picture alliance / Long Wei / Costfoto

Content

EU: Shepherded by Brussels, Europe awakens to Chinese technology

You are reading the EU chapter of the 2026 report of the European Think Tank Network on China (ETNC) "Fragmented Europe: Dealing with China as a technology and innovation power". Go back to the main page.

By Rebecca Arcesati

EU-China innovation relations have turned more difficult in recent years. Although government policies cannot undo deep interdependencies in science and business overnight, cooperation no longer goes uncontested. The exclusion of Chinese entities from large parts of the Horizon Europe funding program and capitals’ increased scrutiny of Chinese investments into high-tech sectors are just two examples of a wider transformation: From largely unconditional openness to China in science and technology, the EU’s approach has shifted towards a logic of “de-risking” and economic security.1

Technology and innovation in EU-China relations: from openness to economic security

Amid intense geopolitical and technological rivalry between Beijing and Washington, Euro-peans increasingly find themselves in a position of relative disadvantage and dependency. To be sure, European companies control “chokepoints” on some of the world’s most critical technology value chains, such as advanced semiconductor fabrication, and occupy im-portant niches for energy systems and connectivity – both crucial for the data centres and networks upon which artificial intelligence (AI) relies.2 But the continent is quickly falling behind when it comes to developing, deploying, and setting the standards for tomorrow’s most disruptive technologies.

In this context, supply-side dependencies on China for critical technologies and their inputs are viewed with growing preoccupation. Opportunities and the necessity of cooperation notwithstanding, there is growing recognition that the People’s Republic of China (PRC)’s ambitions and capabilities pose serious challenges to Europe in terms of supply chain resilience, technological security, critical infrastructure security, and exposure to economic coercion. The Economic Security Strategy from 20233 reflected an emerging EU-wide con-sensus regarding the nature of these challenges, even though profound divisions remain between – and within – member states as to urgency and acceptable costs of specific responses.

