picture alliance / CFOTO | CFOTO

Content

MERICS Briefs

MERICS Europe China 360°

EU Industrial Accelerator Act + Critical materials + Platform exports

ANALYSIS

The EU's Industrial Accelerator Act won't stave off China's unfair trade practices

By Esther Goreichy

The EU is sharpening its industrial policy playbook with a new Industrial Accelerator Act (IAA), presented in March. The aim is to preserve its core industries threatened by unfair competition from China and to facilitate technology transfer in sectors where it lags behind. While the IAA fills important gaps in the EU’s playbook, the current proposal contains loopholes that could undermine its capacity to protect European industries. Likewise, the package does not task the EU with drastically sharpening its trade policy.

As China is increasingly offloading excess goods abroad due to manufacturing overcapacity, the IAA aims to limit access to public funding for Chinese exporters unless they localize production in Europe or with its trading partners. However, the new requirements for foreign companies can be waived in cases where costs would be significantly higher (between 25 and 30 percent) should non-EU or partner countries’ firms be excluded – or if they would cause delays or there were no viable alternatives. Given extensive state subsidies and currency devaluation in China, such thresholds are likely to be met in a number of sectors. For example, Chinese wind turbines are already 30 percent cheaper than in Europe. Without complementary measures to address these distortions, the IAA may even incentivize anticompetitive practices from China.

Despite its more forward-looking approach, the IAA fails to include future sectors

The measures allow the EU to assume a more forceful posture in preserving EU industrial capacity in strategic sectors. Indeed, low-carbon and “Made in EU and partner countries” requirements will be introduced for public procurement and public support schemes for selected strategic sectors. These include steel, cement, aluminum, electric or hybrid vehicles, and net-zero technologies (such as batteries, solar photovoltaics, heat pumps, and wind power systems), with a possible extension to chemicals. But while the IAA is a good start, it may not go far enough to protect EU industries against China’s subsidization of industries that are set to produce the next wave of overcapacity.

China’s 15th Five-Year Plan, for instance, already points to those sectors. The EU is likely to face overcapacity pressure in areas like next-gen IT, new energy sources, robotics, biomedicine, aerospace, etc., which are not included in the IAA (semiconductors, cloud computing, cybersecurity, artificial intelligence are also not included). Although it contains a review clause after three years with a possible extension to additional sectors such as shipbuilding and rail rolling stock, the IAA does not provide clear indications on how such sectors will be selected.

FDI conditions are innovative but expansion to countries outside EU poses risks

The IAA introduces conditions for foreign direct investment (FDI) in sectors where the EU lags behind China. This conditionality, which applies to investors from non-partner countries holding over 40 percent of global manufacturing capacity, clearly targets China. Investments above EUR 100 million will require compliance with at least four of six value-added criteria, such as limits on ownership, joint ventures with EU partners, intellectual property sharing, minimum research and development (R&D) spending in the EU, and commitments to local sourcing and workforce integration. A requirement that at least 50 percent of the workforce be EU-based will apply in all cases.

Beyond addressing a long-discussed policy gap, the FDI measure offers several advantages. Conditioning access to the EU internal market encourages Chinese firms to engage in technology transfer, while EU-wide rules help prevent competition between member states in attracting foreign investment.

It applies to around 25 to 30 countries outside the EU engaged in bilateral trade agreements or in the WTO Government Procurement Agreement with the EU. It enhances long-term planning security for European producers, allowing them to invest without fear of unfair competition from subsidized Chinese firms. However, the expansion to countries outside the EU also increases the risk of circumvention, as Chinese firms may invest in these countries to gain access to EU public procurement while avoiding the new FDI conditionality measure.

Long-term, reliable commitment to EU objectives is key

China has already voiced strong opposition to the IAA, describing it as protectionist and discriminatory. Chinese authorities and business representatives argue that it will undermine WTO principles, such as most-favored-nation treatment, and disrupt global supply chains, leading to higher costs. The Ministry of Foreign Affairs spelled out “Three oppositions,” rejecting forced technology transfers, interference in business operations, and discriminatory practices.

As the European Parliament and Council negotiate the IAA, it will be important to remember that a meaningful reorientation of investment requires that both European and foreign firms can rely on the EU’s long-term commitment to its objectives. This means resisting pressures to dilute or diminish ambitions even in the face of cyclical constraints, such as the energy crisis, or external forces.

