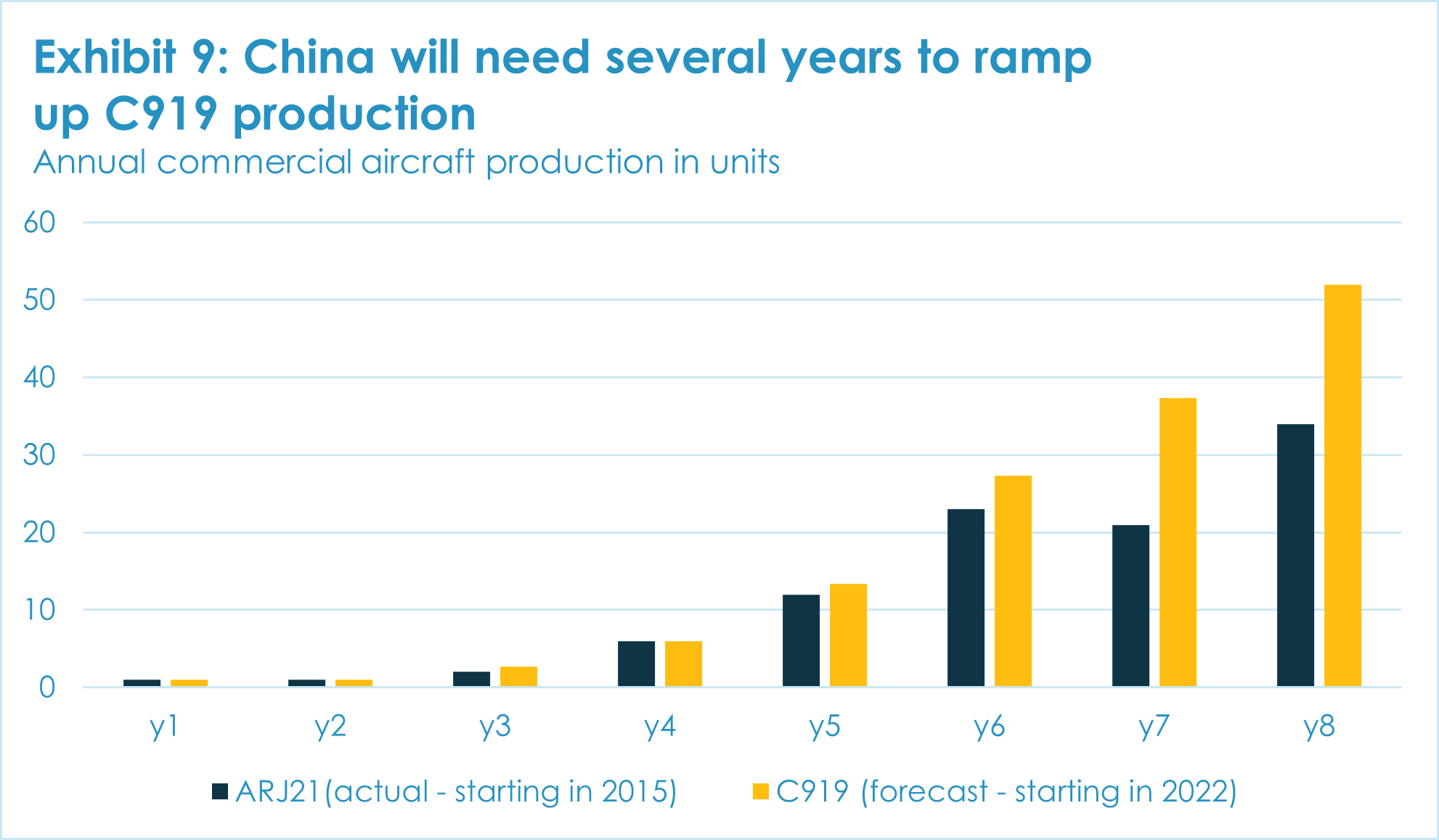

China aims to challenge European aerospace producers, yet COMAC will face challenges ramping up C919 production. Making a single-aisle jet is already challenging enough that few firms have been able to manufacture them at scale. COMAC targets annual output of 150 C919s by the late 2020s, but the history of the ARJ21 suggests problems. China will still rely on foreign aircraft makers, including Airbus, to serve its domestic market for some years.