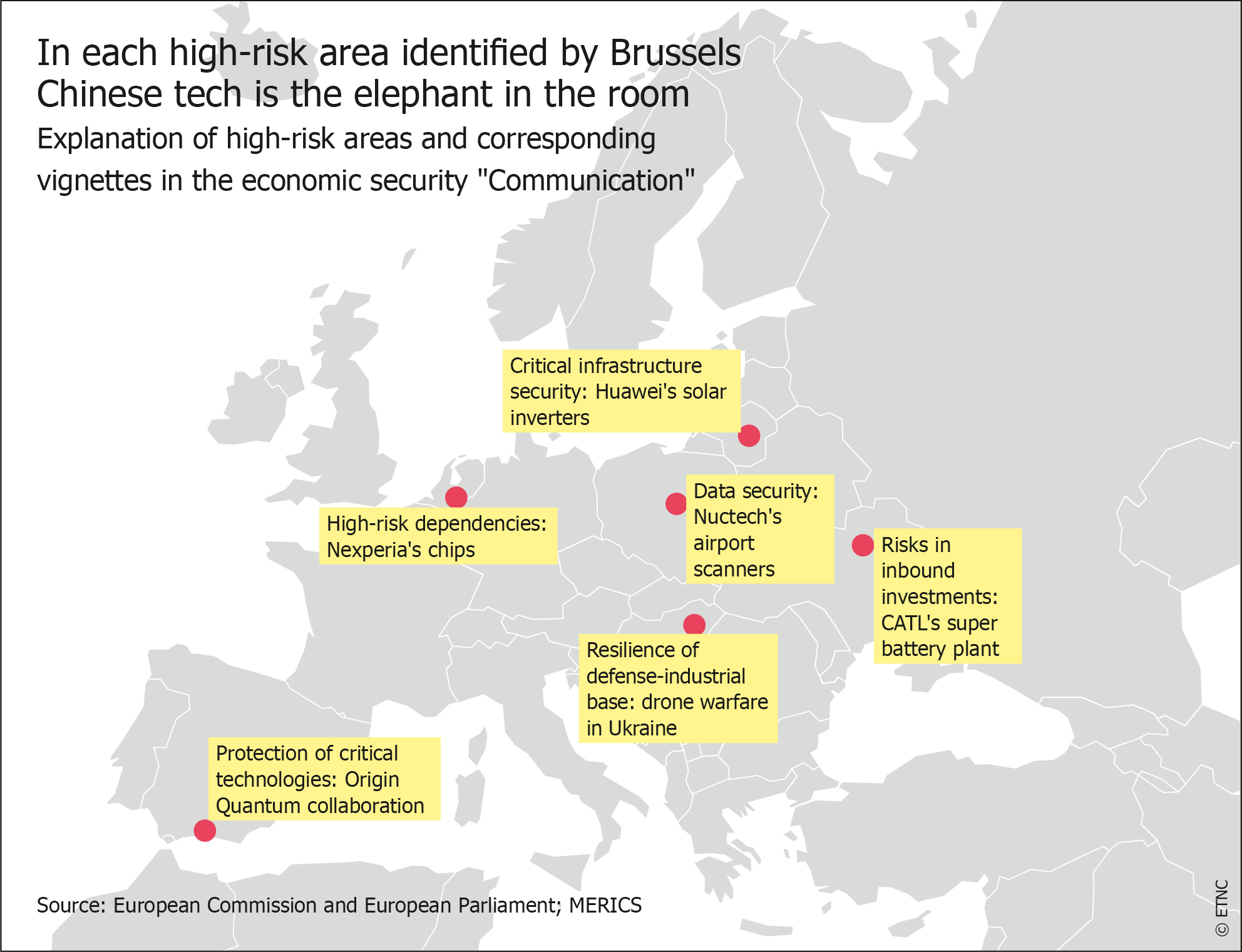

Against this backdrop, Brussels aims to turn the economic security agenda from paper to practice. The Joint Communication by the European Commission and the High Represen-tative on strengthening the EU’s economic security, published in December 2025, offered the clearest official diagnosis yet of the challenges that China’s techno-industrial system poses to the bloc’s resilience, security, and long-term competitiveness.4 PRC-origin tech-nology looms large in each of the high-risk areas identified as needing the most urgent action – from Europe’s strategic import dependency for chips to the security and resilience of its energy grids. This assessment reflects a growing consensus among experts and an-alysts in and outside governments.

Focus areas: EU-China interaction in technology and innovation

Foundational semiconductors: Nexperia’s saga brings strategic dependencies in focus

The EU’s collective reliance on China as a technology supplier is a top priority on the de-risking agenda. After the Dutch government used emergency powers in October to seize control of semiconductor manufacturer Nexperia from its Chinese parent, Wingtech Technology, the European automotive industry found itself embroiled in a dramatic supply shock.5 Beijing responded the move, which the Netherlands had taken to address the al-leged improper transfer of assets by Nexperia’s since-ousted CEO, by blocking shipments of packaged chips from the company’s plants in China.6 Because Nexperia sent around 70-80% of its wafers to China for processing, testing and packaging, foreign carmakers have been left exposed to Beijing’s export restrictions. Despite the experience of the Covid-19 pandemic, companies from Volkswagen to Bosch, having failed to prepare for possible disruptions, were forced to cut or suspend production lines.7

A lesson in the importance of robust and consistent screening rules for foreign direct invest-ment (FDI) across Europe, Nexperia’s case also highlights a key weakness in EU econom-ic and technological security: The bloc’s growing dependency on China for mature-node semiconductors, also known as “legacy chips”.8 Long seen as relatively unimportant, these integrated circuits, which include the ones Nexperia produces, are foundational to the functioning of industries ranging from automotive and medical devices to drones, robotics, aerospace and defence, to name a few.

China controls around 30% of front-end capacity (i.e., chip fabrication), not including semi-conductor assembly, testing and packaging (ATP, also commonly referred to as back-end manufacturing).9 On top of that, like Nexperia, other European chipmakers, such as ST-Micro, also do much of their back-end manufacturing in China before selling packaged chips to their consumers – including European companies that produce in China for export. This vital technology trade is therefore vulnerable to potential Chinese government export restrictions.