Read more:

- European Commission: Industrial accelerator Act

- Chatham House: ‘European preference’ signals a wider change of EU doctrine

- Kiel Institute: Ambition Without Precision: Why the Industrial Accelerator Act Falls Short

UPDATE

Europe is running out of time to cut its dependency on China for critical materials

By Altynay Junusova

Europe must move faster to build its own supply of critical minerals or it may fail to secure supplies it needs for defense, the clean energy transition, and economic competitiveness. The EU has recently shifted to viewing critical minerals as belonging to its strategic resources, but progress has been slow. In December, Brussels adopted the RESourceEU action plan to secure critical raw materials, but three months later, results have yet to materialize. Many of the most ambitious measures, including a financing hub and a critical raw materials center, are still in the early stages of implementation. These efforts are not enough to match the scale and urgency of the challenge.

Europe is working on plans to build alternative supply chains and reshore some mining and processing capacity at home. But the target of reducing dependence in batteries, rare earths, and defense-related materials by up to 50 percent by 2029 will be a difficult reach. At this rate, substantially lower reliance on China is unlikely before the 2030s. In the meantime, European industry will remain exposed to Beijing’s leverage. This challenge is unfolding as political attention in Brussels shifts toward the anticipated energy crisis and surge in inflation, distracting from the critical materials issue – even though the stakes are just as high.

Beijing has only gained a firmer grip on global supply

Over the past 16 years, Beijing has shown a willingness to leverage its near-monopoly over strategic resources in pursuit of geopolitical goals and to take steps to maintain that privileged position. Europe should, therefore, expect China to respond to any efforts to cut dependencies by tightening its grip on supply chains.

One year after imposing export controls on rare earths, Beijing has now issued supply chain security measures as part of an effort to push back against what it sees as growing Western protectionism. These new measures elevate supply chain oversight to the highest levels of government and expand control over critical supply chains, including raw materials. In practice, this gives Beijing a means to investigate and penalize foreign companies that are trying to reduce reliance on Chinese suppliers. Should tensions with Europe escalate, Beijing could plausibly cut off or continue to suspend exports of critical minerals. Its export controls on rare earths announced in October and suspended until November, for example, have yet to take effect. This creates uncertainty for European companies.

In fact, in most cases, China doesn’t even need to cut off supply to turn up the pressure. Delays, licensing requirements, and targeted restrictions are often more than enough, such as with its export controls on gallium and germanium, which, by 2025, had triggered price rises as high as 360-400 percent in Europe.

Beijing’s deployment of export controls for political purposes is a credible threat. In recent months, it has punished Japan by targeting rare earth elements, permanent magnets and other critical minerals with civilian and military dual use applications. Despite more than a decade of efforts to build supply resilience, Japan still relies on China for around 60-70 percent of its rare earth imports, down from 90 percent 16 years ago. These measures have reduced dependence, but not risk.

Takeaways for the EU

- Europe lags far behind EU plans to build up its own supply of critical minerals. The implementation of ambitious measures, such as a financing hub and a critical raw materials center, is still in early stages.

- This makes it very difficult to reduce dependencies on China in batteries, rare earths, and defense-related materials by up to 50 percent by 2029 as planned.

- Beijing will continue to leverage its advantage in critical materials, forcing Europe to the bargaining table on issues it deems important. Maintaining focus on this high-stakes topic, even in the face of other immediate, emerging crises, is key.

- Beijing’s new supply chain measures allow it to penalize foreign companies attempting to reduce reliance on Chinese suppliers. Beijing could retaliate by cutting off or continuing to suspend exports of critical minerals. But this may not even be necessary, as it can also use delays, licensing requirements, and targeted restrictions to turn up the pressure.

- China dominates refining, and Europe’s processing capacity is much diminished. And regardless of its diversification in sourcing raw materials, much of the value chain remains tied to China.

- All is not lost: If Europe can speed up implementation, it does have the knowhow to rebuild mining, refining and recycling, alongside its industrial base. And it has partners – for example, in Japan and Australia.

