MERICS China Economic Indicators

MERICS China Economic Indicators

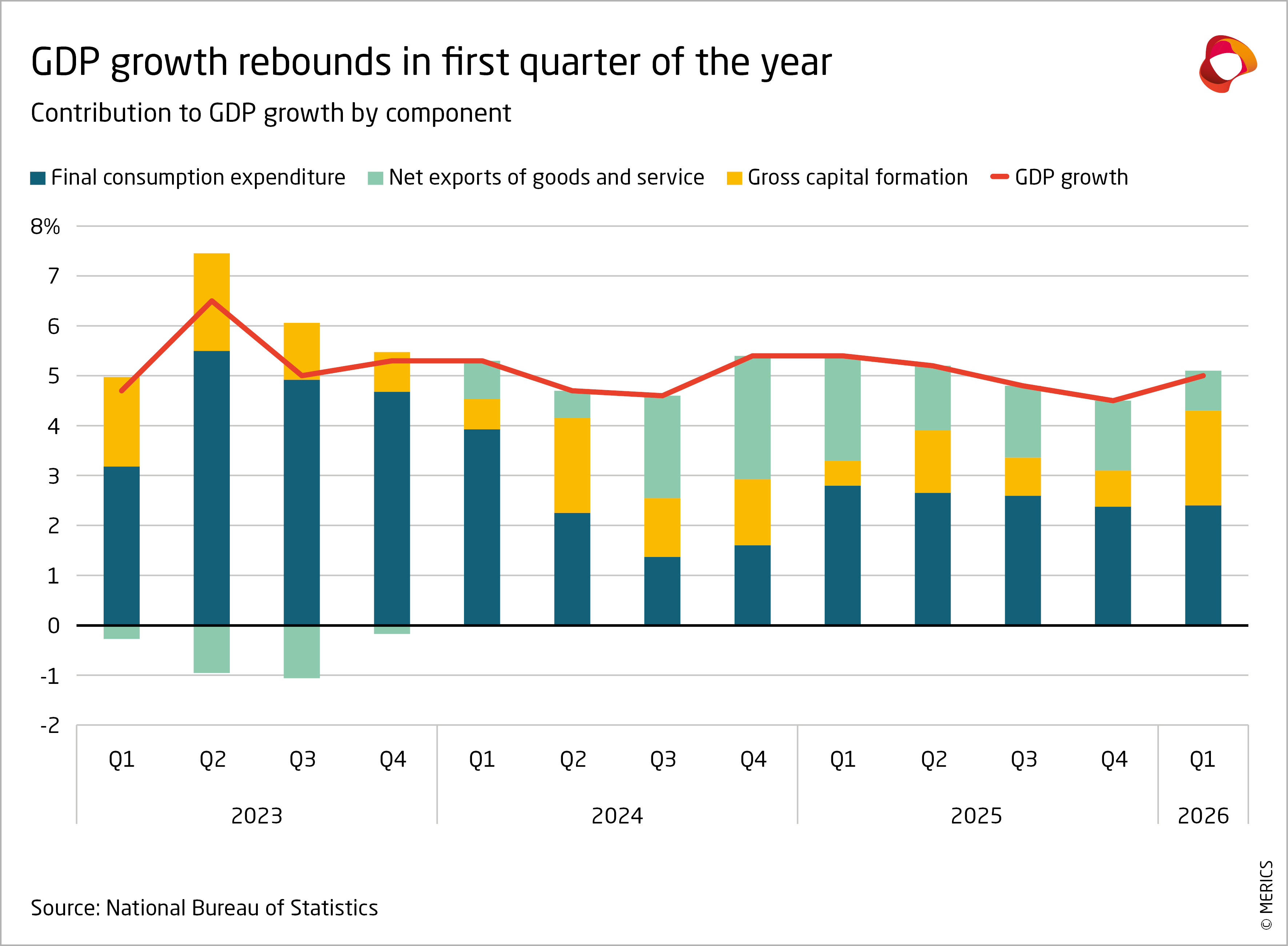

MERICS China Economic Indicators is our quarterly analysis of China’s economic data. The MERICS Economy and Industry team provides updates on the latest macroeconomic trends and their impact on Europe. The findings are presented on a dashboard in interactive charts and explained in concise texts. In-depth analyses put a spotlight on the most important developments.

MERICS Members have privileged access to this publication. Learn more about the Membership program here.

Graphs

Download as PDF

Analyses

Previous editions

Authors

Senior Analyst

Head of Program

Analyst

Visiting Fellow