picture alliance/AP Photo | Andy Wong

Comment

Bond defaults: Beijing weeds out state-owned enterprises

The facts: A series of bond defaults of state-owned enterprises (SOE) has cast a shadow on China’s economic recovery from the Covid-19 crisis. On November 17, Tsinghua Unigroup, a semiconductor company and key player in China’s efforts to upgrade its industry, became the latest to join the list, defaulting on a CNY 1.3 billion bond. The spook began in October when Huachen Automotive, owned by the provincial government of Liaoning, defaulted on a bond payment. Yongcheng Coal and Electricity, based in Henan Province, also defaulted on a CNY 1 billion bond that was only issued in October.

The People’s Bank of China (PBOC) injected CNY 800 billion into credit markets on November 16 to sooth investors’ nerves, but some fundamentals are changing. The PBOC’s WeChat account resurfaced an older speech from Governor Yi Gang in which he stated that investors should bear the risks of their investments. The influential Financial Stability and Development Committee agreed to pursue a zero-tolerance strategy with regard to debt evasion.

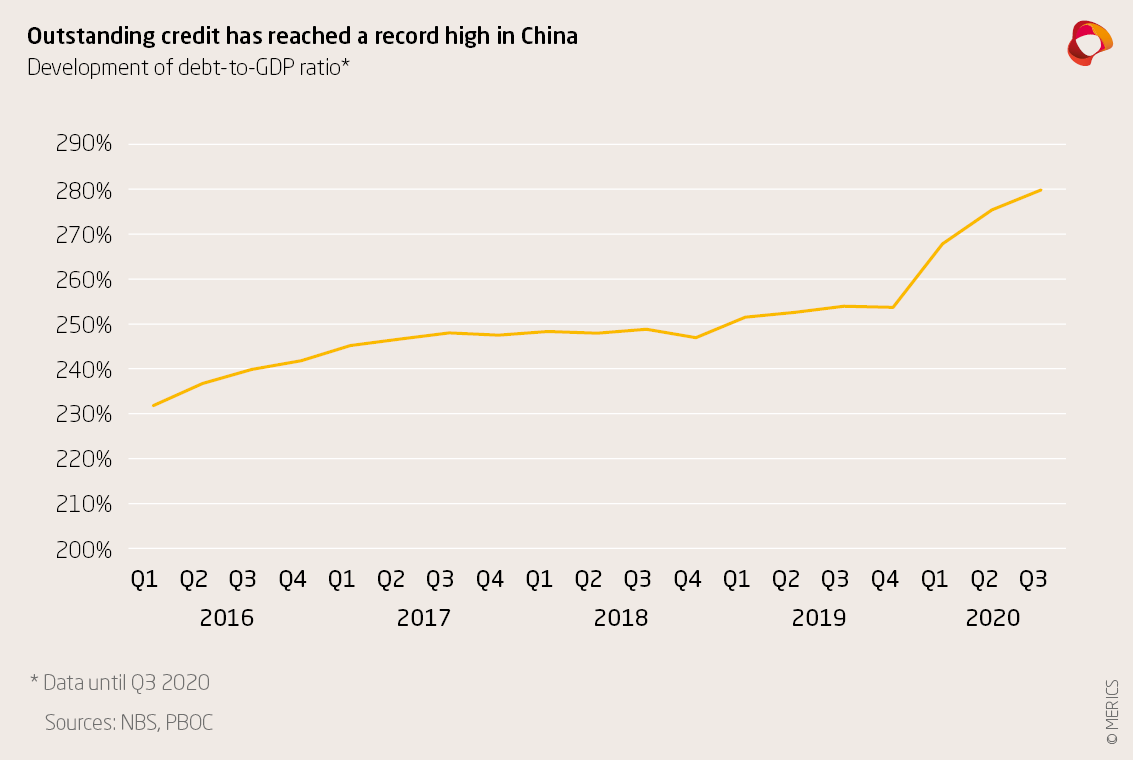

What to watch: Taking into account China’s frail debt markets and the currently weak world economy, a series of defaults could increase risks in China’s already troubled financial market. Beneath China’s swift coronavirus recovery, not everything is rosy. Chinese companies’ ability to service debt is weak: the year-to-date industrial profits are down by 4.9 percent and the producer price index fell by 2.1 percent indicating deflation. Q3 data indicates how much the GDP growth heavily dependent on credit growth: nominal GDP grew at 1.4 percent while outstanding credit jumped by 13.5 percent, leading to a 36 percentage-point increase in the debt-to-GDP ratio since January. It has now reached a record high of 280 percent and is set to expand even more.

MERICS analysis: Beijing is on a mission to induce market discipline into China’s corporate debt market. Undermining investors’ faith in implicit guarantees that troubled SOEs will be bailed out is part of its strategy. It appears that Beijing is signaling it is ready to pull the plug. However, a continued series of defaults could undermine economic recovery and lead to capital outflow pressure, a scenario that policymakers are eager to avoid. So, it’s possible Beijing will step in, should defaulting get out of hand.

Media coverage and sources:

- Reuters: China’s Tsinghua Unigroup defaults on bonds

- Economist: China’s bond market is jolted by some surprising defaults

- China Banking News: Ten state-owned enterprises with USB 15.7 billion in outstanding bonds default

- Wall Street Journal: Bond upsets rattle Chinese credit market

- SCMP: Chinese authorities warn bond issuers they can’t run away

- Rhodium Group: Credibility in the balance

This article first appeared in the November 26, 2020 issue of MERICS China Briefing.