Read more:

- European Commission: RESourceEU Action Plan

- European Commission: Commission launches platform to aggregate demand of raw materials and boost diversification - Internal Market, Industry, Entrepreneurship and SMEs

- European Court of Auditor: EU risks running short of raw materials for renewables

- European Union Chamber of Commerce in China: Exporting Control - China’s new strategic toolkit

- China’s State Council: Regulations on industrial, supply chain security (CN)

EUROPE-CHINA DIPLOMATIC TRACKER

- European leaders continued to push for a recalibration of their relationship with China during visits in February and April. Although differing in the tone of their rhetoric and length of visits, German Chancellor Friedrich Merz and Spanish Prime Minister Pedro Sánchez echoed similar underlying messages: Europe seeks economic engagement and investments from China but rejects the deepening structural asymmetries, calling trade dynamics “unsustainable.”

- Merz’s February trip culminated in a pledge to relaunch German-Chinese government consultations, further bilateral dialogue on the energy transformation and climate, and the resumption of the German-Chinese Dialogue Forum. Berlin used the visit to clearly signal its concerns on trade frictions and imbalances, even as Merz pointed to concrete business wins such as China’s order for 120 additional Airbus aircraft.

- During his April visit, Sánchez paired calls for “balanced and reciprocal” trade with an active pitch for Chinese investment in higher-value sectors, including digital and AI-related projects. The key outcomes of the trip included the creation of a new Spain-China Diplomatic Strategic Dialogue and the signing of 19 new cooperation documents covering trade and investment promotion, sustainable transport and infrastructure, as well as collaboration on science and biodiversity. The visit also produced new agreements to expand Spanish agrifood exports and included meetings with 36 Chinese business leaders such as Xiaomi’s Lei Jun. Sánchez also voiced support for Beijing’s involvement in stabilizing the crisis in the Middle East.

- Beijing’s readouts from the visits, however, remain consistent with the usual calibrated charm offensive and targeted commercial offers, but limited willingness to address European leaders’ fundamental concerns. China continued to pay lip service to European strategic autonomy, attempting to put a positive spin on the relationship and delay confronting structural tensions.

- The EU and China also stepped up diplomatic contacts over the Iran war. Chinese Foreign Minister Wang Yi spoke with EU High Representative Kaja Kallas and the German and French foreign ministers. These exchanges point to a shared interest in de-escalation and reopening the Strait of Hormuz, but so far remain consultative and have not signaled a specific joint initiative that might include working-level structures.

It is noteworthy that Europe and Beijing have in the past joined forces on Iran nuclear issues. After US President Donald Trump withdrew from the long-negotiated multinational Iranian nuclear deal (JCPOA) in 2018, the EU and China pledged to salvage the agreement. But coordination to deescalate the current conflict would be much more challenging in view of the potential impact on transatlantic relations. - The European Parliament resumed high-level engagement with China, sending its first delegation in eight years. Members of the Internal Market and Consumer Protection (IMCO) Committee visited Beijing and Shanghai from March 31 to April 2, focusing on competition in e-commerce, particularly the surge in small-parcel trade. Discussions covered EU digital market rules, customs practices, and concerns over a level playing field and involved major platforms such as Alibaba, Shein and Temu. Representatives from the National People’s Congress, the State Administration for Market Regulation, and China Customs attended.

The visit precedes a follow-up mission in late May by the EP’s Delegation for Relations with the PRC, led by MEP Engin Eroglu. Beijing and potentially Wuhan are on the itinerary.

These exchanges reflect a gradual thaw in EU-China parliamentary relations that Beijing has sought since spring 2025, including through removal – though not formally announced – of sanctions on sitting MEPs and renewed contacts with European Parliament President Roberta Metsola’s office.