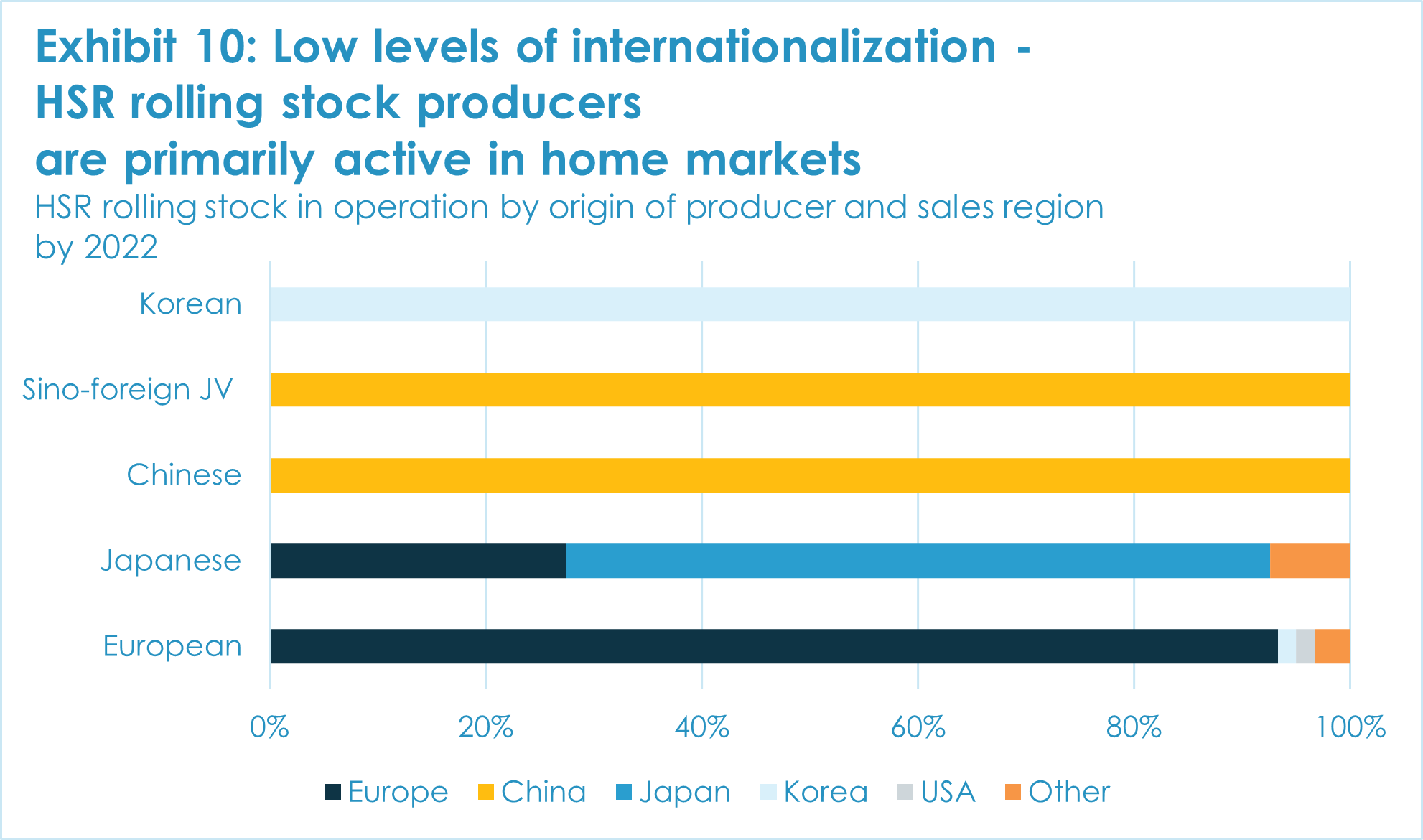

The hurdles to exporting the C919 and challenging Airbus and Boeing in third markets are even higher than in HSR, and even in HSR, China struggles with lackluster exports. In 2023, the first and only Chinese-made HSR train set so far exported went to Indonesia’s Jakarta-Bandung line. HSR manufacturers are primarily active in their home markets (see graphic). But China’s HSR exporters should gain advantages from the BRI and access to policy bank funding. However, other advanced economies, such as Germany, have recently started to use instruments like export guarantees to support their own HSR champions win overseas contracts. If HSR internationalization is proving problematic, breaking into global commercial aerospace markets will be even tougher.

