picture alliance / CFOTO

Kommentar

China’s new Five-Year Plan will embrace industry – and once again give consumers the cold shoulder

Despite pledges to boost consumption, Beijing will continue with its expansive industrial policy, says Alexander Brown. This article is part of our series on China’s 15th Five-Year Plan, which the National People’s Congress is scheduled to adopt in early March.

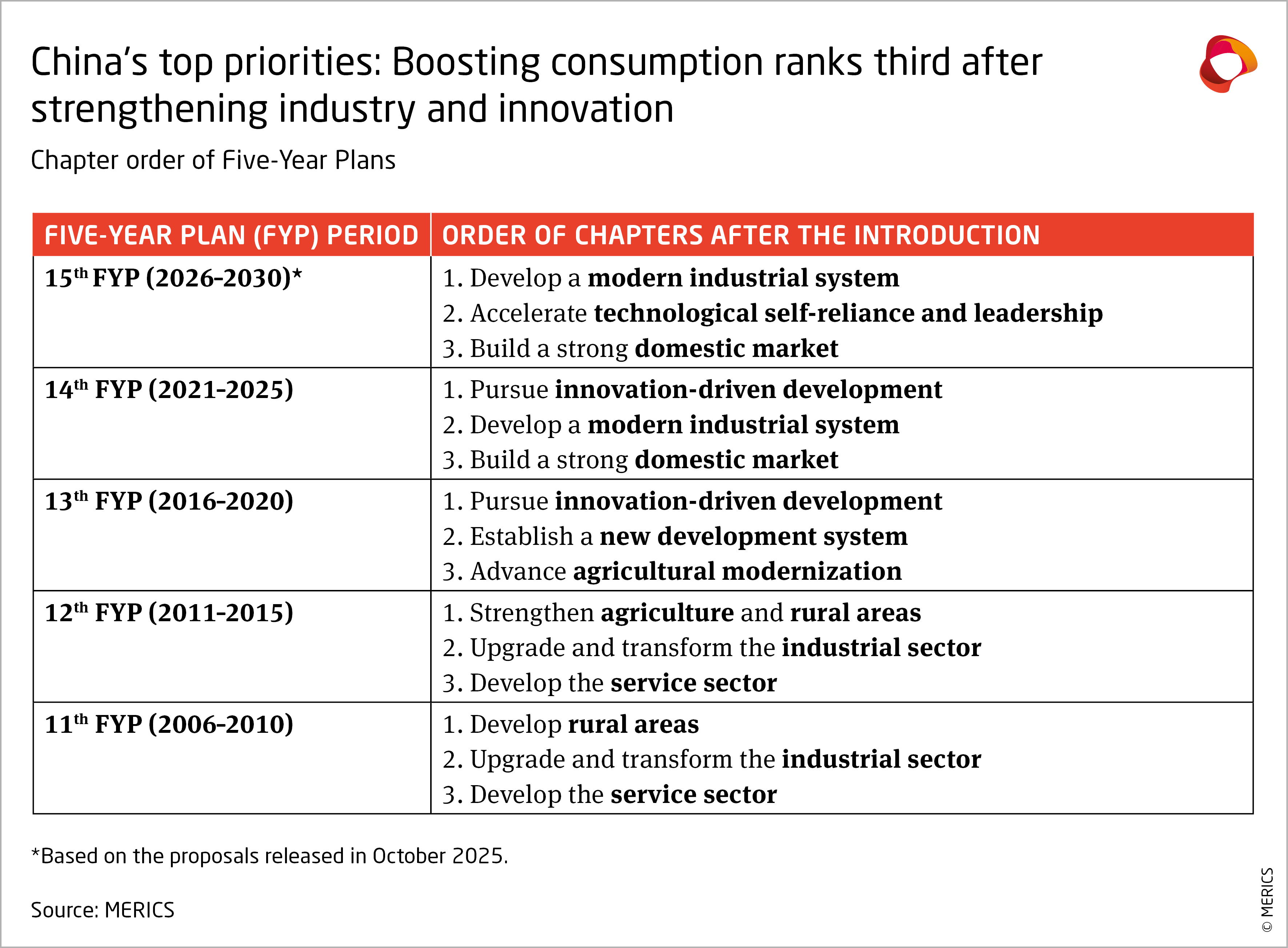

China’s 15th Five-Year Plan looks set to declare boosting domestic consumption a top economic priority for the second consecutive planning period. Based on the order of the chapters in the CCP leadership’s recommendations for the document, the goal of building “a strong domestic market” has once again made it into the top three alongside support for industry and innovation (see Figure 1). But five years after this elevation, Chinese households have little to show for it – and it’s unlikely that situation will change any time soon.