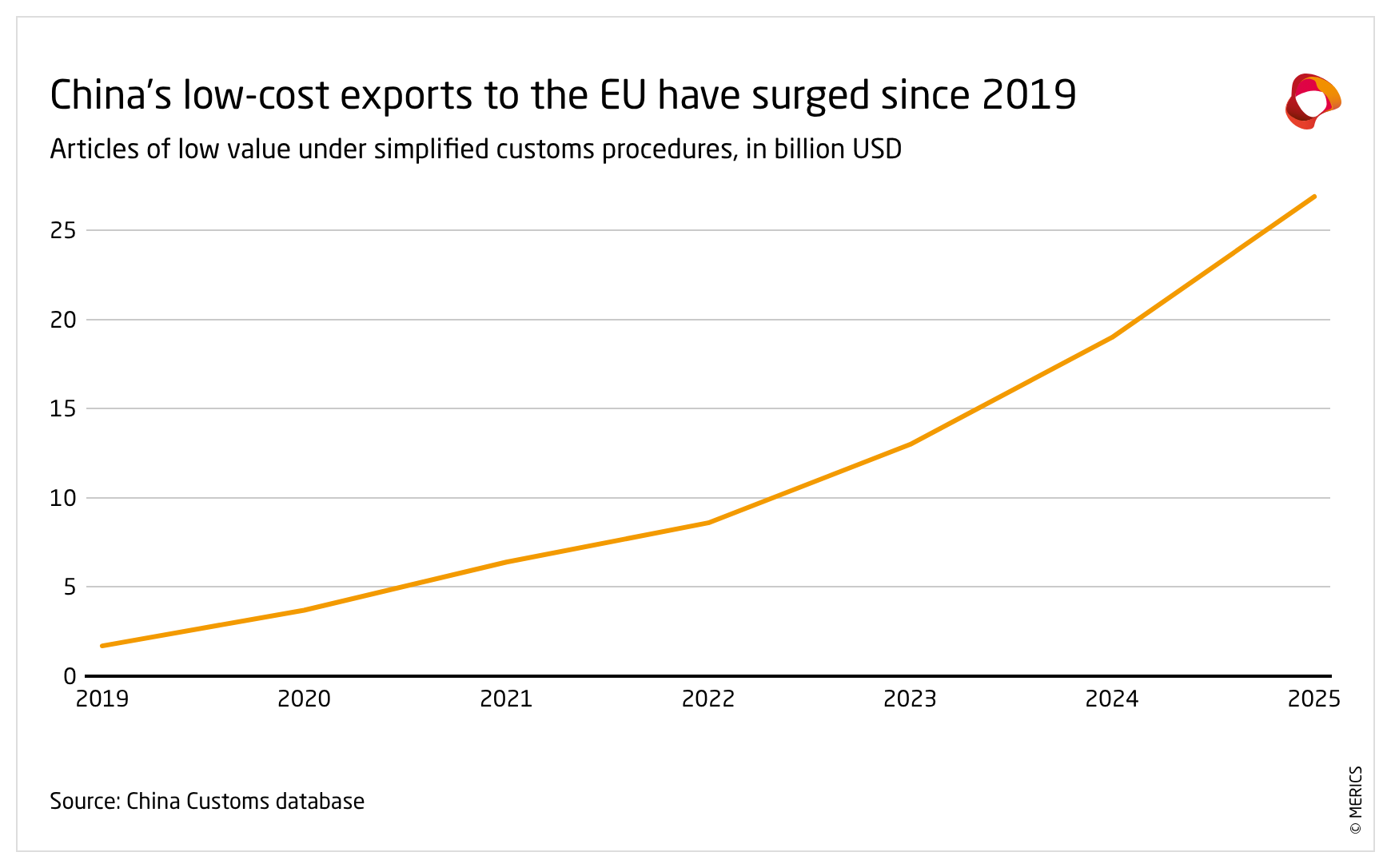

SOAPBOX MERICS DATA HIGHLIGHT

Chinese online platform exports to the EU

| The Soapbox-MERICS Data Highlight offers visualizations of EU-China economic relations. In this issue, MERICS Senior Associate Fellow Rafael Jimenez Buendía, author of the weekly China trade newsletter “Soapbox”, zooms in on the latest developments with regard to European tariffs on electric vehicles made in China. |

The EU is moving to address a huge surge in parcels imported via Chinese online platforms in recent years. The compliance of these goods with EU rules, such as consumer safety, is one major challenge. Another is that the sheer volume of small parcels arriving from China each year hampers inspection and tax collection, leading to significant loss in revenue. Since July 2021, all imports into the EU have been subject to VAT and an import declaration, regardless of their value. But that reform did not alter the customs-duty relief for parcels valued under EUR 150, leaving considerable space for exploitation by China’s e-commerce platforms focused on competitive product pricing.

