picture alliance / Long Wei / Costfoto

Germany: From mutual benefit to existential competition with China

You are reading the Germany chapter of the 2026 report of the European Think Tank Network on China (ETNC) "Fragmented Europe: Dealing with China as a technology and innovation power". Go back to the main page.

By Claudia Wessling and Bernhard Bartsch

After decades of highly lucrative technology cooperation with China, Germany finds itself in an existential crisis. China has been catching up in high-tech and research areas where Germany has traditionally been a leader. Fears of losing key industries and potentially hundreds of thousands of jobs have led to soul-searching about reviving German competitiveness. But diverging strategies emerge along the fault lines of politics and business. While the German government tries to shift its focus on security politics and geoeconomics, many companies and research institutions consider the risks of not cooperating with China on innovation as being higher – and are doubling down on their engagement with Chinese partners.

Recent trends: Balancing more conscious risk management and staying at the competitive edge in science and tech

In the spring of 2026, German debates on China are shaped by concerns of a looming existential crisis. The German export industry appears to be in free fall, seemingly over-whelmed by a “China Shock 2.0”, a flood of Chinese products of remarkable quality at prices that European companies can hardly compete with. Business leaders are getting increasingly vocal about their frustration with political processes in Berlin and Brussels that they see as much too slow and insufficient to save or transform Germany’s economic model. And even though chancellor Friedrich Merz and leading figures in his coalition government share the concern and sense of urgency, they appear overwhelmed by the global turmoil from Ukraine to Iran that is leaving little room and few resources to undertake long overdue structural reforms.

