Tracker

China Global Competition Tracker

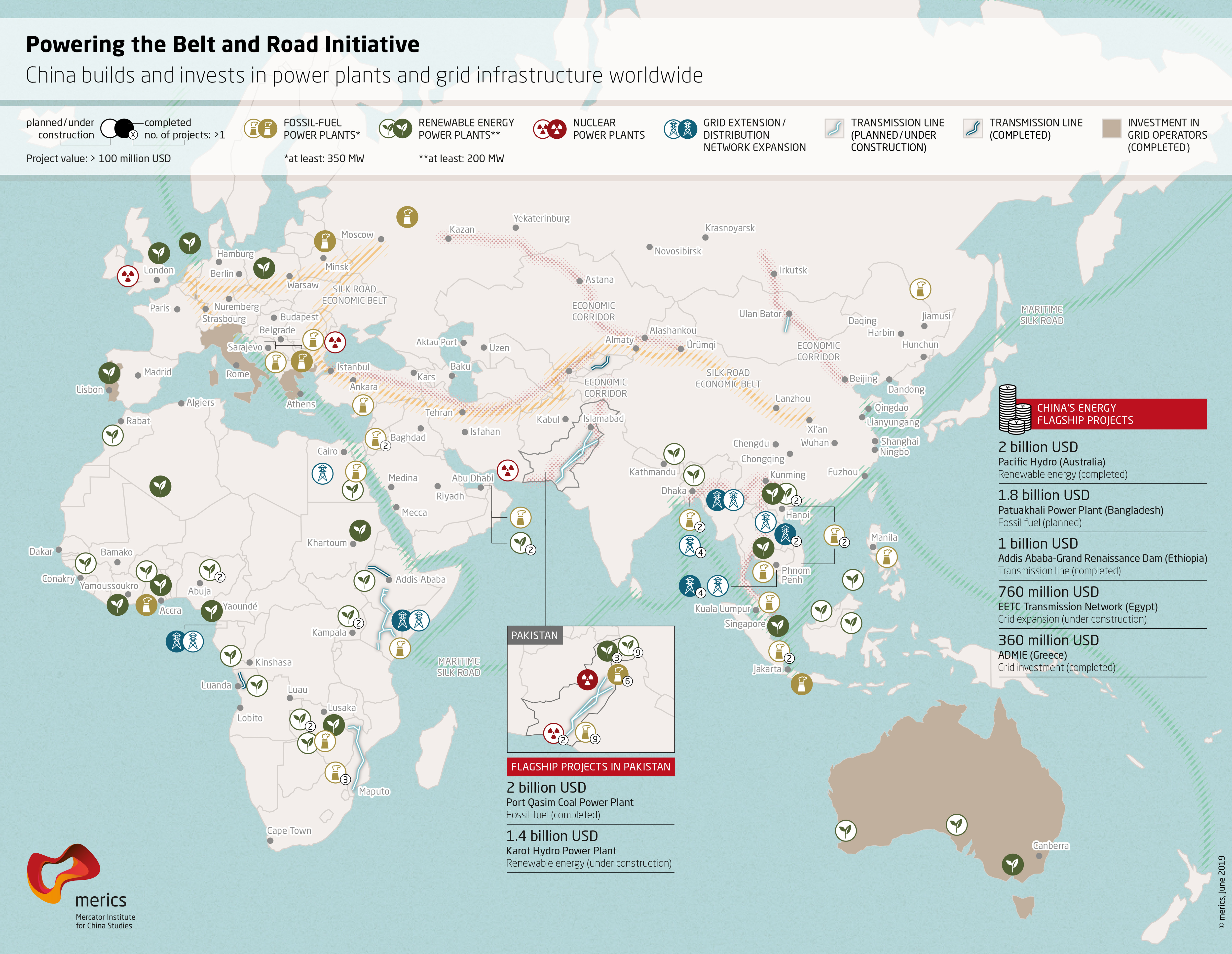

Powering the Belt and Road

The Chinese government prominently featured energy-infrastructure co-operation when it outlined the priorities for the Belt and Road Initiative (BRI) in March 2015. In a broad sweep, Beijing noted the extraction of energy resources, power generation, upgrading power grids, and building of electricity transmission lines in the foundational policy paper ”Vision and Actions on Jointly Building the Silk Road Economic Belt and 21st-Century Maritime Silk Road”. But the document did not say how these goals would be achieved and who would contribute what. Later policy papers on maritime cooperation under the BRI (2017) and on the Arctic (2018) had a greater focus on renewable energy generation, but also said nothing about China’s plans for implementation.

The MERICS BRI Database has allowed us to identify projects related to renewable energy, fossil fuel and nuclear power projects; grid investments and upgrades; as well as key domestic and cross-border transmission-line projects (see map below). This has produced four insights about BRI-related projects in energy generation and distribution. Firstly, investment in power plants and grids dominates China’s spending on BRI-related infrastructure. Secondly, China is encouraging its energy companies to seek contracts abroad without necessarily prioritizing any sector - Beijing is neither leading a “green” revolution nor a fossil-fuel revival, but rather playing both sides. Thirdly, China’s energy projects are geographically diversified - Latin America is in the lead in terms of volume of completed investments (mostly into renewables and energy distribution), while Southeast Asia boasts the highest number of projects (mostly involving coal). Fourthly, China’s initial focus on energy projects creates the preconditions for the next phase of the BRI: industrial buildup and new China-centered supply chains.

