picture alliance / CFOTO

Tracker

China Economic Indicators

China's economy in Q1: Economy rebounds as geopolitical fallout is yet to come

MERICS China Economic Indicators Q1/2026

This analysis is part of the Q1/2026 MERICS China Economic Indicators, our quarterly analysis of China’s economic data. You can find the most recent data here.

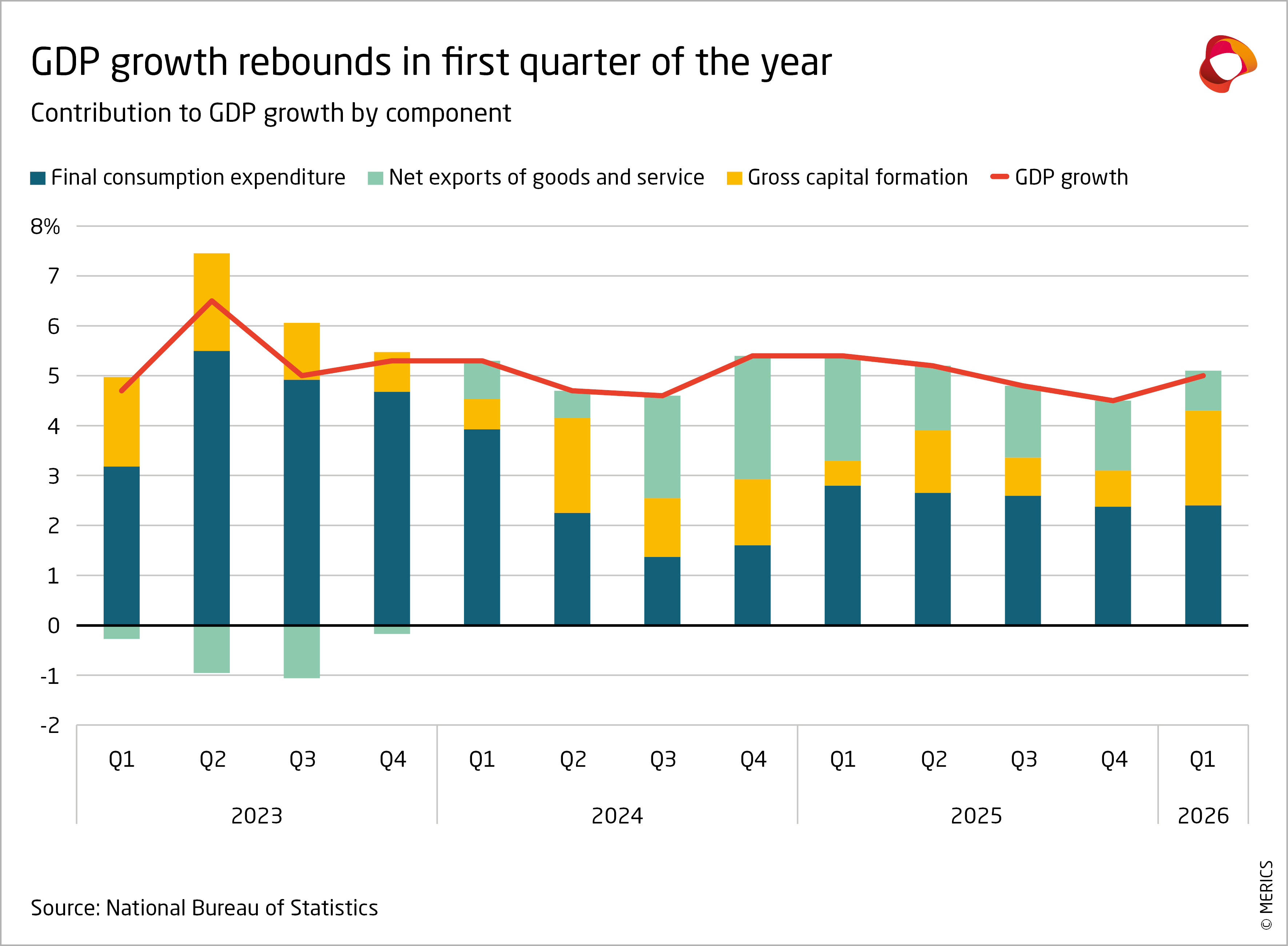

Amid global turbulence, China’s GDP expanded by five percent according to the official statistics in the first three months of 2026, up from 4.5 percent in Q4 last year. It was stronger than the market consensus of 4.8 percent and at the top end of the leadership’s target of 4.5-5 percent annual growth this year. Strong investment in infrastructure and manufacturing, led by state-owned enterprises, was crucial in returning fixed-asset investment (FAI) growth to positive territory. Yet the overall picture of the economy has not changed: growth continues to rely on strong manufacturing and exports, while consumption remains weak. The government’s cautious approach to policy support may be tested in the coming months as global uncertainties increase.

Geopolitical turbulence had limited impact on China

China remained relatively insulated from the US war with Iran in Q1. While much of Asia faced energy disruptions and price spikes due to the closure of the Strait of Hormuz, China was cushioned by large fuel reserves. China sources roughly half of its crude oil from the Middle East, but its exposure is less acute than peers such as Japan, which relies on the region for the 95 percent its imports. A diversified energy mix - still anchored by coal - offers further insulation. While some Asian countries have already taken drastic steps to reduce energy demand, such as four-day working weeks or extended public holidays, China looks comparatively well placed.

China’s government has been able to moderate oil price increases somewhat by using its substantial stockpiles and price ceilings for gasoline and diesel. In March, the producer price index (PPI) for the oil and gas extraction sector jumped by 15.8 percent, and headline PPI rose to 0.5 percent, its first increase in over three years. China's crude oil imports remained relatively steady in March, falling just 2.8 percent year-on-year from a high base, as these cargoes were loaded in January and February. Direct constraints on China’s fuel supply will only begin to show in Q2.

So far, China’s trade with the world has been barely affected by the conflict in the Middle East. China recorded a strong increase in trade volumes in Q1, with imports up 22.7 percent and exports up 14.7 percent, the largest quarterly growth figures for either since the start of 2022. Strong imports were driven by demand for commodities and high-tech components rather than consumer goods, showing that the increase does not reflect any improvements in household demand or a structural shift in the drivers of growth.