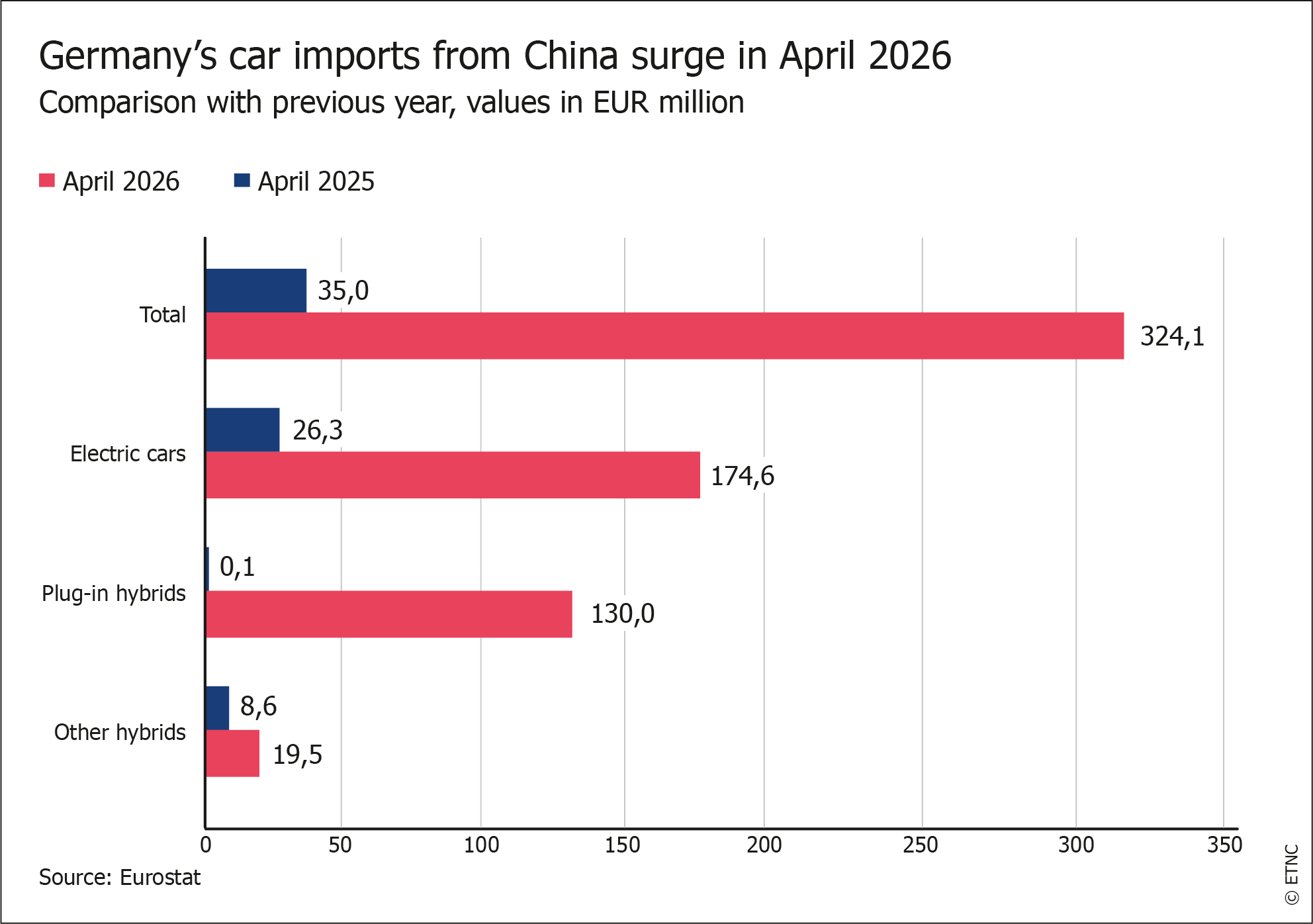

There is growing concern about risks emanating from excessive dependence on innovative Chinese products, like batteries for electric vehicles, photovoltaics or wind energy equipment. In sectors that were traditionally dominated by German companies, such as automotives or mechanical engineering, China has emerged as a serious competitor that threatens Germany’s industrial base and by extension the value and production chains in many other European countries.