In commercial aerospace, foreign airlines, used to Airbus and Boeing planes, are likely to resist the high switching costs of adopting the C919 which is not fundamentally better than the familiar options and lacks a proven safety record. China will need to flex its diplomatic muscle and offer substantial concessions to make the C919 an international success. But Beijing counts on influencing Chinese companies to order Chinese planes, even overseas. Indonesian carrier TransNusa – backed by Chinese SOE CALC - has ordered 30 ARJ21 regional jets. The first one was delivered in 2022. In September 2023, Tianju Group – a Shaanxi-based private enterprise with an ownership stake in Brunei-based GallopAir – announced the airline had ordered 15 ARJ21 and 15 C919 jets. Interest has also come from the Irish subsidiary of BOC Aviation, itself owned by Bank of China (see chapter 4).

These obstacles suggest China’s HSR playbook is only partially suited to the realities of the commercial aerospace industry. Still, Airbus and Boeing should remain vigilant. It is a key Chinese objective to establish a competitive domestic commercial aerospace sector and Airbus’ own rapid success provides a compelling model for Beijing. The European company took only 26 years to secure 50 percent global market share in 2000, after deploying its inaugural aircraft in 1974. China’s geopolitical situation is more intricate, yet robust government support for commercial aviation and a quickly shifting global landscape should not be underestimated.

6. The EU should brace itself for China’s commercial aerospace aspirations

While Europe’s transportation equipment manufacturing remains strong – especially in commercial aerospace - China's industrial ambitions pose a challenge for Europe’s industrial base. Over the past decades China has absorbed significant parts of global value chains. In 2022, China accounted for 30.5 percent of global manufacturing and was especially strong in consumer goods and electronics. In the future, Beijing wants to have the same unmatched competitiveness in advanced sectors.

The China-led global transformation of key transportation industries has had a differentiated impact on Europe so far:

- In railways, European rolling stock and railway companies remain globally competitive. But as part of China’s “going out” and BRI strategies, Chinese enterprises (often SOEs) increasingly challenge European firms in third markets. Companies like CRRC often win contracts in emerging markets in Africa, Asia and South America, backed by cost advantages and Chinese financing. In the high value added HSR segment, China has matched the technological level of European rivals or surpassed them. China’s HSR manufacturing system is also comparatively technologically self-reliant. However, partly because of a global lack of demand for HSR systems, it has not yet exported its HSR technology to many markets or challenged European HSR competitors internationally.

- In shipping, European shipyards have been in decline for decades amid growing competition from Asia (initially from Japan and South Korea and now from China). China has major cost advantages in shipbuilding from lower wages and a massive expansion of China’s steel and aluminum production capacity, exceeding half of global capacity since 2015. It has done well building cargo ships with massive steel hulls, but is less advanced in higher-value segments. These include specialized vessels, such as cable laying or drilling ships, cruise ships and luxury yachts. China still relies on foreign technology for critical components such as engines, propellers, or marine radar systems. High technical barriers to entry and a high degree of specialization have enabled European companies to remain important in China’s marine components supply chain.

- In commercial aerospace, Airbus and European suppliers are among the world’s most competitive firms. Beijing is eager to become a major aerospace power itself, but while the C919’s initial commercialization on domestic routes amounts to a major step towards success, China remains dependent on foreign, including European technology. The HSR roadmap is less easily applicable to commercial aerospace. COMAC’s progress will therefore continue to be slower than that of China’s HSR leader CRRC. Still, COMAC and its Chinese suppliers are progressing, and European companies should be alert for increasing Chinese competition. Despite all these challenges it is the party’s ultimate goal to manufacture an indigenous passenger jet, using mainly Chinese suppliers and technology, that can compete with Airbus and Boeing in global markets.