The BRI has been more about investing in energy than anything else

The MERICS BRI Database suggests that about two thirds of Chinese spending on completed BRI projects went into the energy sector, and already amounts to more than 50 billion USD. The rest was used for transport projects (more than 15 billion USD), and the “digital silk road” (more than 10 billion USD). The emphasis on the energy sector also holds for projects currently under construction. They will get a similar volume of Chinese FDI and loans to projects already completed. The timetables for newer projects vary greatly, which means that some should go onstream as early as this year, while others will go live only in the mid-2020s.

China is pushing its companies to grab market share in all energy sectors

The BRI policy documents mentioned above put a premium on cooperating in the field of renewable energy with countries in Africa and the Arctic region – they mention the word “coal” only once. Indeed, renewable energy power-plants lead the pack of completed, Chinese-funded energy projects with a total investment volume in excess of 20 billion USD. But close behind are both fossil-fuel energy generation projects (ca. 15 billion USD) and grid investments (ca. 12 billion USD). Indeed, more coal-fired than renewable power plants are being financed by China, even if overall investment in renewables is higher as a result of several huge hydropower projects.

Beijing in particular wants to help coal-sector companies to make up for an order slump in a domestic market becoming more environmentally conscious. Honoring its commitments at the Paris Climate Conference, the Chinese government wants to cut domestic emissions by transitioning to clean energy sources, including hydropower, although it is also moving to boost nuclear power and natural-gas imports. As a result, many domestic coal-fired power-plant projects have been cancelled. The Chinese government and state-controlled banks are giving companies affected by these moves financial and political support to seek new contracts in other countries.

Yet the government wants Chinese energy companies in all areas of power generation and distribution to increase their international market share and become global champions. The vast scale of the Chinese market has already allowed companies in areas such as hydropower production and grid operation to grow to unprecedented sizes and gather valuable experience and expertise. Often, Chinese investors and contractors can also draw on world-class Chinese suppliers such as solar-panel makers. For Chinese companies desperately looking for new contracts, geography is no issue.

China has diversified its BRI-projects geographically

Most BRI-related energy projects have clustered in developing and emerging markets, in which China can more easily avoid tenders and secure contracts directly for its energy companies. But Chinese entities have also successfully gained footholds in the energy markets of advanced economies. These promise more secure investments and may be marketed as demonstrating Chinese companies’ financial firepower, technological prowess and trustworthiness. Most prominently, Chinese companies have invested heavily in Australian grid infrastructure and renewables (e.g. SP Ausnet, SPI (Australia) Assets, Pacific Hydro). And they have successfully invested in Southern European grids and Western European wind power (e.g. EDP (Portugal), ADMIE (Greece), Meerwind (Germany), Dudgeon (UK)).

Chinese FDI and loans for BRI-related energy projects are highly diversified geographically, with numbers exceeding 4 billion USD on every continent. The Americas are clearly ahead in funding volume as a result of a Chinese investment spree that started in 2016. Projects focus on Latin American hydropower and grid infrastructure, and most are above the billion-dollar mark. Brazil currently occupies the top spot in Chinese-funded energy generation and distribution.

But the largest number of projects, albeit often smaller in size, is clustered in Southeast Asia. In the region neighboring China, Chinese companies have been involved in two large power-generation buildups - a fossil fuel-powered one in Indonesia, and a hydropower surge along the Mekong River in Laos and Cambodia. Some of these countries will likely see Chinese-backed power generation outstrip domestic demand. This incentivizes future Chinese investments in cross-border transmission lines. They can be built onto grid upgrades that often have already happened and promise additional revenue streams in the form of electricity exports.

Most grid investments, upgrades, and extensions do not yet involve cross-border elements, and are geographically widely dispersed. While the Chinese leadership has supported plans to later expand into a (China-driven) global energy grid, these are only in an initial phase, and do not appear as the primary motivation behind projects in this sector.

Instead, projects in both energy production and distribution should be seen as a necessary precondition for the next phase of the BRI: a global industrial buildup and the establishment of China-centered industrial supply chains. The “Long-Term Plan” for the China-Pakistan Economic Corridor mentions this goal on a regional level, but it appears to hold true much more broadly. China is putting in place the power supply its companies will need, while securing market share and key assets in the energy sector.

For the rest of the world, China’s BRI energy drive has two main implications. Firstly, many developing countries will gain access to new power supply and distribution much more quickly than previously forecast. China is indeed creating a potential foundation for new industrial centers in many countries. These could form new China-bound supply chains and might alter competition in power-intensive sectors.

It remains far from certain, however, whether high project costs, new debts incurred, and long-term high-price electricity contracts agreed to please Chinese power-sector investors will leave host countries with any net economic benefit. In the end, this could undermine China’s industrial cooperation plans, if target countries are no longer convinced these are in their best interest.

Secondly, energy companies from Europe and elsewhere face strong competition from Chinese giants willing to accept more risk and less profitable conditions for the sake of securing market share. The Chinese government supports its (mostly state-owned) energy companies and wants to turn them into global champions. Eventually, they should be strong enough to protect their market positions by themselves. At the same time, they would be able to accommodate Beijing’s industrial strategy by handing more contracts to Chinese suppliers. Power-generation equipment is one of the ten key sectors for which “Made in China 2025” sets global market-share targets. In this way the challenge to European industry from BRI-bolstered Chinese competitors could spread further to suppliers and sub-contractors, who have thus far been able to profit from the initiative.

Autor(en)

Ehemaliger Wissenschaftlicher Mitarbeiter

Ehemaliger Research Fellow

Autor(en)

Ehemaliger Wissenschaftlicher Mitarbeiter

Ehemaliger Research Fellow