Consumers an afterthought in Beijing's quest for industrial strength

The Chinese leadership’s recommendations for the 2026 – 2030 economic plan call on officials to “use new demand to guide new supply, and new supply to create new demand, so as to promote a virtuous cycle between consumption and investment” – while the country’s ongoing flood of exports and low domestic demand show in which direction the Chinese economy remains skewed. According to the party line, investments in upgrading supply stimulate demand, reducing the need to support consumption through welfare payments and other measures to increase household income.

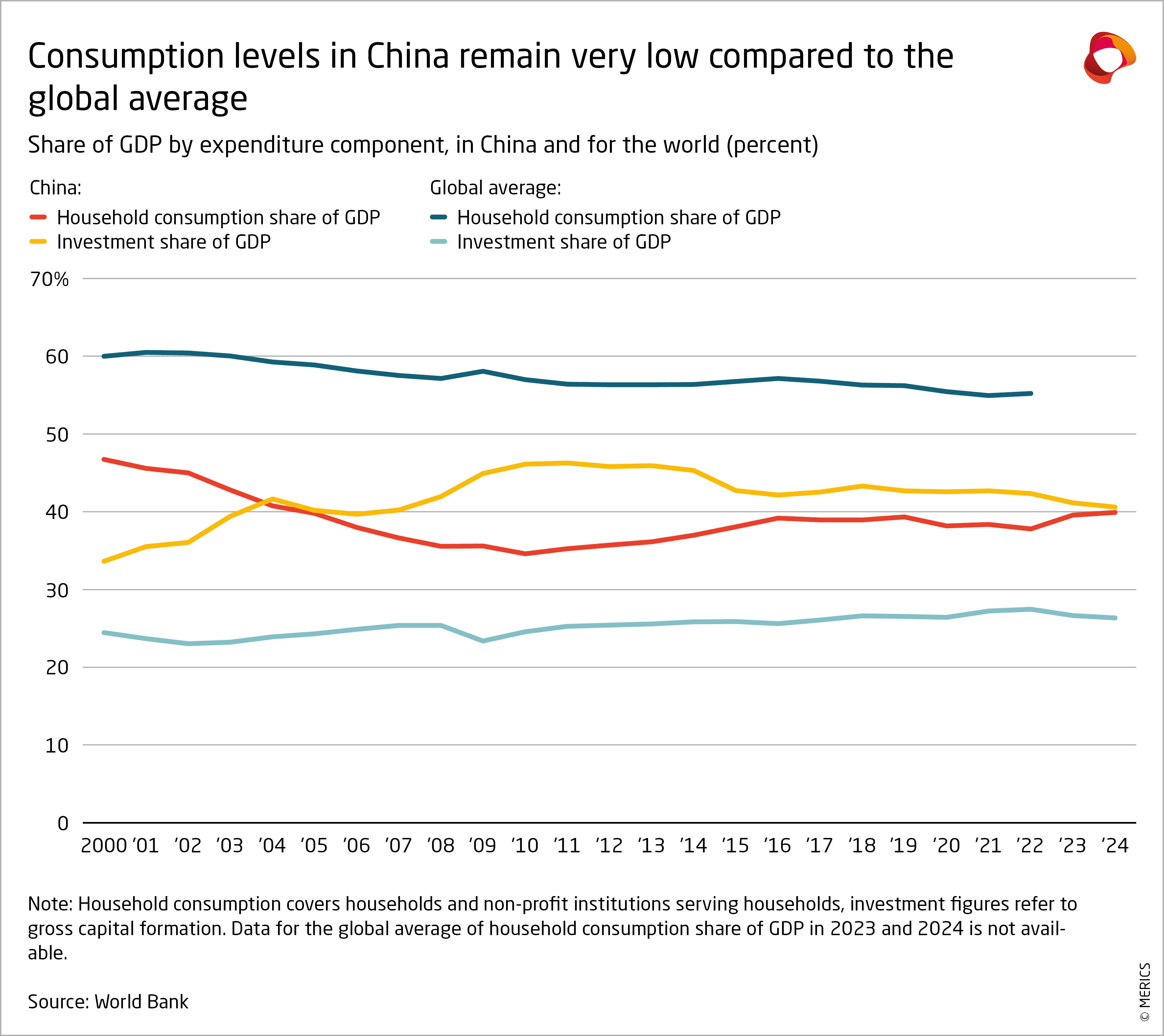

Social transfers through social security, welfare, allowances, healthcare and education currently amount to about 13 percent of GDP, compared to about 30 percent in the EU, and consumption has been persistently low for years. Since 2005, household consumption has on average accounted for 38 percent of China’s GDP, compared to a global average of 57 percent (see Figure 2). Reversing this trend would require substantial reforms to a raft of policies which systematically favor industrial enterprises over consumers. In China, banks offer savers artificially low interest rates and to enable cheaper loans to companies, weak worker rights suppress wages for low-skilled labor, and its regressive tax system disproportionately burdens lower-income households.

Pressure is mounting for a shift in direction. China’s economic growth looks precariously balanced on one leg – its thriving exports – as weak domestic consumption and falling investment leave other potential growth engines sputtering.

But despite the wording of last and the next FYP, China’s economic policy is and will remain resolutely skewed towards supporting industry over households. Xi Jinping is convinced that this approach is not only necessary to boost China’s resilience in an era of great power competition, but also best serves the country’s long-term economic development. The result will be a continued slow-rolling of measures to expand social welfare – and ever more Chinese firms climbing the value chain in their industrial sectors.

Beijing goes all in on high-tech and leaves households to eat bitterness

Xi’s emphasis on fostering “new quality productive forces” essentially presents investments in high-tech sectors as a panacea for overcoming the country’s challenges of slowing growth, rising debt and an ageing workforce. The official narrative depicts China as poised to lead the next wave of technological revolutions in emerging fields like artificial intelligence, biotech, quantum computing and new materials. Beijing hopes innovation in these areas will drive productivity gains that result in higher corporate profits, feed into higher wages, more service-sector jobs, and increased tax revenue – at which point the government will finally be able to raise welfare spending.