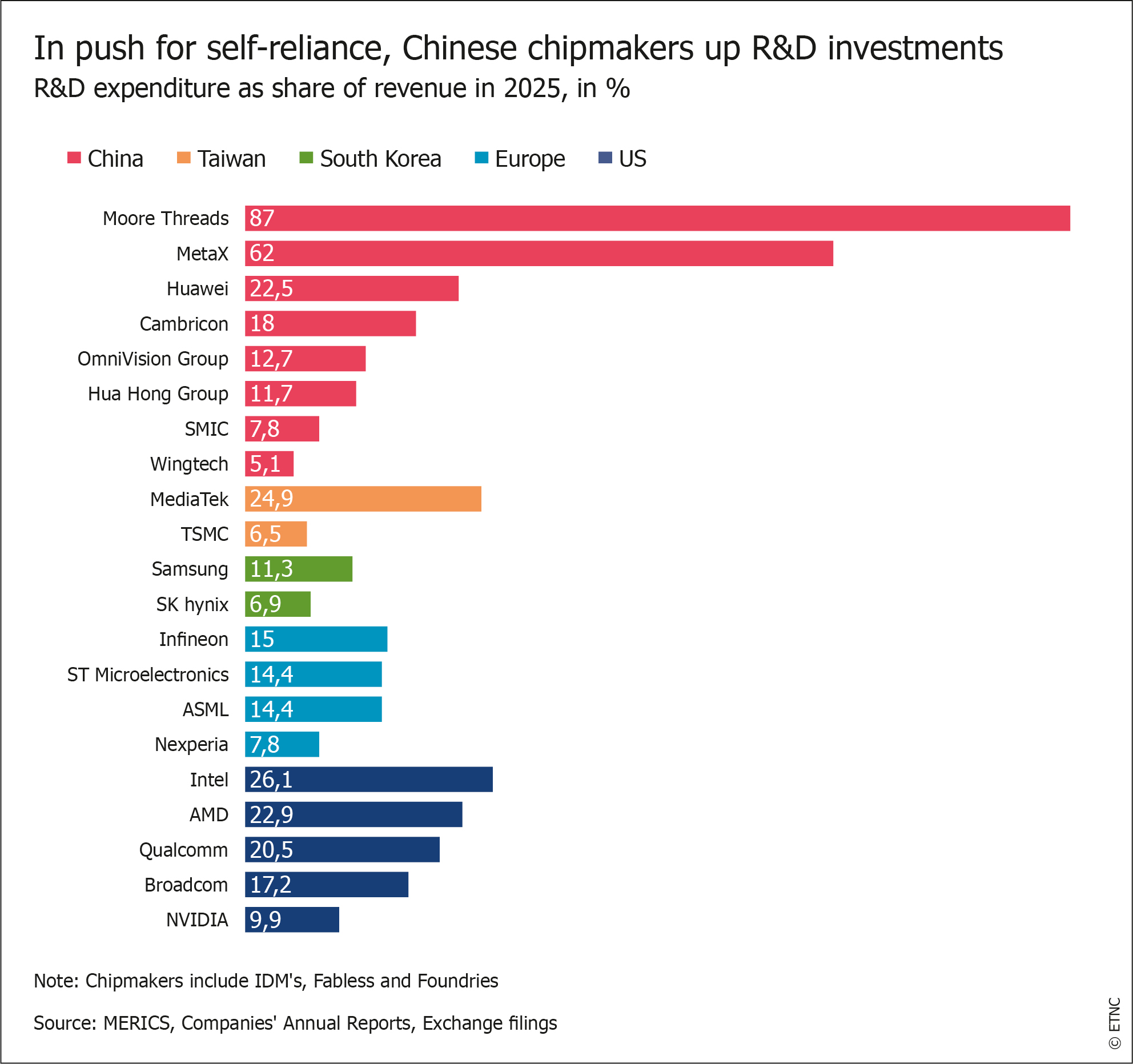

This trend is only poised to intensify given rising global demand for mature-node chips, coupled with China’s projected capacity expansions. The EU faces a projected annual sup-ply gap of 12.7 million wafers by 2030, with currently planned fab expansions expected to cover less than half.10 If downstream European industries manage to survive the ongoing “China shock”11 and thus continue driving chip demand (which is not a given), the shortfall in legacy nodes will be acutely felt. Meanwhile, Chinese companies have committed to doubling their capacity by 2030 (compared to the 2023 baseline).12 China is therefore set to dominate EU chip imports, while European chipmakers will also face growing pressure from their local competitors. The result is a mounting challenge to the bloc’s resilience and competitiveness.