To address this, from July 1, 2026, the EU will introduce a temporary, fixed customs duty of EUR 3 per item category in parcels under the EUR 150 threshold. This interim measure will be in effect until implementation of a wider customs reform. In parallel, the EU will levy a new handling fee for goods entering from non-EU countries and sent directly to EU consumers, to be introduced before November 1, 2026.

But the fundamental issue remains: National customs services need to verify the contents of packages arriving in huge numbers. The EU currently has no full picture of the magnitude of this challenge. This is one reason the attached graph draws on data from China Customs. The EU Customs Union Reform agreed in March may provide a consistent, EU-wide solution to the problem of data collection via 27 different national IT systems. The plan is to create a digital EU Customs Data Hub – a centralized, AI-driven platform replacing those at the national level.

The implementation of the pan-EU solution will take time but is the only realistic way forward. National attempts to address the issue – even though customs is an EU competence – have fallen flat, as shown by Italy’s attempt to introduce a tax on small parcels at the national level.

SHORT TAKES

The first dedicated discussion on China by the European Commission’s Security College, which brings together the full College of Commissioners, slated for April 13, was postponed in order to prioritize the Gulf crisis and the risk of further energy disruption. The rescheduling illustrates a broader problem for the EU: Even as China rises on the agenda, immediate geopolitical shocks continue to disrupt strategic debate. At the same time, however, the Commission has been quietly moving on more targeted measures. For example, it plans to restrict EU funding channeled into projects that contain China-made inverters, equipment that is critical for renewable energy systems.

- SCMP: China sidelined: EU shelves rare strategy debate as Middle East crisis takes priority

- SCMP: EU to cut funding for Chinese inverters as quiet offensive replaces grandstanding

Hungary’s April 12 election ended Viktor Orbán’s 16-year rule and may weaken the political exceptionalism that shaped China-Hungary ties. Péter Magyar has signaled pragmatism, saying Hungary should remain open to “Eastern ties.” But his push for tighter oversight of battery plants and fewer subsidies for gigafactories point to greater scrutiny of Chinese projects, especially CATL and BYD, and a more transactional relationship. Magyar could also review the opaque Budapest–Belgrade railway deal, which Orbán’s government long treated as a politically protected flagship project, and which has faced accusations of misusing public funds.

- Euronews: Péter Magyar walks line between Brussels and Beijing on China trade

- Global Times: Hungary's Magyar says open to cooperation with China

On February 12, China concluded an 18-month anti-dumping investigation into European dairy products, initiated after the EU imposed tariffs on electric vehicles made in China. China has now reduced dairy tariffs to 7.4-11.7 percent from 21.9-42.7 percent. The tariffs apply to around EUR 500 million in exports and are set to remain in place for five years.

- MOFCOM [CN]: Announcement No. 9 of 2026 on the final ruling on the countervailing investigation of import-related dairy products originating in the EU

- Reuters: China lowers EU dairy tariffs in final ruling after 18-month probe

Italy tightened its restrictions on Chinese state-owned Sinochem’s control over premium tire manufacturer Pirelli. Sinochem is Pirelli’s largest shareholder. The government’s “golden power” rules, aimed at protecting Italy’s national interests, cut Sinochem’s board seats to three from eight and barred it from top corporate roles. The move shows that, for Rome, Chinese capital remains welcome only if it doesn’t jeopardize strategic control of domestic companies or their access to the US market. Pirelli’s ownership structure poses a problem as the Trump administration has recently clamped down on the use of Chinese automotive tech. Sinochem says it will appeal the decision.

- Reuters: Italy imposes curbs on China's Sinochem to avoid US restrictions on Pirelli

- Reuters: Italy's curbs on Chinese investor allow Pirelli full access to US market, minister says

In February, the Polish army banned China-made connected vehicles from entering military sites and barred its personnel from connecting official cell phones to them due to data collection concerns. Similar restrictions were already in place in China, prompting suspicions that Beijing may itself use connected vehicles for espionage purposes.

Author(s)

Visiting Fellow

Analyst

Head of Brussels Office/Senior Analyst

Author(s)

Visiting Fellow

Analyst

Head of Brussels Office/Senior Analyst

Content