But what sounds convincing in theory, amounts to a clear trade-off between raising living standards and corporate profits in short-term, as well as a risky bet over the long-term. There is no guarantee that growth in high-tech industries will deliver significant gains for the broader economy. Robotics, cars, green tech, drones and many other high-tech sectors are highly automated, which means their ability to improve employment opportunities for China’s large migrant work force will be marginal. The strong focus on producing goods will also divert capital away from the service sector, which is where growth in consumption is most likely.

On top of that, China’s expansive industrial policy and pursuit of self-reliance have fueled growing corporate and government debt rather than boosting productivity. In electric vehicles and other sectors in which China has succeeded in fostering competitive domestic players, the country has also unleashed economic “involution” – a destructive form of corporate competition that puts downward pressure on prices, investments, wages and profits. Many companies reliant on state financing have become more of a liability than an asset.

The next five years are crucial for securing Europe’s own industrial base

Lastly, other countries do have a say in whether Beijing can pull off its supply-side wager. As long as China shies away from reforms to boost domestic consumption, access to foreign markets will remain crucial to generate returns on corporate investment. Facing growing trade imbalances with China, fifty-two of the world’s 70 largest economies (including the EU-27) in 2025 took steps to protect selected sectors – even if these have as yet failed to curb an export glut that saw China’s trade surplus grow 20 percent to a record USD 1.2 trillion in 2025.

Stronger action from China’s major trading partners would put Beijing under greater pressure to deliver on its pledge to boost domestic consumption. It is clear that the EU, in particular, should strengthen its trade defense measures. Europe’s industrial base in car making, machinery, chemicals and pharmaceuticals faces ever greater pressure not only from Chinese companies, but also from European ones investing in R&D and production in China.

The 15th Five-Year Plan will send a clear signal that China wants to retain and expand its position as the world’s factory. The challenge for EU policymakers now is to send equally loud message, letting it be known that Europe’s days as an industrial powerhouse are not over yet.

Autor(en)

Senior Analyst

Autor(en)

Senior Analyst