Battery electric vehicles: Europe wants Chinese technology

Another example of China’s challenge to European technological competitiveness is the growing footprint of and demand for Chinese battery electric vehicles. Chinese players en-joy advantages stemming from the country’s massive economies of scale and state support to the industry, and their products are increasingly sophisticated too. This notably includes batteries, a critical technology field where Chinese firms, particularly Contemporary Amper-ex Technology Co. Ltd. (CATL), dominate major parts of the value chain. Today, China is the world’s leading producer of lithium-ion (Li-ion) batteries, with Chinese battery producers holding 65% of global production.13

As CATL and other companies are expanding in Europe and opening facilities to supply local automakers, the attractiveness of their investments for the European economy is obvious. To maximize the benefits, Brussels and some capitals are considering condition-ality requirements – including possible technology transfer requirements – for those invest-ments. This is not EU competence, however, as it is up to each member state government to negotiate greenfield investment deals. The Commission is now trying to promote har-monisation through guidance on FDI, non-price criteria for public procurement, as well as additional provisions included in the draft Industrial Accelerator Act.14 The goal is to ensure that competition for Chinese battery projects among capitals does not trigger a race to the bottom.

Transferring technology, unfortunately, is easier said than done. As mentioned previously, China’s government has shown both the willingness and the ability to restrict technolo-gy outflows.15 Indeed, several types of battery technology and components, as well as any associated intellectual property, are subject to PRC technology export controls.16 In July 2025, China’s Ministry of Commerce included fourth-generation lithium iron phos-phate (LFP) cathode technology, newer lithium manganese phosphate (LMFP) technology, as well as certain technologies for phosphate cathode raw material production, lithium extraction, and gallium extraction.17 By requiring that Chinese exporters obtain a license for overseas transfers, the government is proactively preventing foreign competition from emerging. As such, Chinese export controls are poised to further complicate EU industrial policy and de-risking plans.

Energy infrastructure: solar inverters expose cybersecurity concerns

The expansion of Chinese battery makers heralds the arrival of more PRC-origin tech-nologies in the European market, which has given rise to cybersecurity and data security concerns, too.18 Particularly when components end up in critical infrastructure, such as transportation or energy systems, vendor trustworthiness is paramount. However, one big lesson learnt from the patchworked implementation of the 2020 cybersecurity “toolbox” for 5G networks regards the difficulty of getting to a shared, EU-wide definition of political risk.19

This is largely due to a lack of political will. Existing cybersecurity regulations, notably the Cyber Resilience Act, Critical Entities Resilience Directive, and NIS2 Directive, do provide for the assessment of both technical and non-technical risk factors in the context of eval-uating critical ICT products, services, and systems being procured in the EU.20 Chinese vendors stand out for their risk profile due to their centrality on many ICT supply chains, coupled with the political and legal landscape in their home country, where the CCP is above the law, prosecutes a markedly offensive cyber policy, and limits the autonomy of economic actors. Although some member states have used such authorities, others have been wary of singling out specific vendors – in large part out of fear that doing so would jeopardise bilateral relations with China.

An illustration of this regulatory patchwork, Chinese solar inverters were banned in Lith-uania in 2023 but remain widely available elsewhere in the EU.21 Over 80% of inverters are sourced from China, with Huawei being the market leader, followed by other Chinese firms.22 Over 200 GW of European solar power capacity is estimated to be linked to in-verters made in China.23 Inverters, which connect power devices to the grid, must be ac-cessible remotely for updates and maintenance. Reports of undisclosed communication devices found in some Chinese solar inverters have triggered renewed concerns around potential sabotage or damage.24 Now, under the proposed recast of the EU Cybersecurity Act, the Commission would be empowered to designate and de facto restrict these or other products “where dependencies on a single or very limited number of suppliers could pose a significant security risk.”25

Recent policy adjustments: De-risking enters crucial implementation phase

These illustrate two key difficulties the EU is facing in translating its de-risking strategy into action. First, achieving greater technological autonomy entails choices that are both finan-cially and politically costly. Industrial and innovation policy in sectors like semiconductors and green technologies come with big price tags, and at a time when European citizens are being asked to spend more on the continent’s defence capabilities in the face of Russia’s aggression and the less reliable, more unpredictable US administration of Donald Trump. These conditions further limit the political will and cohesion required for member states to implement high-stakes policies that would reduce exposure to China’s value-chain dom-inance and willingness to weaponise its advantages. This is largely why good-on-paper initiatives such as the ReSourceEU Action Plan, the Net Zero Industry Act, or the proposed Industrial Accelerator Act face so many structural, political, and financial constraints.