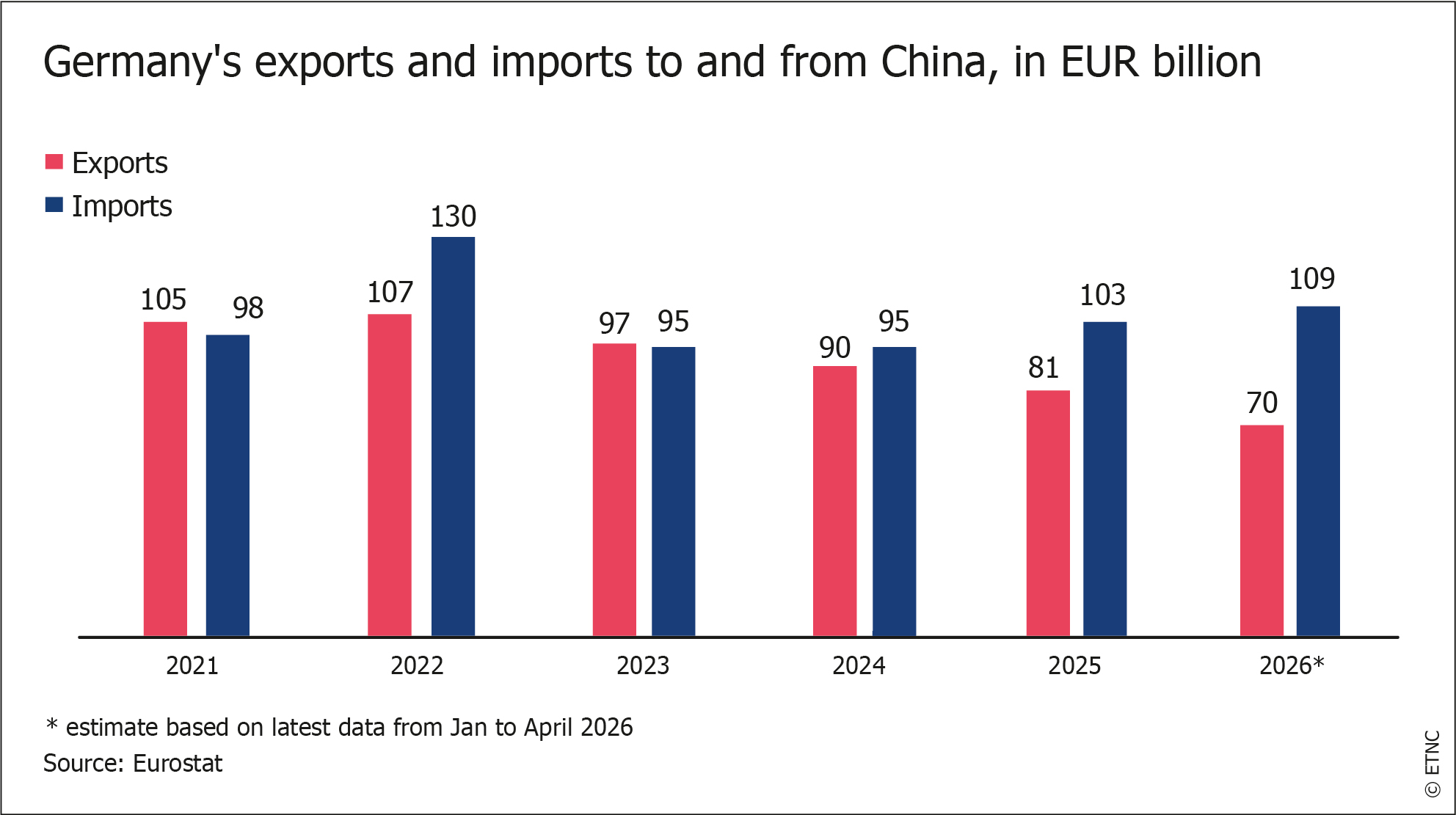

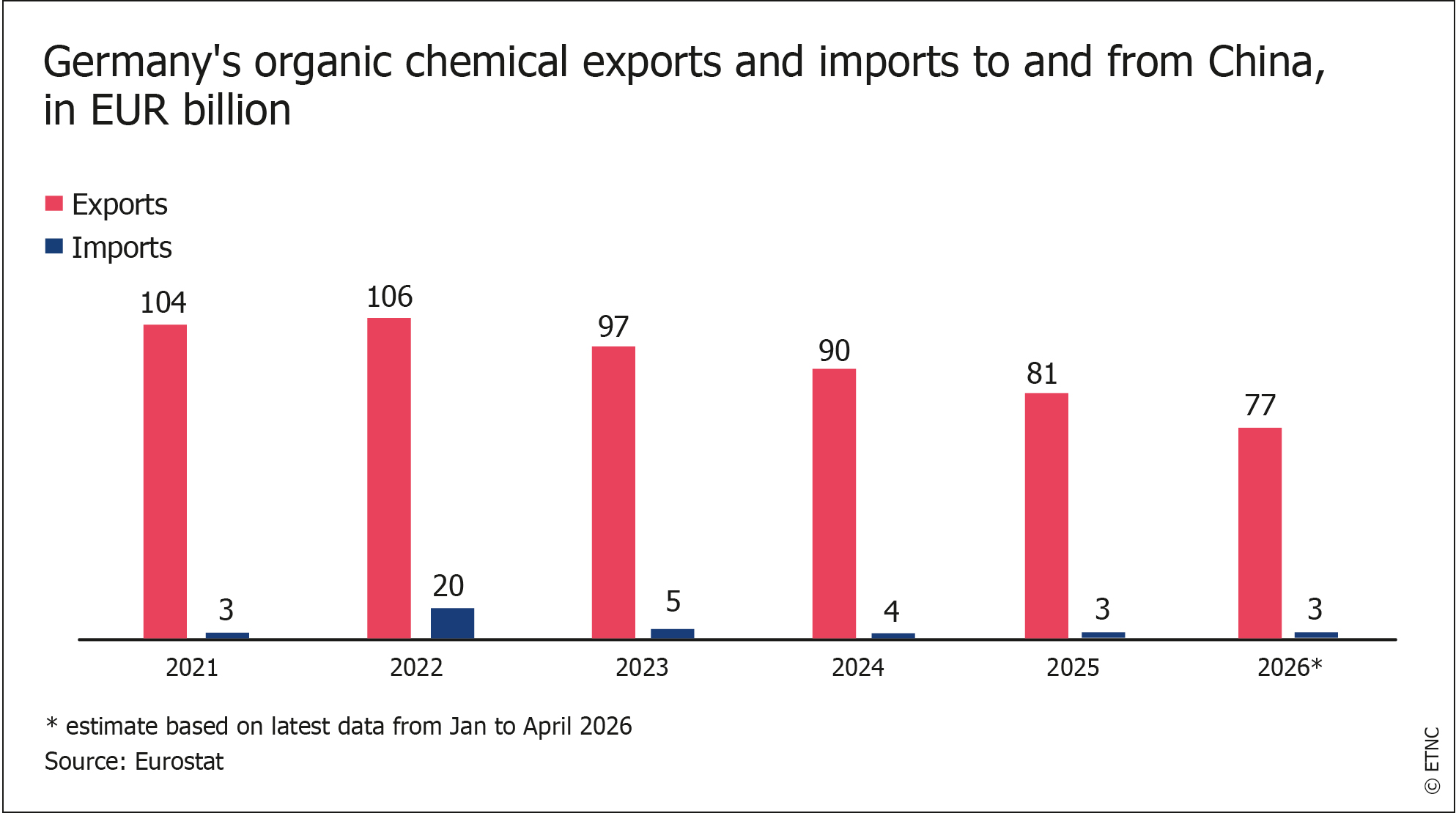

In 2025, around 120,000 industry jobs were lost in Germany,1 and competition from China is considered a main factor (even though no reliable figures exist that attribute clear causality). Bosch alone has announced cutting more than 20,000 jobs in its automotive division due to weak global demand for German cars.2 In 2025, Germany’s exports to China decreased by 9.7%, while imports of Chinese goods increased by 8.8% (year-on-year).3 With this sense of crisis comes a new round of fierce debates about the role of China for Germany’s tech and innovation prowess. Both the business and the scientific research communities stress the importance of upholding connections with the PRC, now considered a trend setter in key technologies and innovation hub for researchers. While politicians have emphasised the need for greater research and economic security as part of the de-risking agenda laid out in Germany’s China strategy (2023), companies increasingly demand that they be “left alone” to do their businesses, and a considerable part of the scientific community insists on maintaining the spirit of “Wissenschaftsfreiheit” - freedom of science.

Automotive, machinery, climate technologies and STEM research: Where China’s innovation strategies are most relevant for Germany

Years of discussions about a national China strategy have led to a largely mainstreamed understanding of the risks China’s technological progress poses to German as a high-tech powerhouse. It’s the strategies derived from this analysis where positions diverge.