- Endnotes

-

1 | Hoskins, Peter. BBC (2023). “China overtakes Japan as world's top car exporter”. May 19. https://www.bbc.com/news/business-65643064. Accessed: Oct 10, 2023.

2 | China Daily (2023). “China continues to lead in global shipbuilding market”. Jan 28. https://www.chinadaily.com.cn/a/202301/28/WS63d4e343a31057c47ebab90f.html. Accessed: Oct 10, 2023.

3 | China Daily (2023). “China continues to lead in global shipbuilding market”. Jan 28. https://www.chinadaily.com.cn/a/202301/28/WS63d4e343a31057c47ebab90f.html. Accessed: Oct 10, 2023.

4 | Methodological note to MERICS trade dependency database: trade dependencies are identified at the HS6 level, under the following conditions: (i) overall total imports of the product by China is twice higher than total exports; (ii) bilateral imports makes up for at least 30 percent of all the Chinese imports of that products; (iii) the world concentration of that product has a high concentration (i.e. Herfindahl-Hirschman Index above 0.25).

5 | State Council (2015). “国务院关于印发《中国制造2025》的通知” (State Council Notice on the Issuance of ‘Made in China 2025’). May 19. https://www.gov.cn/zhengce/content/2015-05/19/content_9784.htm.

6 | Naughton, Barry; Xiao, Siwen; Xu, Yaosheng (2023). The Trajectory of China’s Industrial Policies. La Jolla: University of California Institute on Global Conflict and Cooperation.

7 | MOFCOM (2016). “商务部等7部门联合下发《关于加强国际合作提高我国产业全球价值链地位的指导意见》” (The Ministry of Commerce and seven other departments jointly issued the Guiding Opinions on Strengthening International Cooperation to Improve the Position of China's Industries in the Global Value Chain). Dec 5. http://www.mofcom.gov.cn/article/b/fwzl/201612/20161202061465.shtml.

8 | For comparison, the key term ‘common prosperity’ (共同富裕) appeared over 800 times during the same time period.

9 | Measured on an HS2 level that includes parts and assemblies.

10 | Kennedy, Scott (2020). “China’s COMAC: An Aerospace Minor Leaguer”. Dec 7. https://www.csis.org/blogs/trustee-china-hand/chinas-comac-aerospace-minor-leaguer. Center for Strategic and International Studies (CSIS).

11 | MOT (2023). “《加快建设交通强国五年行动计划(2023—2027年)》解读” (Interpretation of the Five-Year Action Plan for Accelerating the Construction of a Strong Transportation State (2023-2027)). Apr 23. https://www.gov.cn/zhengce/2023-04/23/content_5752770.htm.

12 | Huang, Han; Xiong, Jie; Zhang, Junfang (2021). “Windows of Opportunity in the CoPS’s Catch-Up Process: A Case Study of China’s High-Speed Train Industry”. Sustainability 13(4): 2144. https://doi.org/10.3390/su13042144.

13 | Sohu (2023). “中国高铁被日本螺丝卡脖子,中国真造不出永不松动螺丝?” (China's high-speed rail is fully dependent on Japanese screws, is China rally unable to make screws that never loosen?). Apr 27. https://www.sohu.com/a/671540313_121687414. Accessed: Oct 11, 2023.

14 | Kennedy, Scott (2020). “China’s COMAC: An Aerospace Minor Leaguer”. Dec 7. https://www.csis.org/blogs/trustee-china-hand/chinas-comac-aerospace-minor-leaguer. Center for Strategic and International Studies (CSIS).

15 | Kennedy, Scott (2020). “China’s COMAC: An Aerospace Minor Leaguer”. Dec 7. https://www.csis.org/blogs/trustee-china-hand/chinas-comac-aerospace-minor-leaguer. Center for Strategic and International Studies (CSIS).

16 | CAAC (2017). “Li Jian Attends Regional Aviation and China-Made Regional Aircraft Development Forum 2017”. Nov 14. http://www.caac.gov.cn/en/XWZX/201711/t20171114_47548.html.

17 | Yang, Yijing (2022). “C919如何带飞1.4万亿大飞机产业链?中国商飞营收已破百亿,涉及38家上市公司,遍布陕西、江苏、山东……” (How does the C919 help the 1.4 trillion yuan large aircraft industry lift off? COMAC’s revenues have surpassed 10 billion yuan, involving 38 listed companies across Shaanxi, Jiangsu and Shandong). Sep 19. https://news.stcn.com/sd/202209/t20220919_4867999.html. Accessed: Oct 11, 2023.