The second difficulty lies in the multi-stakeholder nature of many technology and economic security policies, which require that the right structures, mechanisms, and incentives be in place. The dynamics in the semiconductor and automotive sectors capture the dilemma well: European businesses are still drawn to China’s innovation ecosystem and market due to the pace of innovation and digitalisation, even though the very self-reliance campaign that is fuelling localisation in China is also increasing dependencies and driving de-indus-trialisation in Europe. This situation explains why the December Communication places so much focus on getting industry on board – including as crucial providers of information and intelligence upon which to base risk assessments as well as the ensuing mitigation measures.

Outlook: Distrust in Chinese technology will stay despite EU-US tensions

Europeans increasingly perceive China as a major science and technology power whose development and policies involve high stakes for Europe. In a survey of 766 Europe-based China experts and observers conducted by MERICS, nearly 80% of respondents expected the country to make “major” or “very major” progress in AI in 2026, with more than half expressing the same views for semiconductors, biotechnology, and green technologies. At the same time, most respondents were either pessimistic or only slightly optimistic about the EU’s ability to reduce dependencies on the PRC and prosecute economic de-risking.26 The ongoing crisis of the transatlantic relationship will further complicate the implemen-tation of many China-related policies. Although Brussels is staying the course of the eco-nomic security strategy that the first von der Leyen Commission unveiled three years ago, Washington’s policies are absorbing much of member states’ bandwidth. Amid Trump’s tar-iffs, assault on European countries’ sovereignty and democracy, and transactional dealings with China and Russia, priorities in capitals have inevitably shifted. Importantly, Europeans are also rethinking their dependency on US chip designers and hyperscalers.

Once a partner in implementing important de-risking policies vis-à-vis China –sometimes by unilaterally pressuring Europeans to treat Chinese technology as a threat – the United States is now undermining the EU and its ability to act in global technology competition. European governments may be excused for scrambling to respond in kind to Chinese ex-port controls on critical inputs for their tech industries while the United States is coercing its allies.27 Similarly, restricting Chinese ICT vendors or strengthening export controls may seem ill-timed as Washington is making concessions to Beijing on the technology front.28

Still, it seems fair to say that Trump’s policies are making it more complicated and costlier for Europe to reduce its strategic vulnerabilities, but they will not fundamentally change member states’ collective risk assessment on China. With some exceptions, the risks stemming from deep technological interdependence with China are arguably recognised by most EU governments. However, conversations with officials in Brussels reveal an acute preoccupation regarding the bloc’s resolve, urgency, and ability to act swiftly to counter the PRC’s growing techno-industrial dominance.

- Endnotes

1 | European Commission (2026). “Horizon Europe.” https://research-and-innovation.ec.europa.eu/ funding/funding-opportunities/funding-programmes-and-open-calls/horizon-europe_en. Accessed: April 8, 2026; Fieldhouse, Rachel (2026). “Why Europe barred China from flagship Horizon research programmes.” Nature. February 16. https://www.nature.com/articles/d41586-026-00435-w. Accessed: April 8, 2026.

2 | Kleinhans, Jan-Peter and John Lee (2024). “Lithography: Is the EU’s Semiconductor Manufacturing Equipment a Strategic Chokepoint?” In: DPC Report; Rühlig, Tim (ed.). “Reverse Dependency: Making Europe’s Digital Technological Strengths Indispensable to China,” pp. 30 -43. Digital Power China (DPC). May 7. https://dgap.org/system/files/article_pdfs/DPC%20-%20GESAMT_Final.pdf. Accessed: April 9, 2026; Fedasiuk, Ryan (2026). “Europe Dominates AI’s Plumbing”. CEPA. February 27. https://cepa.org/article/europe-dominates-ais-plumbing/. Accessed: April 9, 2026.

3 | European Commission (2023). “European Economic Security Strategy.” Document 52023JC0020. June 20. https://eur-lex.europa.eu/legal-content/en/TXT/?uri=CELEX:52023JC0020. Accessed: April 8, 2026.