When Beijing announced its “Made in China 2025” strategy in 2015, German companies took China’s ambitions seriously but largely doubted that China would achieve a good part of its ambitions within only ten years.4 But now the tables seem to be turning. According to the UN Innovation Index published in autumn 2025, Germany is no longer among the top ten on the list of most innovative nations. It dropped to be only ranked 11th – behind China, ranked 10th.5

China no longer depends on Germany as much for access to high-tech products and highly specialised knowledge. It is now German economic actors who are looking to China for innovative approaches and technologies. They argue that China is indispensable as a location for innovation to maintain their own competitive edge, both on the Chinese and international markets. This applies to industries such as automotive, mechanical engineering, chemicals, and pharmaceuticals.

Nevertheless, the outlook differs across different sectors. Three German industries in particular - the automotive industry, mechanical engineering and automation, and green and climate tech – are strongly affected by China’s innovation success. Cutting across each of these is the underlying theme of science and research collaboration, where the German community appears keen to press against the grain of research security.

The automotive industry and its suppliers: Feeling the heat of China’s innovation

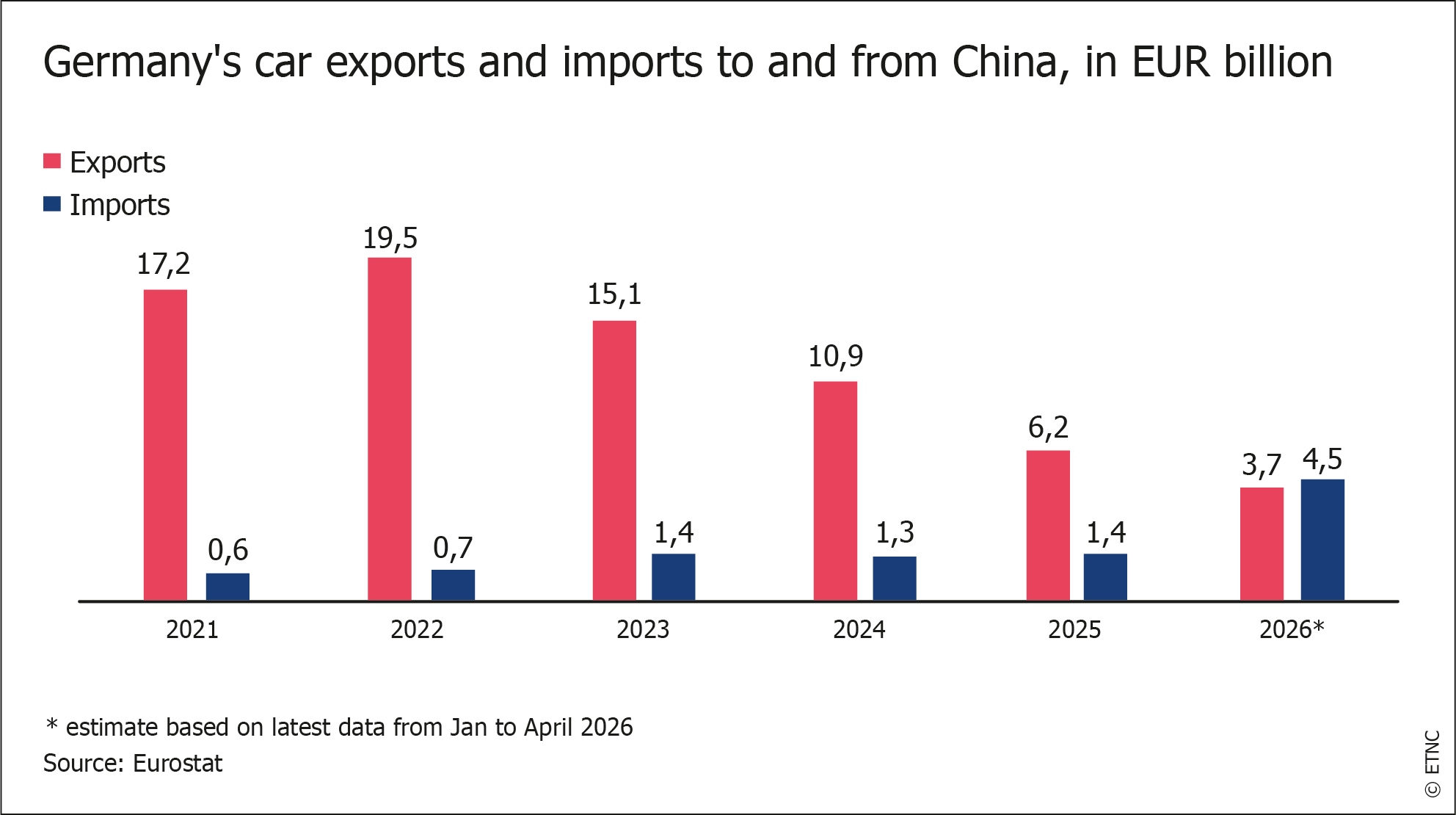

The automotive industry, the backbone of Germany’s economy, is feeling the heat of China’s innovation most acutely.6 After decades of lucrative collaboration in joint ventures in China, German auto makers like BMW, VW and Mercedes see the China share of their revenue declining. According to a study of consulting firm E&Y published in December 2025,7 competition from China especially in the EV sector, sluggish demand for German premium cars and US tariffs have caused a “perfect storm for German carmakers”. The study points to development speed, agility and completely digitalised R&D processes as a main strength of Chinese competitors like BYD, Geely and Great Wall Motors.