18 | Jin, Zhuanglong (2012). “把大型客机项目建成创新型国家标志性工程” (Building the large passenger aircraft program into a landmark project for an innovative country). Sep 4. https://www.cscec.com/zgjzxb/xwzx7_8/gzdt78/201209/2795473.html. China State Construction Engineering Corporation (CSCEC).

19 | EET (2023). “国产化率达60%,国产大飞机C919产业链揭秘” (Localization rate reaches 60%, domestic large aircraft C919 industry chain revealed). May 30. https://www.eet-china.com/mp/a223436.html. Accessed: Oct 11, 2023.

20 | Airbus (2023). “Airbus and China aviation industry sign next phase in partnership”. Apr 6. https://www.airbus.com/en/newsroom/press-releases/2023-04-airbus-and-china-aviation-industry-sign-next-phase-in-partnership. Accessed: Oct 11, 2023.

21 | Hu, Zhe; Xie, Jiao (2017). “成功突破102项关键技术:C919 “大块头有大智慧”” (Successful breakthroughs in 102 key technologies: C919 "big man with big wisdom"). May 5. http://www.xinhuanet.com//politics/2017-05/05/c_1120926704.htm. Accessed: Oct 11, 2023.

22 | Jin, Zhuanglong (2012). “把大型客机项目建成创新型国家标志性工程” (Building the large passenger aircraft program into a landmark project for an innovative country). Sep 4. https://www.cscec.com/zgjzxb/xwzx7_8/gzdt78/201209/2795473.html. China State Construction Engineering Corporation (CSCEC).

23 | Sohu (2017). “哪些钢铁企业助力国产C919大飞机首飞成功?” (Which steel companies helped make the maiden flight of the domestically produced C919 aircraft a success?). Dec 21. https://www.sohu.com/a/211926297_651160. Accessed: Oct 11, 2023.

24 | CKHQ (2023). “长江1000发展策略十分巧妙!3项先进技术让它有底气叫板进口航发” (The Yangtze 1000 development strategy is very clever! 3 advanced technologies have the strength to challenge imported aircraft engines). Jan 28. https://www.ckhq.net/arc/hqck/jsck/2023/0128/580962_3.html. Accessed: Oct 11, 2023.

25 | Xinhua (2023). “Airbus China-assembled aircraft delivered to Philippine airline”. Jun 30. http://www.china.org.cn/business/2023-06/30/content_90218622.htm. Accessed: Oct 11, 2023.

26 | Kennedy, Scott (2020). “China’s COMAC: An Aerospace Minor Leaguer”. Dec 7. https://www.csis.org/blogs/trustee-china-hand/chinas-comac-aerospace-minor-leaguer. Center for Strategic and International Studies (CSIS).

27 | CAAC (2022). ““十四五”民用航空发展规划” (Civil Aviation Development Plan for the 14th Five-Year Plan). Dec 24. http://www.caac.gov.cn/XXGK/XXGK/FZGH/202201/P020220107443752279831.pdf.

28 | Lawrence, Martha; Bullock, Richard; Liu, Ziming (2019). China’s High-Speed Rail Development. International Development in Focus. Washington, DC: World Bank. doi:10.1596/978-1-4648-1425-9.

29 | Freifeld, Karen; Alper, Alexandra (2020). “U.S. weighs blocking GE engine sales for China's new airplane: sources”. Feb 15. https://www.reuters.com/article/us-usa-china-aircraft-idUSKBN2090SG. Accessed: Oct 11, 2023.

This MERICS Policy Brief is part of the “Dealing with a Resurgent China” (DWARC) project, which has received funding from the European Union’s Horizon Europe research and innovation programme under grant agreement number 101061700.

Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union. Neither the European Union nor the granting authority can be held responsible for them.

Author(s)

Former Chief Economist

Senior Analyst, Rhodium Group and former Analyst, MERICS

Author(s)

Former Chief Economist

Senior Analyst, Rhodium Group and former Analyst, MERICS

Content