4 | European Commission and High Representative (2025). “Strengthening EU economic security.” December 3. https://circabc.europa.eu/ui/group/7fc51410-46a1-4871-8979-20cce8df0896/ library/777b1ecb-e7ce-4774-a92c-53f81e64ce76/details?open=true. Accessed: April 8, 2026.

5 | Government of the Netherlands (2025). “Letter to the Parliament on the invoked Goods Availability Act.” Minister of Economic Affairs. September 30. https://www.government.nl/documents/2025/10/14/letter-to-the-parliament-on-the-invoked-goods-availability-act. Accessed: April 9, 2026.

6 | Hijink, Mark (2025). “Nexperia in no-man’s-land: how a chip company became caught between two world powers.” NRC. December 30. https://www.nrc.nl/nieuws/2025/12/30/nexperia-in-no-mans-land-how-a-chip-company-became-caught-between-two-world-powers-a4916395. Accessed: April 8, 2026.

7 | Reuters (2025). “How the Nexperia chip crisis upended auto supply chains – again.” Reuters. November 24. https://www.reuters.com/business/autos-transportation/how-nexperia-chip-crisis-upended-auto-supply-chains-again-2025-11-24/. Accessed: April 8, 2026.

8 | Rühlig, Tim (2024). “Curbing China’s legacy chip clout - Reevaluating EU strategy.” EUISS Policy Brief. December 13. https://www.iss.europa.eu/publications/briefs/curbing-chinas-legacy-chip-clout-reevaluating-eu-strategy. Accessed: April 8, 2026.

9 | Grimm, Sunny (2025). “China’s mature chips to make up 28% of world production, creating oversupply — Western companies express concern for their survival.” Tom’s Hardware. February 26. https://www.tomshardware.com/tech-industry/chinas-mature-chips-to-make-up-28-percent-of-world-production-creating-oversupply-western-companies-express-concern-for-their-survival. Accessed: April 9, 2026.

10 | German Association of the Automotive Industry (2023). “Semiconductor crisis.” Position of the VDA. May. https://www.vda.de/dam/jcr:ed5b5fa5-96f8-4b86-bc2a-baa0dc19504c/Paper_Semi-conductor%20Crisis.pdf?mode=view. Accessed: April 9, 2026.

11 | Gunter, Jacob and Mikko Huotari (2025). “Shockwaves Made in China.” Internationale Politik Quarterly. October 20. https://ip-quarterly.com/en/shockwaves-made-china. Accessed: April 9, 2026.

12 | Triolo, Paul (2024). “Legacy Chip Overcapacity in China: Myth and Reality.” CSIS. April 30. https://www.csis.org/blogs/trustee-china-hand/legacy-chip-overcapacity-china-myth-and-reality. Accessed: April 9, 2026.

13 | Jugé, Marie et al. (2025). “Transatlantic clean investment monitor 4: electric vehicles.” Bruegel. June 5. https://www.bruegel.org/analysis/transatlantic-clean-investment-monitor-4-electric-vehicles. Accessed: April 9, 2026.

14 | Council of the European Union (2026). “Proposal for a Regulation of the European Parliament and of the Council on the screening of foreign investments in the Union and repealing Regulation.” Document 2024/0017 (COD). February 10. https://data.consilium.europa.eu/doc/document/ ST-6254-2026-INIT/en/pdf. Accessed: April 9, 2026; European Commission (n.d.) “The Net-Zero Industry Act.” https://single-market-economy.ec.europa.eu/industry/sustainability/net-zero-indus-try-act_en. Accessed: April 9, 2026; European Commission (2026). “Industrial Accelerator Act.” March 4. https://single-market-economy.ec.europa.eu/publications/industrial-accelerator-act_en. Accessed: April 9, 2026.

15 | Arcesati, Rebecca, François Chimits, and Antonia Hmaidi (2024). “Keeping value chains at home.” MERICS Report. August 8. https://merics.org/en/report/keeping-value-chains-home. Accessed: April 9, 2026.

16 | Laha, Michael (2025). “Chinese Export Controls on Cathode Technology: The EU Must Increase Insight into Supply Chains.” DGAP Memo No. 54. December 18. https://dgap.org/en/research/publications/chinese-export-controls-cathode-technology-eu-must-increase-insight-into. Accessed: April 9, 2026.