According to the study, German carmakers altogether saw their profit margins shrink by 76% in the 3rd quarter of 2025 alone. In China, German carmakers saw their sales dropping to a 13-year low last year.8 China has become a global leader in production of lithium-ion batteries, controlling almost the entire value chain from the extraction of raw materials to the production of the batteries.9 According to a study by the Institute of Economics (IW) in Cologne10, there is an imminent threat (to German industry) of China leapfrogging also in other areas of the electrification and digitalisation of the automotive industry.

Several measures have been taken both on the political and business level to navigate the increasing competition from China in the mobility sector. To avoid becoming overly dependent on battery supply chains, for instance, Chinese producers are incentivised to invest in battery plants in Germany. Battery maker CATL has built a plant in Arnstadt in the federal state of Thuringia, producing battery capacity for at least 200,000 EVs per year and supplying also European car makers.11

The plant is considered by many a positive example of what future cooperation strategies with China could look like: by bringing Chinese innovative tech to Germany or Europe, local producers and universities can work closely with Chinese counterparts on domestic soil, avoiding unwanted tech transfer and other supply chain risks arising from German companies’ localisation in China. During his visit to Beijing in February 2026, Chancellor Merz also called for more Chinese investments in Germany: “We want jobs in Germany with Chinese investments”, he stressed.12 However, it remains unclear how it will be ensured that local German stakeholders benefit from the investments.

Mechanical engineering and automation: Increasing competition with China for global market shares

For a long time, China has depended on German high-tech machinery to innovate its industry. The case of Chinese takeover of German robot maker Kuka in 2016 marked the beginning of a changing of tides and China’s rise in robotics. Ever since, the German industrial automation industry has come under increasing pressure in the competition for global market shares. Faced with the “Buy China” trends, German companies in the sector also increasingly feel compelled to localise in China and enter into cooperative arrangements with domestic players.

“Made in China 2025” targeted exactly those areas in which Germany used to be a technological frontrunner, like industrial robotics, high-end computerised machines, high-performance medical equipment or advanced railway transportation equipment. At the time, Beijing’s industrial innovation strategy was welcomed by many German actors as a booster for more mutually beneficial cooperation in the targeted sectors. The ambition never really materialised. Instead, China has reached its goal of becoming a global leader in key manufacturing sectors in many areas. According to the German Engineering Federation (VDMA), Chinese machinery manufacturers delivered goods worth EUR 20 billion to the EU in 2018. That figure has reached EUR 48.7 billion in 2025.13