Moderate measures not enough to stimulate consumption

Household sentiment remains subdued by the protracted downturn in the property market and still-fragile labor market. Retail sales rose a mere 2.4 percent year-on-year in the first three months of the year (which included the Chinese New Year holiday), offering little sign of an imminent rebound. Consumption is unlikely to accelerate significantly without more forceful policy action. So far, the government has opted for an incremental approach. Efforts have focused on stabilizing employment and nudging up incomes. Firms are being subsidized to retain workers and hire graduates and local governments have raised minimum wages. In the past year, 27 of China’s 31 provincial-level jurisdictions have implemented minimum wage increases; half of these rises were in double-digits.

China’s strategy before the US-Israeli attack on Iran appeared to hinge on patience: shore up the labor market, lift incomes gradually and allow confidence to recover in time. Given the relatively large role of consumption in China’s GDP, even a modest improvement could offset weakness elsewhere. Yet the odds of success are diminishing. The lengthening conflict in the Middle East is likely to stoke inflation, squeezing both corporate margins and household purchasing power. In that case, gradualism may prove insufficient.

Leadership to remain calm as economy enters choppy waters

The longer the US-Israeli war with Iran lasts, the more difficult it will be for China to keep economic growth within their target range for the year. The chief danger is that rising inflation, at home and abroad, could undermine efforts to revive consumption while dampening global demand for Chinese exports. China’s cost advantages and relative energy stability may allow its firms to gain market share even as global demand softens. But this would be a consolation prize: the overall volume of exports might still decline.

Despite these risks, China’s leaders may hold off on any major policy changes for the time being. A strong start to the year gives policymakers some breathing room. Experience suggests that, in times of stress, Beijing’s instinct is not to unleash consumption-led stimulus but to double down on industrial policy, supply-chain resilience and technological self-sufficiency.

Ultimately, China’s performance will be judged in relative terms. If it can maintain stability while other economies succumb to inflation - or worse, stagflation - the leadership may see little reason for alarm. In a troubled global economy, merely weathering the storm could be counted as success.

Autor(en)

Senior Analyst

Autor(en)

Senior Analyst