17 | Ministry of Commerce of the People’s Republic of China 中华人民共和国商务部 (2025). “商务部 科 技部公告2025年第28号 关于调整发布《中国禁止出口限制出口技术目录》的公告.” (Announcement on the Revision and Release of the “Catalogue of Technologies Prohibited or Restricted for Export from China”). July 15. https://fms.mofcom.gov.cn/zcfg/jsjckzcfg/art/2025/art_ba35a101c22c4f6e844f749cb0a98552.html. Accessed: April 9, 2026.

18 | European Commission (2026). “EU launches new toolbox to strengthen ICT supply chain security.” February 13. https://ec.europa.eu/commission/presscorner/detail/en/mex_26_411. Accessed: April 9, 2026.

19 | Clark, Sam and Mathieu Pollet (2026). “EU’s Huawei hardliners get top court backing.” Politico. March 19. https://www.politico.eu/article/eu-huawei-hardliners-get-top-court-backing/. Accessed: April 9, 2026.

20 | European Commission (2025). “The Cyber Resilience Act - Summary of the legislative text.” December 3. https://digital-strategy.ec.europa.eu/en/policies/cra-summary. Accessed: April 8, 2026; European Parliament and Council of the EU (2022). “Critical Entities Resilience Directive.” Document 32022L2557. December 27. https://eur-lex.europa.eu/eli/dir/2022/2557/oj/eng. Accessed: April 8, 2026; European Parliament and Council of the EU (2022). “Directive (EU) 2022/2555.” Document 02022L2555-20221227. December 14. https://eur-lex.europa.eu/eli/dir/2022/2555. Accessed: April 8, 2026.

21 | Jowett, Patrick (2024). “Lithuania bans remote Chinese access to solar, wind, storage devic-es.” PV Magazine. November 18. https://www.pv-magazine.com/2024/11/18/lithuania-bans-remote-chinese-access-to-solar-wind-storage-devices/. Accessed: April 8, 2026.

22 | Jowett, Patrick (2025). “EU security doctrine highlights high-risk dependency on Chinese solar inverters.” PV Magazine. December 16. https://www.pv-magazine.com/2025/12/16/eu-security-doctrine-highlights-high-risk-dependency-on-chinese-solar-inverters/. Accessed: April 8, 2026.

23 | Gehrke, Tobias (2025). “How China could crash Europe’s energy grid and what the EU can do about it.” European Council on Foreign Relations. November 20. https://ecfr.eu/article/how-china-could-crash-europes-energy-grid-and-what-the-eu-can-do-about-it/. Accessed: April 8, 2026.

24 | Mcfarlane, Sarah (2025). “Rogue communication devices found in Chinese solar power inverters.” Reuters. May 14. https://www.reuters.com/sustainability/climate-energy/ghost-machine-rogue-communication-devices-found-chinese-inverters-2025-05-14/. Accessed: April 9, 2026.

25 | Eudebates.tv (2026). “We Must Identify the Risks: EU Moves to Restrict High-Risk Tech Suppliers!” Youtube. January 20. https://www.youtube.com/watch?v=qVt7wNTdJAY. Accessed: April 9, 2026.

26 | Soong, Claus and Niklas Hintermayer (2025). “MERICS China Forecast 2026: High expectations for Chinese innovation, low expectations for relations with US and EU.” MERICS. November 26. https://merics.org/en/comment/merics-china-forecast-2026-high-expectations-chinese-innovation-low-expectations-relations. Accessed: April 8, 2026.

27 | Poitiers, Niclas (2026). “What can Europe learn from Trump’s Greenland tariff threats?” Bruegel. January 26. https://www.bruegel.org/newsletter/what-can-europe-learn-trumps-greenland-tariff-threats. Accessed: April 9, 2026; Gerhke Tobias and Nina Schmelzer (2026). “Beijing hold’em: European cards against Chinese coercion.” European Council on Foreign Relations Policy Brief. March 31. https://ecfr.eu/publication/beijing-holdem-european-cards-against-chinese-coercion/.

Accessed: April 9, 2026.28 | Sevastopulo, Demetri and Michael Acton (2025). ”Nvidia can sell H200 AI chips to China, Donald Trump says.“ Reuters. December 9. https://www.ft.com/content/ac63139d-5143-4aed-a1e4-980a06551b51?syn-25a6b1a6=1. Accessed: March 31, 2026.

Content