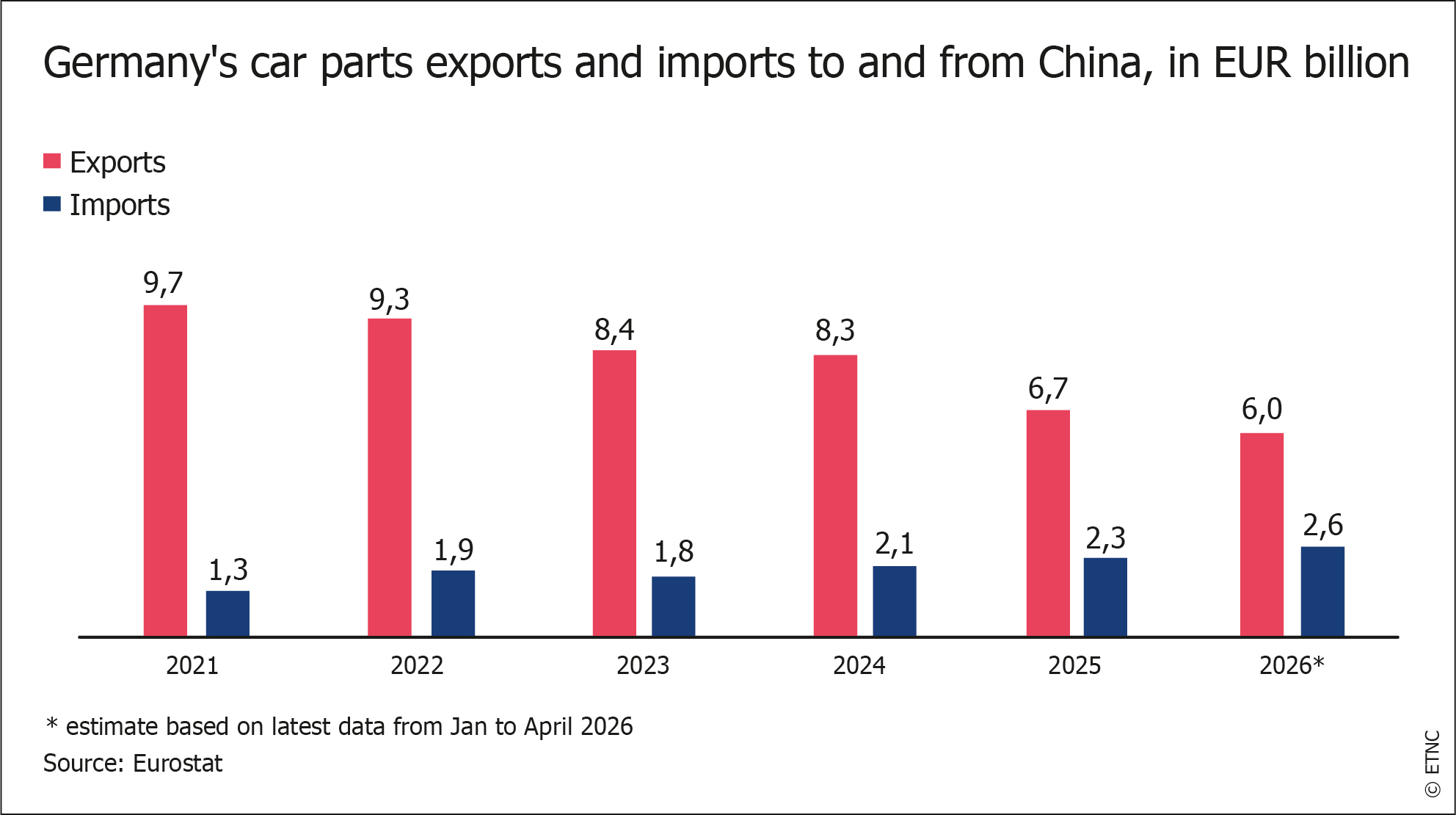

Even though Germany still exports more machinery to China than vice versa (2025 exports: EUR 16.2 million, imports: EUR 11.9 million)14, VDMA, an association for the machinery and equipment manufacturing industry in Europe and Germany, has called for improved conditions and deep reforms in Germany to prevent more research and production from being relocated to foreign countries.15

Green and climate tech: the predicament of an industry falling behind

China has become a dominant producer of climate technology, one of the fastest growing industry sectors, reaping growing shares of the estimated five-billion-dollar revenues worldwide.16 Germany – once the home of “solar valley” in the country’s east – has fallen behind. China’s high innovation speed and competitive pricing of relevant products is also increasing German dependency on wind turbines, photovoltaic and energy storage equipment from China. German companies in the sector are in a predicament: So far, there is no solution of how to gain access to Chinese innovation while at the same time protecting Germany’s industry from competitors that provide low-cost and high-quality solutions also due to ample financial support by the Chinese state.

According to a study published by the Boston Consulting Group (2025),17 Germany is losing competitiveness in the field of environmental technologies to China. Obstacles include high electricity prices, lengthy approval procedures, and a lack of investment incentives for companies. According to the study, China spends more money on environmental technology than other regions of the world, invests more quickly, and is thus consolidating its control over value chains in green technology. “For the first time, the epicentre of innovation is shifting from traditional Western centres to China,” the study states.

Science and research: a scientific community that wants engagement despite risks

Science and research on the academic level are areas where China remains keenly in-terested in collaborating with German counterparts. In recent years, the debate over risks emanating from research collaboration has gained traction: cases of alleged bribery of German professors (RWTH Aachen)18 or the explicit warnings by the German intelligence service against science espionage from China in its yearly reports have raised eyebrows. There is increased risk awareness in fields like quantum or AI.

However, this heightened risk perception collides with a continuously high interest on the part of German scientists to continue established collaboration with Chinese counterparts. The focus of these collaborations clearly is on STEM and subject matters that are at the core of China’s innovation strategy. According to 2025 figures,19 205 German institutions of higher education maintained collaborations with 338 Chinese counterparts. China continues to be attractive due to its high pace of innovation, a highly motivated and flexible talent pool, and generous funding for research areas prioritised by Beijing’s innovation agenda.

In a recent survey of the research organisation Max Planck Gesellschaft, 55% of respondents stated that science collaboration with China was “important and even essential” for their research. According to that same institution, more than 3,700 joint publications were published by MPG and the Chinese CAS alone.20

German universities and research associations have launched programs21 to increase China expertise and published guidelines so that researchers can develop an informed approach and develop strategies for risk management, e.g., of technology and knowledge outflow, lack of access to jointly developed research data, or dual use.

Recent measures: Defending the competitive edge with a German high-tech agenda

In late fall 2025, German Chancellor Friedrich Merz presented his government’s new high-tech agenda by stressing: “The US and China must not be allowed to determine the future of technology on their own”. 22 The goals formulated in the strategy reflect the ambition to strengthen the technological sovereignty of Germany and Europe in a world marked by geopolitical conflicts and a struggle for tech supremacy.

According to the strategy, ten percent of Germany’s economic output is to be generated by AI-based technologies by 2030. The federal government wants to expand chip production capacities, establish competitive battery production in Germany by 2035, and expand research and development of alternative car engine technologies and climate-friendly fuels. It is no coincidence that the areas mentioned are ones in which China has made great strides in recent years.

Merz’s high-tech strategy is just one of several measures targeted at safeguarding Germany’s position as a hub of industrial and scientific innovation. For example, fears of unwanted technology and knowledge transfer prompted the German government to, at the end of 2025, agree on a framework for strengthening research security. It calls for a “holistic and nationwide approach” to systematically strengthen “knowledge security in Germany and Europe.” There are also plans to establish a national platform on the topic, and even the German Research Association (DFG) recently emphasised the need for “more security” in research and science. “As open as possible, as protected as necessary”, is the new slogan issued by the funding institution for promoting international scientific cooperation in this new era of geopolitical disruption.

For a more informed approach to collaboration with China, the German Ministry of Research plans to establish a national “China Competence Network” in which central and regional actors contribute to providing independent knowledge about China to those involved in exchanges on innovation and technology issues.23

The debate on how to deal with China as a rising innovation power is closely linked to the question of how to achieve a calibrated “derisking”. Some have brought up the concept of “Chinese Walls”: Whether to engage in cooperation with China depends on the assessment of the criticality of the technology or area of innovation in question. While avoiding critically sensitive areas, others should, in principle, remain open for collaboration. Inviting Chinese innovative companies to invest and build factories in Europe is also seen as part of the solution.

Outlook: Risks of innovation collaboration outweigh the opportunities for Germany

According to a recent survey published by the German Chamber of Commerce in China24 more than two thirds of German firms (68%) favour R&D collaboration with China. Re-spondents from 55% of the companies surveyed also emphasised that the benefit of R&D engagement was mutual: while a transfer of know-how from German mother companies to China (63% of cases) could be observed, so could a transfer from China to Germany (40%).

Despite these arguments from companies, there is also consensus that Germany will need to both invest in its own domestic capabilities to innovate and take measures to become more independent from China and the US.

China’s rise to become a high-tech nation has a massive impact on Germany, which has a similar focus. The long-term effects on the dynamic of mutual innovation and on Germany’s economy as a whole are uncertain, but the following scenarios illustrate two trajectories that feature prominently in current discussions:

- The de-industrialisation nightmare: China’s momentum continues and it increasingly dominates key industries. The “China Shock 2.0” will mark the end of Germany’s export driven economy, with major companies going into decline. Despite calls for de-risking, many of these businesses will see no other chance than pinning their hopes on extending tech and R&D collaboration with China. What may be good for some businesses as well as research clusters will come at a high price for Germany as an economy and undermine its position as a breeding ground for top-notch basic and applied science and research.

- Regrouping for a proper decoupling: As counterintuitive as this may seem in early 2026, there remains the prospect of a large coalition of G7-led countries forming a block that seeks to break dependencies from China and establish a hemisphere in which Chinese tech is pushed to the margins. Many in the US still seem convinced that they can build on their own dominance and “allied scale” to contain China’s ambitions. The likelihood of such a trajectory would not only depend on a friendlier mindset in Washington towards its partners, but mostly on maintaining the competitive edge in Europe. Defensive measures against Chinese overproduction can buy time, but Germany must make substantive efforts to increase competitiveness, innovation and global partnerships.

Graphics provided by Rafael Jimenez Buendía, MERICS Senior Associate Fellow and author of the SOAPBOX newsletter on EU-China trade relations.

- Endnotes

1 | F.Specht. 120.000 Industriejobs sind innerhalb eines Jahres weggefallen. Handelsblatt. 1 April 2025. https://www.handelsblatt.com/politik/konjunktur/arbeitsmarkt-120000-industriejobs-sind-innerhalb-eines-jahres-weggefallen/100118017.html

2 | Tagesschau. 30 January 2026. https://www.tagesschau.de/tagesschau_20_uhr/ts-76206.html

3 | Statistisches Bundesamt. China im Jahr 2025 wieder wichtigster Handelspartner Deutschlands. 20 February 2026. https://www.destatis.de/DE/Presse/Pressemitteilungen/2026/02/PD26_056_51.html

4 | M. Cui, S. van Ackern. Made in China 2025: Der stille Machtwechsel. Deutsche Welle. 20 Jan-uary 2026. https://www.dw.com/de/made-in-china-2025-der-stille-machtwechsel-deutschland-e-auto-batterien-roboter-europa/a-75524843

5 | World Intellectual Property Organization (WIPO). Global Innovation Index 2025 results. 2025. https://www.wipo.int/web-publications/global-innovation-index-2025/en/gii-2025-results.html

6 | N. Martin, A. Becker. Deutschlands Autoindustrie: Schicksalskampf um die Zukunft. Deut-sche Welle. 3 January 2026. https://www.dw.com/de/deutschlands-autoindustrie-schicksalskampf-um-die-zukunft-der-mobilit%C3%A4t/a-75367240

7 | EY. Gewinneinbruch in der weltweiten Autoindustrie – Marge auf 10-Jahres-Tiefstand. 15 Decem-ber 2025. https://www.ey.com/de_de/newsroom/2025/12/ey-automotive-bilanzen-q3-2025

8 | L. Backovic, M. Scheppe. Deutsche Autobauer rutschen in China auf 13-Jahres-Tief. Handels-blatt. 14 January 2026. https://www.handelsblatt.com/unternehmen/industrie/vw-bmw-mercedes-deutsche-autobauer-rutschen-in-china-auf-13-jahres-tief-02/100188654.html

9 | Fraunhofer FFB. Study on the battery supply chain shows China’s global dominance – and options for Europe. 18 February 2025. https://www.ffb.fraunhofer.de/en/press/news/Chinas_Dom-inanz_in_der_Batterielieferkette.html

10 | M. Haag, E. Kohlisch, O. Koppel. China auf dem Weg zur führenden Technologienation. Institut der Deutschen Wirtschaft.19 October 2023. https://www.iwkoeln.de/studien/maike-haag-enno-kohlisch-oliver-koppel-china-auf-dem-weg-zur-fuehrenden-technologienation.html

11 | M. Cui, S. van Ackern. Made in China 2025: Der stille Machtwechsel. Deutsche Welle. 20 January 2026. https://www.dw.com/de/made-in-china-2025-der-stille-machtwechsel-deutschland-e-auto-batterien-roboter-europa/a-75524843

M. Cui, S. van Ackern. Das Ende von „Made in Germany“? Chinas Mega-Fabrik in Thüringen:

„Das ist das Beste, was uns passieren kann.“ Focus. 29 January 2026. https://www.focus.de/earth/bedeutet-chinas-hightech-fabrik-in-thueringen-das-aus-von-made-in-germany_e6739ba1-4141-4c0c-8cdf-4a8fb90021a0.html12 | Wirtschaftswoche. Merz nennt China einen „umfassenden strategischen Partner“. 25 February 2026. https://www.wiwo.de/politik/deutschland/schwieriger-besuch-merz-stellt-fuenf-leitlinien-fuer-china-reise-auf/100202959.html

13 | J. Gernandt. Investitionen als Schlüssel zur wirtschaftlichen Erneuerung. VDMA. https://www.vdma.eu/de/maschinenbau-zahl-bild

14 | VDMA. Deutscher Maschinenaußenhandel. December 2025. https://www.vdma.eu/documents/d/group-34568/deutschland_maschinenaussenhandel

15 | VDMA. Wettbewerb auf Augenhöhe: Ein Appell an die Politik im Umgang mit China. 2025. https://www.vdma.eu/documents/d/group-34568/chinaposition_2025_d_final-1

16 | Süddeutsche Zeitung. Studie: Umwelttechnologie boomt und China dominiert. 2 December 2025. https://www.sueddeutsche.de/wissen/klima-und-technologiewettlauf-studie-umwelttechnologie-boomt-und-china-dominiert-dpa.urn-newsml-dpa-com-20090101-251202-930-367721

17 | Boston Consulting Group. Green Economy wächst auf 5 Billionen Dollar – China dominiert, Deutschland unter Zugzwang. 2 December 2025. https://www.bcg.com/press/2december2025-green-economy-wachst-auf-5-billionen-dollar-china-dominiert-deutschland-unter-zugzwang

18 | T. Eckert. Die Bling-Bling-Professoren aus Aachen. Correctiv. 18 June 2024. https://correctiv.org/aktuelles/china-science-investigation/2024/06/18/die-bling-bling-professoren-aus-aachen/

19 | Hochschulrektorkonferenz (HRK). Internationale Hochschulkooperationen. https://www.internationale-hochschulkooperationen.de/home.html

20 | T. Gabel. China-Kooperationen: „Wir brauchen ein gemeinsames Moonshot-Projekt“. Table.Briefings. 30 October 2024. https://table.media/research/interview/china-kooperationen-wir-brauchen-ein-gemeinsames-moonshot-projekt

21 | For instance, the German Research ministry has funded regional competency centers in the

„Regio China“ framework, which ended in 2025. Bundesministerium für Forschung, Technologie und Raumfahrt (BMFTR). China. https://www.bmftr.bund.de/DE/Forschung/International/Asiatisch-PazifischerRaum/China/china_node.html22 | Bundesregierung. Rede von Bundeskanzler Merz bei der Auftaktveranstaltung zur „Hightech Agenda Deutschland”. 29 October 2025. https://www.bundesregierung.de/breg-de/aktuelles/kanzler-hightech-agenda-2391454

23 | Details on the framework are expected to be made public in 2026.

24 | Deutsche Außenhandelskammer (AHK). Business Confidence Survey 2025/26. 2 December 2025. https://china.ahk.de/en/news/business-confidence-survey-2025-26?utm_source=chatgpt.com